What Is An Advantage Of An Adjustable Rate Mortgage Brainly

Picture this: my friend, let's call him Alex, was buzzing. He'd just snagged his first apartment, a sweet little studio with a balcony that promised future rooftop parties (or at least a spot for his overly dramatic plant collection). He was so excited about the place, he barely glanced at the mortgage details. "It's a good rate!" he'd declared, flashing a thumbs-up that I swear was 90% pure adrenaline and 10% actual financial understanding.

Fast forward a year. Alex calls me, sounding less like a proud homeowner and more like a squirrel who's just discovered winter is, indeed, coming. "Dude," he’d wailed, "my mortgage payment just jumped! Like, significantly!" Turns out, his "good rate" was… well, adjustable. And the rates had decided to take a scenic detour upwards. So, while Alex learned a very valuable, albeit expensive, lesson about reading the fine print, it got me thinking. What are the advantages of these sneaky, shape-shifting things called Adjustable Rate Mortgages, or ARMs, as the cool kids call them?

Let's dive in, shall we? Because while Alex's situation was a bit of a cautionary tale, ARMs aren't all bad. In fact, for some folks, they can be downright brilliant. Think of it like this: life is unpredictable, right? Sometimes you get a surprise bonus at work, other times your car decides to impersonate a deflated balloon. A mortgage, in its own way, can be a little like that. And an ARM? Well, it offers a bit of flexibility in that unpredictable dance.

So, What's the Big Deal with an ARM?

