Whole Life Insurance Policy Explained: How It Works And What It Costs

Hey there, friend! So, you’ve been hearing all about this thing called "whole life insurance," and it sounds about as exciting as watching paint dry, right? I get it. Insurance can feel a bit… well, insurance-y. But stick with me for a few minutes, because whole life insurance isn't just some stuffy financial product. It’s actually a pretty neat tool that can offer some serious peace of mind and even a little bit of a financial superpower. Think of it as a lifelong hug for your loved ones, wrapped in a surprisingly smart financial package. Let's break it down, no boring jargon allowed!

Imagine this: you're looking for a way to make sure your family is taken care of, no matter what. You know, the classic “what if I’m not around anymore?” scenario. Term life insurance is like renting a life insurance policy. It covers you for a specific period, say 20 or 30 years. It’s great for covering big debts like a mortgage or ensuring your kids are funded through college. But eventually, that rental agreement ends, and poof! No more coverage. Whole life, on the other hand, is more like owning that life insurance. It's yours for your entire life. Pretty cool, huh?

The "Whole" Story: How This Magical Policy Works

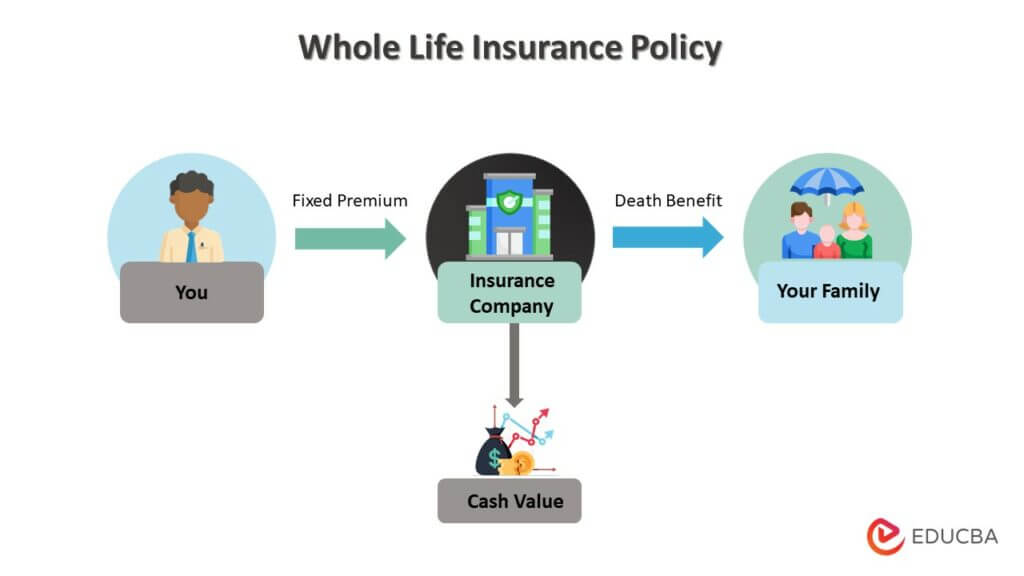

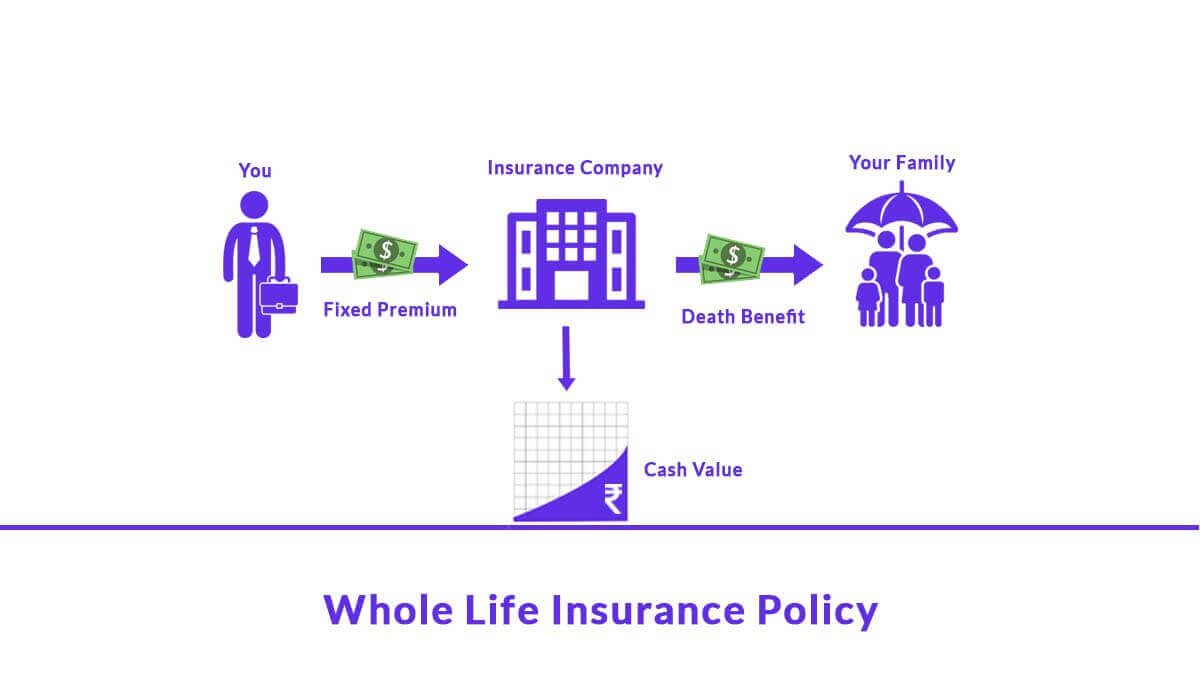

So, how does this whole-life magic happen? It’s actually pretty straightforward, despite the fancy name. When you get a whole life insurance policy, you're essentially signing up for two main things:

