When Can You Cash Out An Ira Without Penalty

Hey there, money wizards and dreamers! Ever looked at your IRA and thought, "Man, that's a nice nest egg, but what if...?" We all have those moments, right? That little spark of "what if" that could lead to anything from a spontaneous trip to seeing your kid off to college without a financial white-knuckle ride. Well, guess what? Cashing out your IRA without a penalty might be more accessible than you think! Let's dive into the fun stuff and uncover when those funds can become your financial superheroes.

Now, before you go imagining a yacht with your name on it (though, a girl can dream!), it's important to know that the IRS has some rules. Think of them as friendly bouncers at the "penalty-free party." But don't let that scare you! These rules are often there for good reasons, and more importantly, they pave the way for some genuinely awesome life events.

The Big 5-0: A Milestone Worth Celebrating (and Possibly Funding!)

This is the golden ticket, folks! If you've hit the magical age of 59 1/2, congratulations! You've officially unlocked the penalty-free withdrawal zone. Seriously, it's like getting a VIP pass to your own money. No more worrying about those pesky 10% early withdrawal penalties. This is your time to enjoy the fruits of your labor, whether that means finally taking that dream cruise, investing in a passion project, or simply boosting your current lifestyle. Go on, you've earned it!

Think about it: all those years of saving, diligently putting money away. Now, the universe (or, you know, the IRS) is basically saying, "Okay, you've been good. Enjoy!" It’s a pretty fantastic feeling, isn't it? So, if you're approaching this milestone, start dreaming up what your next adventure will be. The possibilities are practically endless!

When Life Throws You a Curveball (The Really Expensive Kind!)