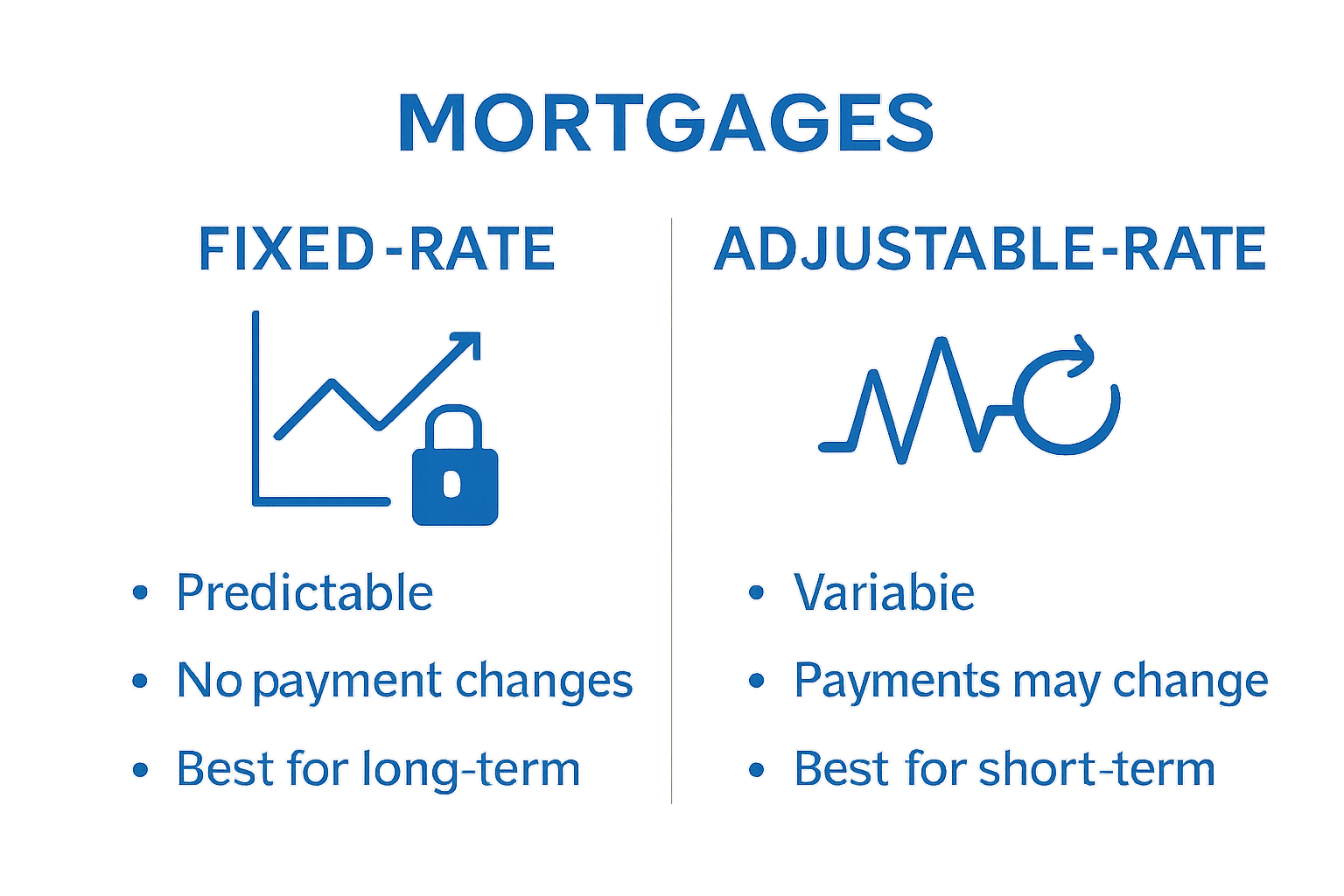

Okay, deep breaths. Forget the horror stories of sky-high payments for a sec. At its core, an Adjustable Rate Mortgage is a home loan where the interest rate can change over time. Unlike a Fixed-Rate Mortgage (FRM), where your rate is locked in for the entire life of the loan – think of it as a stubbornly reliable old friend – an ARM is more of a… free spirit. It starts with an initial rate, often for a set period (like 5, 7, or 10 years), and then, bam! it starts to float based on market conditions. It's like having a variable wardrobe based on the weather.

Now, before you start imagining your payment doing the cha-cha to the moon, understand that these changes aren't random acts of financial chaos. ARMs have rules. They have what we call "caps." These are like guardrails, designed to prevent your rate from going completely off the rails. There's usually a cap on how much the rate can increase at each adjustment period (often called the periodic or one-time adjustment cap) and a cap on how much it can increase over the entire life of the loan (the lifetime cap). So, while Alex might have had a shock, his rate probably didn't climb to something utterly unmanageable thanks to those caps.

The Golden Goose: Lower Initial Payments

Here's where we get to the real potential upside. One of the most significant advantages of an Adjustable Rate Mortgage is the potentially lower initial interest rate. Because the lender is taking on a bit of risk with the fluctuating rate, they'll often offer a lower starting rate compared to a fixed-rate mortgage. This means, for that initial period, your monthly payments will likely be lower. Significantly lower, sometimes.

Why is this a good thing? Well, for starters, it can make homeownership more accessible. If you're buying your first home and your budget is a little tight, that lower initial payment can be a lifesaver. It can give you more breathing room in your monthly budget, allowing you to perhaps save up for that fancy new sofa you’ve been eyeing, or, you know, build up an emergency fund. Because, let's be real, life happens, and having a financial cushion is always a good idea.

:max_bytes(150000):strip_icc()/what-is-an-adjustable-rate-mortgage-3305811_V2-d24ce035796b4b3ebb7cee3f65049a24.png)

Think of it like getting a great deal on a new car. You get the cool ride now, and for a while, your payments are easier on the wallet. It’s the allure of immediate savings. This initial period of lower payments can be particularly attractive if you anticipate your income increasing in the near future. Maybe you're expecting a promotion, or you're planning to take on some freelance work. That lower initial payment acts as a bridge until your finances are more robust.

The "We're Not Staying Long" Strategy

This is a big one, and it's where ARMs truly shine for a specific group of people. If you have a solid plan to sell your home or refinance before the initial fixed-rate period ends, an ARM can be an absolute no-brainer. Let's say you buy a starter home with a 5-year ARM, with the intention of selling it in 3-4 years to move up to a bigger place. You benefit from the lower initial interest rate for those crucial years, and then you're out of the ARM game before it even has a chance to get truly interesting (and potentially expensive).

This strategy is particularly popular with people who are in the military and might face mandatory relocations, or for individuals who are in a job that requires frequent moves. Or, let's be honest, for people who just love to move! If you know you're going to be in your home for less than the typical 7-30 year mortgage term, an ARM can be a smart financial move. You get the benefit of lower payments for the time you’re actually in the house, and then you pass the baton (and the potential rate fluctuations) onto the next buyer.

It's a calculated gamble, for sure, but one that can pay off handsomely. You're essentially buying time and saving money during your ownership period. You get to enjoy the benefits of a lower monthly outlay while you're there, and then you move on to your next adventure, leaving the ARM to its own devices. It’s a bit like test-driving a car for a few years before committing to a long-term lease.