1. A Lifelong Death Benefit (Your Family’s Safety Net)

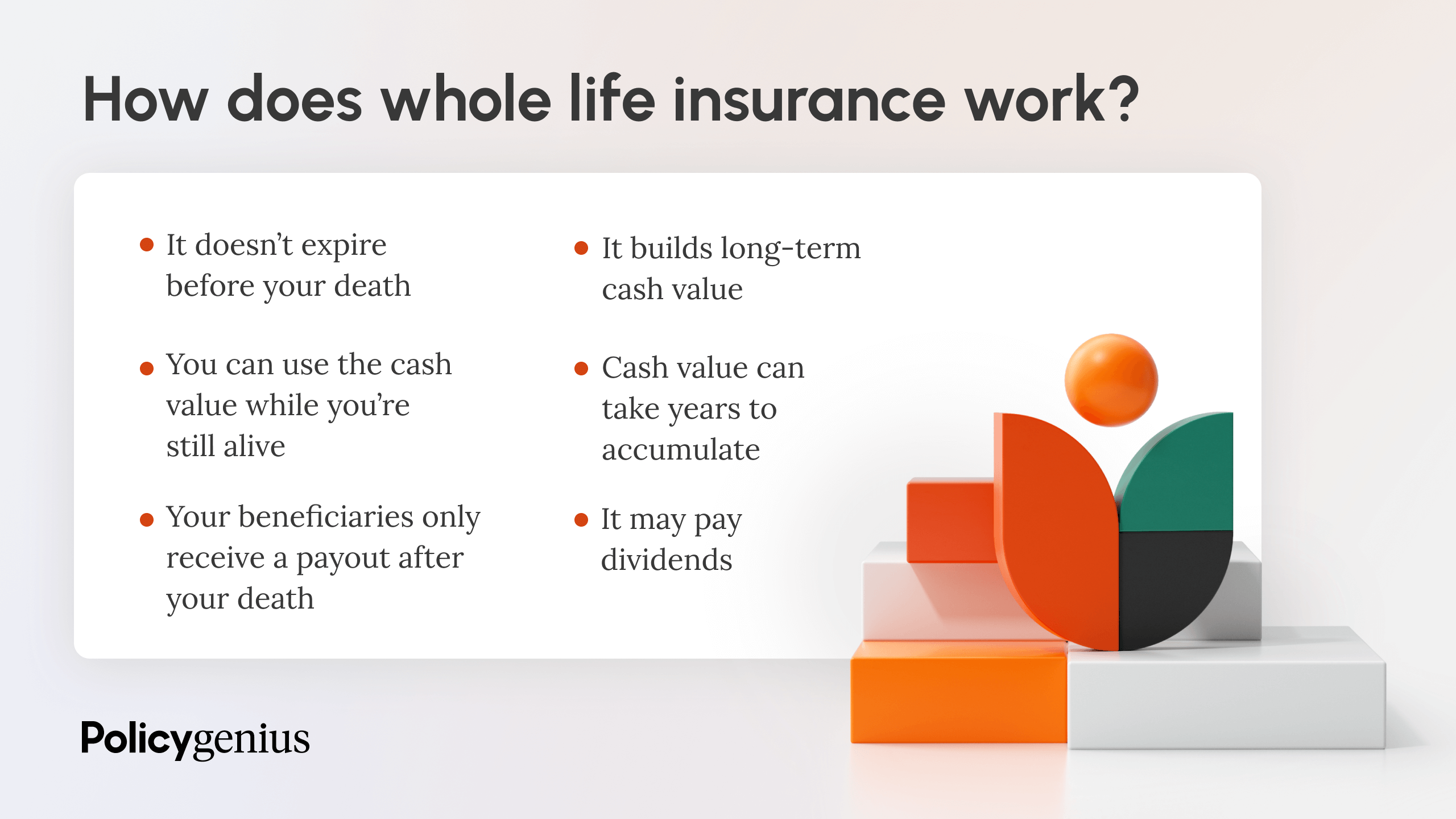

This is the big kahuna, the main reason most people get life insurance. A whole life policy guarantees a specific amount of money, called the death benefit, will be paid out to your chosen beneficiaries when you… well, when you shuffle off this mortal coil. No questions asked (well, very few!).

Think of it as leaving behind a financial cushion for your loved ones. This money can help them cover immediate expenses like funeral costs (which, let's be honest, can be shockingly high), pay off debts (mortgage, car loans, that credit card you swear you'll pay off next month), or even replace your income so they can maintain their lifestyle. It’s a way to say, “I’ve got your back, even when I can’t physically be there.” And that, my friend, is priceless.

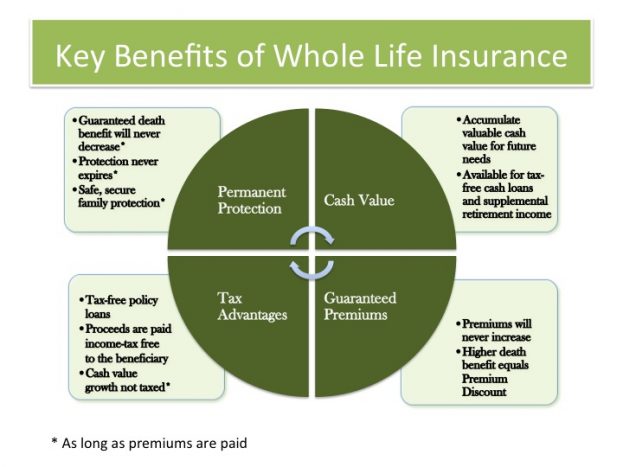

The beauty of the death benefit in a whole life policy is that it's guaranteed. Unlike some other investments that can fluctuate with the market, this payout is locked in. So, your beneficiaries can count on it, providing immense relief during what will undoubtedly be a difficult time.

2. A Cash Value Component (Your Little Financial Secret)

Now, this is where whole life insurance really starts to get interesting and, dare I say, fun! Besides the death benefit, your policy also accrues something called cash value. Think of this as a savings account that grows tax-deferred over time, built right into your insurance policy.

Every premium payment you make isn't just paying for your coverage. A portion of it goes towards keeping your death benefit active, and another portion is added to your cash value. This cash value grows at a guaranteed rate, determined by the insurance company. Some policies might also pay dividends, which are like little bonuses you can choose to reinvest, take as cash, or use to reduce your premiums. It’s like your insurance policy is secretly working for you, accumulating wealth while it protects you!