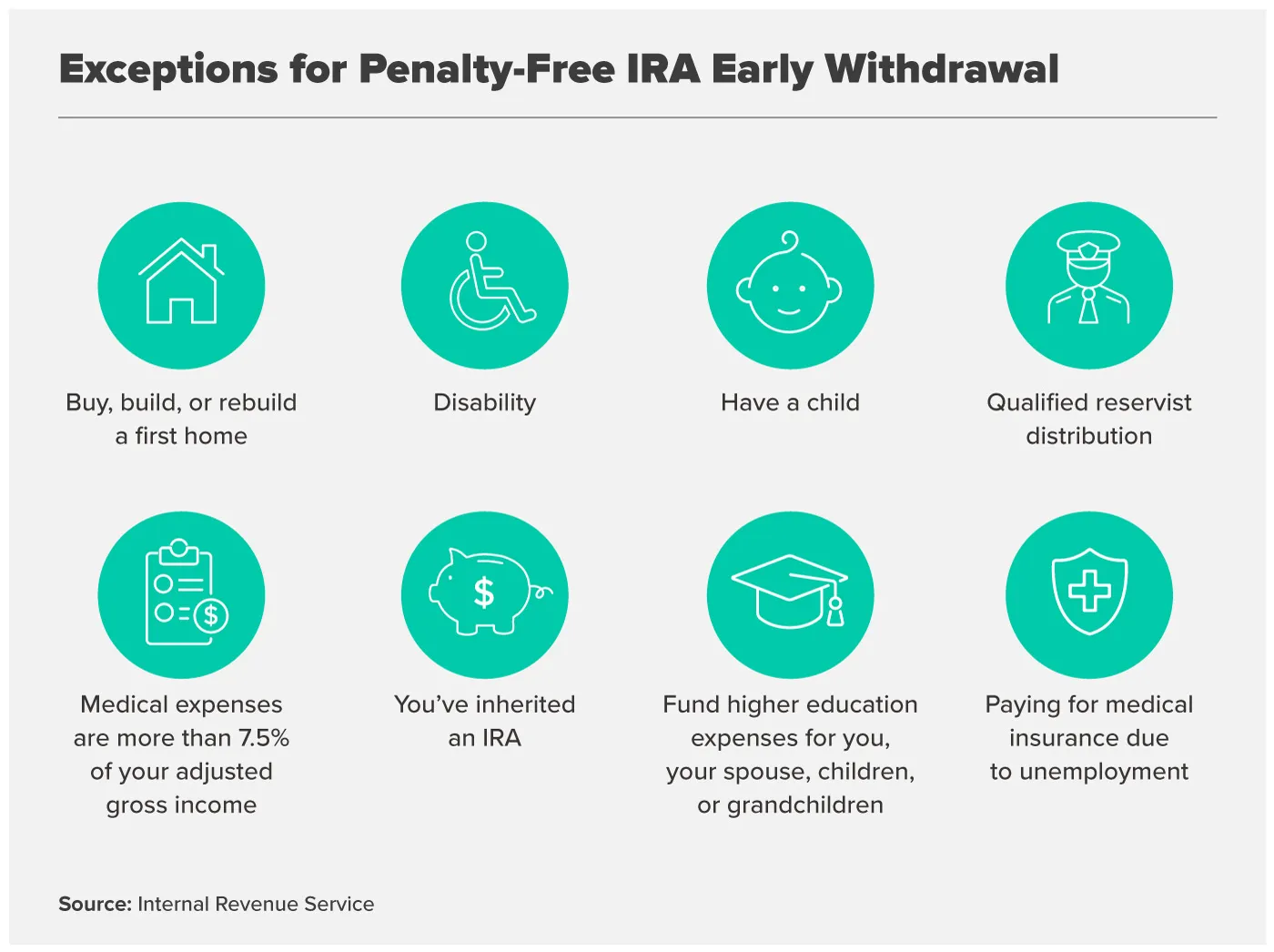

Life, bless its unpredictable heart, sometimes throws us curveballs that require a bit of financial muscle. Fortunately, the IRA has a few hardship exceptions designed to help you out. These are for situations that are truly unavoidable and stressful.

First-Time Homebuyer Bonanza!

Buying your first home is a HUGE life event! And guess what? The IRS wants to help make that dream a reality. You can withdraw up to $10,000 (lifetime limit) from your IRA penalty-free to help with qualified first-time homebuyer expenses. This is fantastic! Think of it as a down payment boost, a little extra cushion for closing costs, or even for some essential furniture to make your new place feel like home.

:max_bytes(150000):strip_icc()/Takingmoneyoutofanira-98057a4d86a843f99b9141cd5c111009.png)

So, if you've been renting and dreaming of owning your own slice of the world, your IRA can be a powerful ally. It’s not just about saving for retirement anymore; it’s about building your present life too. How cool is that? Imagine signing those papers, keys in hand, knowing your IRA played a little part in making it happen.

Higher Education Heroics!

Education is an investment in the future, and sometimes, that future comes with a hefty tuition bill. Good news! You can withdraw funds from your IRA penalty-free to pay for qualified higher education expenses for yourself, your spouse, your children, or even grandchildren. This includes tuition, fees, books, supplies, and even some room and board costs.

This is a game-changer for so many families. It means less reliance on expensive student loans and more freedom to choose the best educational path. So, whether you're looking to further your own learning or help a loved one achieve their academic goals, your IRA can be a valuable resource. It's a way to invest in knowledge, which, let's be honest, is always a smart move.

The Unexpected Medical Marvels

When health issues arise, the last thing you want to worry about is a financial penalty. The IRS understands this. You can withdraw funds penalty-free to pay for unreimbursed medical expenses that exceed 7.5% of your Adjusted Gross Income (AGI). This is for significant medical bills, so it's a lifeline when you need it most.

This exception is a true testament to the idea that financial planning should support your well-being. It’s a safety net for those times when life’s challenges demand immediate attention. Knowing this option exists can bring a significant amount of peace of mind during difficult times.

The Birth of a Baby or the Arrival of an Adopted Child

Welcome to the world, little one! To help new parents navigate the joys (and expenses!) of a new baby, you can withdraw up to $5,000 penalty-free within one year of the birth of a child or the placement of an adopted child for adoption. This is a wonderful way to ease the financial strain of those first precious months.

Think of this as a little "baby bonus" from your future self. It’s for those countless diapers, late-night feedings, and the sheer joy of expanding your family. It’s a beautiful connection between your long-term savings and a truly momentous life event.

The "Oops, I Need It Now" Scenarios (Use with Caution!)

There are a few other less common but still important situations where penalty-free withdrawals are permitted. These are often tied to specific life circumstances that are beyond your control.

Disability Delight (Not Really, But You Get the Idea!)

If you become permanently disabled, you can withdraw funds from your IRA penalty-free. This is a crucial safety net for individuals facing such challenges. It acknowledges that financial stability is paramount when your ability to work is affected.

The "Not-So-Voluntary" Separation

If you separate from your employer during or after the year you turn age 55 (or age 50 for certain public safety employees), you can withdraw from your 401(k) or 403(b) without penalty. While this is specific to employer-sponsored plans, it's a valuable piece of information if you're planning a career change or early retirement.

The "Death and Taxes" (But Mostly Death) Clause

Sadly, if the IRA owner passes away, beneficiaries can typically withdraw the funds penalty-free, although they will likely still owe income tax on the distributions. This is a somber but necessary provision.

The Bottom Line: Your IRA, Your Life, Your Choices!

The beauty of an IRA is that it's designed to be a tool for your financial well-being throughout your life, not just at retirement. While the primary goal is long-term security, understanding these penalty-free withdrawal options can empower you to make smart decisions and seize opportunities.

So, take a moment to review your IRA. Are any of these situations on your radar? Knowledge is power, and in this case, it’s also the key to unlocking your savings for life's significant moments without the sting of penalties. It’s about building a life that’s both financially secure and rich with experience.

Don't let the fear of penalties hold you back from planning for the big moments. Explore your options, and remember that your IRA can be a flexible and valuable asset. Now go forth and plan your adventures! You might be surprised at how much more fun saving can be when you know the exciting possibilities it can unlock.