The "Rates Might Go Down" Hopeful

Okay, this one is a bit more of a gamble, and it requires a healthy dose of optimism about the economy. But, here's the thing: if interest rates fall, your ARM's interest rate can also fall. This is the flip side of the coin from Alex's predicament. Instead of your payment jumping up, it could potentially drop. Imagine that! Your monthly mortgage bill gets smaller, freeing up even more cash. It’s like finding a twenty-dollar bill in a coat pocket you haven’t worn in ages.

This scenario is more likely if you lock in an ARM when interest rates are high, and then they subsequently decrease. The initial rate is lower than a comparable fixed-rate mortgage might have been at that time, and you get the benefit of future rate drops. It's a double whammy of good news. This is where a bit of economic forecasting (or just a lucky guess) can really pay off.

However, and I cannot stress this enough, this is a big "if." Relying solely on rates going down is a risky game. It's like betting on your favorite sports team to win every single game of the season. Sometimes it happens, but you wouldn't base your entire financial future on it, would you? So, while the possibility of lower payments is a definite advantage, it shouldn't be the only reason you choose an ARM.

Flexibility in Uncertain Times

Life is a giant, beautiful, messy question mark, isn't it? And sometimes, having a mortgage that’s a little less rigid can be a good thing. If you anticipate a period of financial uncertainty or change, an ARM can offer some breathing room. For instance, if you're self-employed and your income fluctuates significantly, the lower initial payments of an ARM might be more manageable than the consistent higher payments of a fixed-rate mortgage.

Or, perhaps you're planning a major life event that could impact your finances, like going back to school, starting a new business, or even anticipating a significant change in your family situation. In such cases, the initial lower payments of an ARM can provide a financial buffer, allowing you to navigate these changes without the added burden of a higher, fixed mortgage payment. It's like having an adjustable seat in your car – you can fine-tune it to fit your current needs.

This flexibility can be especially valuable if you're a first-time homebuyer who is still getting a handle on their long-term financial stability. It allows you to ease into homeownership without the immediate pressure of the highest possible monthly payment. It’s a way to get your foot in the door and then adjust as you find your financial footing.

Who is an ARM Best For? (Besides Alex, maybe after therapy)

So, who are these ARMs really for? Let's break it down:

- The Short-Term Homeowner: If you know you'll be selling within the initial fixed-rate period (usually 3, 5, 7, or 10 years).

- The Savvy Investor: Those who are adept at market forecasting and believe they can benefit from falling interest rates or have a solid refinance strategy.

- The Budget-Conscious Buyer: Individuals or families who need lower initial payments to afford a home and can manage potential future increases.

- The Strategically Mobile: People whose careers or life circumstances might require them to move or refinance within a few years.

It’s important to remember that an ARM isn't a one-size-fits-all solution. It requires careful consideration of your personal financial situation, your risk tolerance, and your future plans. You need to be comfortable with the idea that your payments could go up, even with those handy caps in place.

The Flip Side of the Coin (Because Nothing is Perfect)

Now, before you go running off to your bank with stars in your eyes about ARMs, let's have a quick chat about the downsides. Because, as Alex learned, there's always a flip side. The biggest "uh-oh" is the risk of rising interest rates. If rates go up, so does your payment. And that can be a nasty surprise, as poor Alex can attest. You need to be able to comfortably afford your payment even at the maximum possible interest rate allowed by the caps.

Also, ARMs can be a little more complex to understand than fixed-rate mortgages. There are more moving parts, more terms to grasp, and more potential for confusion. It's not as simple as "this much per month, for this many years." You have to really dig into the details of the rate structure, the adjustment periods, and those all-important caps.

So, while the advantages are definitely there, it's crucial to weigh them against the potential risks and complexities. Do your homework, talk to a trusted financial advisor, and make sure you fully understand what you're signing up for. Don't be like Alex, who was so focused on the balcony that he forgot to check the foundation.

Ultimately, the "advantage" of an adjustable-rate mortgage boils down to its flexibility and potential for lower upfront costs. For the right person, in the right circumstances, it can be a brilliant financial tool. For others, it can be a recipe for sleepless nights. The key is to understand your own situation and to make an informed decision. And maybe, just maybe, read all the way to the end of the mortgage document. Your future self (and your plant collection) will thank you.