Here's the neat part about the cash value: you can access it! You can borrow against it (like a loan against your own money, usually without credit checks) or even withdraw from it (though be mindful, withdrawals can reduce your death benefit). This cash value can be a fantastic resource for unexpected emergencies, a down payment on a dream vacation, or even supplement your retirement income later in life. It's like a hidden pot of gold that grows with you.

It's important to remember that the cash value grows slowly in the early years of the policy. Don't expect to get rich overnight! It's more of a marathon runner, steadily building wealth over the long haul. But the fact that it's growing tax-deferred is a pretty sweet deal in the world of finance.

How Do You Pay for This Awesome Insurance? (The Nitty-Gritty of Premiums)

Alright, let's talk about the cost. Because nothing in life is entirely free, right? Whole life insurance premiums are generally higher than term life insurance premiums. Why? Because you're getting lifelong coverage and that accumulating cash value. It’s like comparing the cost of renting a small apartment for a few years versus buying a sturdy house that will be yours forever.

Your premium amount will depend on a few key factors:

- Your Age: Younger you are when you buy, the lower your premiums will likely be. It's like getting the best deal before the "early bird special" ends.

- Your Health: Good health is a gold star! If you're a picture of health, your premiums will be more favorable. If you have some pre-existing conditions, they might be a bit higher, but don't let that discourage you. Many people with health issues can still get coverage.

- The Death Benefit Amount: The more money you want to leave behind, the more expensive the policy will be. It makes sense, right? More protection = more cost.

- The Insurance Company: Different companies have different pricing structures, so shopping around is always a good idea.

One of the major perks of whole life insurance premiums is that they are usually fixed. Once you lock in your policy, your premium amount stays the same for the rest of your life. No scary surprises or sudden jumps in cost as you get older. This predictability is a huge relief for budgeting and financial planning. Imagine never having to worry about your insurance bill doubling next year! That’s a win in my book.

Now, if you're on a super tight budget, the initial cost of whole life might seem a little daunting. But remember that ever-growing cash value. It can act as a safety net, and as it grows, it can potentially offset some of your premium costs over time, or even provide funds when you need them. It’s like planting a tree that will eventually bear fruit.

Who is Whole Life Insurance For? (Is it Your Financial Soulmate?)

So, who benefits most from this lifelong insurance buddy? Whole life insurance is often a great fit for people who:

- Want lifelong coverage: You want to ensure your beneficiaries are always protected, regardless of when you pass away.

- Are financially stable and can afford the premiums: You have the budget for the higher, but fixed, premiums.

- Want to build cash value: You like the idea of a savings component that grows tax-deferred.

- Have estate planning goals: It can be used as a tool to pass on wealth or cover estate taxes.

- Value predictability: You appreciate the guaranteed death benefit and fixed premiums.

It’s also a fantastic option for parents or grandparents who want to leave a legacy for their children or grandchildren, ensuring they have a financial head start or a fund for future needs, like education. It's like leaving them a little extra love in a tangible form.

On the flip side, if you only need coverage for a specific period (like to cover your mortgage until the kids are out of the house), term life insurance might be a more cost-effective choice for your immediate needs. It’s all about matching the right tool to your specific financial toolbox.

The Upsides and Downsides: Let's Be Honest

Like anything in life, whole life insurance has its pros and cons. Let’s be real:

The Sunny Side (Pros):

- Lifelong Protection: You’re covered from day one until your very last day. No worries about policy expiration.

- Guaranteed Death Benefit: Your beneficiaries will receive a predetermined amount. No market crashes can touch this!

- Cash Value Growth: Your money grows tax-deferred, and you can access it. It’s a built-in savings plan that’s a bit more… robust.

- Fixed Premiums: Your payments won't go up over time, making budgeting a breeze.

- Potential for Dividends: Some policies can pay out dividends, adding an extra boost to your cash value.

- Estate Planning Tool: Can help manage estate taxes and provide a smooth transfer of wealth.

The Not-So-Sunny Side (Cons):

- Higher Premiums: Compared to term life, it costs more upfront.

- Slower Cash Value Growth Initially: It takes time for the cash value to build up significantly. Don't expect instant riches.

- Complexity: While we're making it sound easy, there are nuances. It’s good to chat with a financial pro.

- Less Flexibility for Some: If your financial situation changes drastically, modifying a whole life policy can be tricky.

A Little Bit About Costs (The Real Numbers)

Okay, so you want some numbers, right? This is where things get a bit more personalized, because as we said, it depends on you. But let’s give you a ballpark idea. For a healthy 30-year-old non-smoking male looking for a $500,000 death benefit, a whole life policy might range from $500 to $1,000+ per month. For a 50-year-old, that same coverage could be anywhere from $1,500 to $2,500+ per month.

Remember, these are just estimates. A 20-year term policy for the same 30-year-old might be closer to $50-$100 per month. See the difference? It’s that lifelong coverage and cash value component that bumps up the price tag.

Think of it like this: a fancy, high-end coffee maker that will last you for decades and brew amazing coffee every morning will cost more than a basic drip machine that gets the job done for a few years. Both have their place, but one offers more long-term value and features.

It’s crucial to get personalized quotes from reputable insurance companies. They’ll take into account all those factors we mentioned (age, health, etc.) to give you an accurate picture of what your policy would cost. Don't be afraid to ask questions! A good agent will explain everything clearly.

The Takeaway: More Than Just a Policy, It's a Plan!

So, there you have it! Whole life insurance, demystified. It’s not some arcane secret society thing; it's a tool that offers lifelong protection, a growing savings component, and peace of mind. It’s for those who want to build a solid financial foundation for their future and ensure their loved ones are taken care of, no matter what life throws their way.

It might seem like a big decision, and it is! But by understanding how it works, what it costs, and who it's for, you're already ahead of the game. Think of it as investing in your future and the future of those you care about. It’s a way to send a message of love and security that lasts a lifetime and beyond.

And hey, if you’re feeling a little overwhelmed, that’s totally normal! The best advice is to chat with a trusted financial advisor. They can help you navigate the options and find the perfect fit for your unique situation. Because at the end of the day, having a solid plan in place, whatever it may be, is one of the kindest things you can do for yourself and your loved ones. Go forth and secure that peace of mind, knowing you’ve got a little bit of financial sunshine for whatever tomorrow may bring!