Whats The Minimum Credit Score To Buy A Car

So, you’re dreaming of that shiny new set of wheels, the one that’ll whisk you away on spontaneous weekend adventures or just make that soul-crushing commute feel a little less… soul-crushing. Awesome! But before you start picturing yourself cruising down the highway with the wind in your hair (or what’s left of it!), there’s a little hurdle to hop over: your credit score. And you might be wondering, “What’s the magic number, the golden ticket, the secret handshake that unlocks the door to car ownership?”

Let's dive into the wonderful world of credit scores and car buying, and I promise, it won't be drier than a week-old baguette. We’re talking about the minimum credit score to buy a car, and it’s not quite as scary as a dragon guarding a hoard of gold. Think of it more like a friendly greeter at a fancy, but approachable, party. Everyone’s invited, but some folks get the VIP treatment!

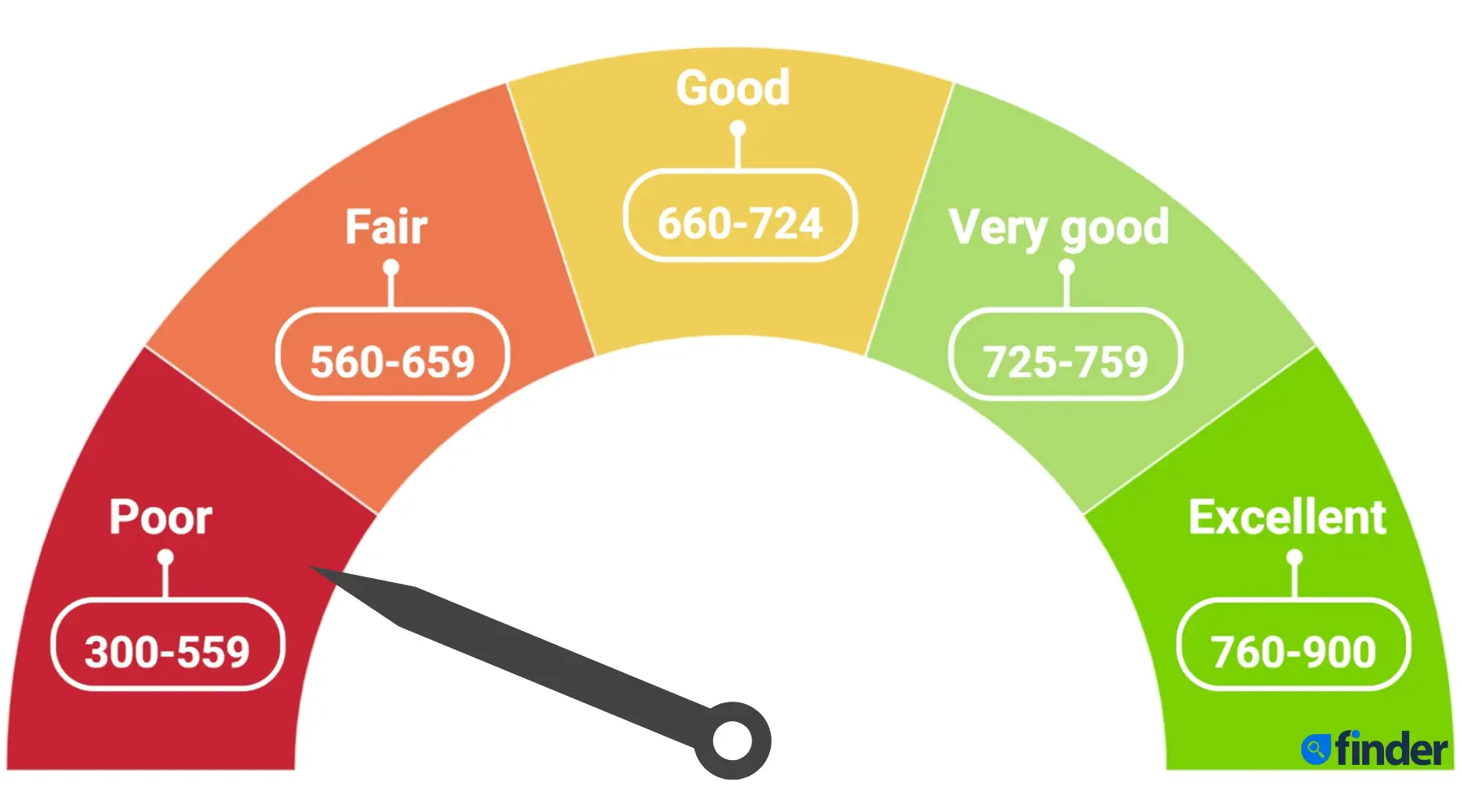

Now, there’s no single, universally set "minimum score" that applies to every single dealership, every single lender, and every single car on the planet. It’s more like a spectrum, a kaleidoscope of possibilities depending on who you’re dealing with and what kind of loan you’re after. But, to give you a ballpark, a generally accepted range for getting approved for a car loan, without needing a cosigner or a small miracle, often hovers around the 600 mark. Yes, 600! If your score is sitting comfortably above that, you’re likely in a pretty good position.

Think of your credit score like your financial report card. A high score means you’ve been acing your financial classes, paying bills on time, and generally being a responsible borrower. A lower score might mean you’ve had a few detours, maybe a missed payment here or there, or perhaps you’re new to the whole credit game. Both are okay! It just affects the kind of car loan you’ll get and, importantly, the interest rate you’ll be offered. That’s the big one, folks!

If your score is in the excellent range (740 and above), congratulations! You’re practically a financial superhero. You’ll likely qualify for the best interest rates, which means you’ll save a boatload of money over the life of your loan. It’s like getting a discount at the world’s most exclusive (and affordable) car boutique. You can walk in, flash your stellar score, and the dealership will practically roll out the red carpet. They’ll be fighting over who gets to help you!

Now, if your score is in the good range (around 670-739), you’re still looking pretty darn good. You’ll get approved for a loan, and your interest rates will be competitive. You’re the reliable friend who always shows up on time, and the bank appreciates that. You’ll still be able to get a sweet ride without breaking the bank.

What about the fair range (around 580-669)? This is where things start to get a little more… interesting. You can still get a car loan, but your interest rates might be a bit higher. Think of it as needing a little extra convincing to the bank. It’s like bringing a really good, but slightly less dazzling, appetizer to a potluck. It’s welcomed, but maybe not the star of the show. You might need to put down a larger down payment to sweeten the deal for the lender. This is where a little planning can go a long way. Saving up a bit extra for that down payment can make a huge difference in your monthly payments and the overall cost of your car.

And then there’s the situation where your score is below 580. This is where it gets a bit more challenging, but please, don’t despair! It’s not the end of your car-buying dreams. It just means you’ll likely be looking at subprime car loans. These loans come with higher interest rates and potentially shorter repayment terms. It’s like trying to get into that exclusive party when you’re a little late and not quite dressed for the occasion. You might still get in, but you might have to pay a little extra for the privilege, and the bouncer might be a bit more scrutinizing. Some dealerships specialize in working with buyers who have lower credit scores, and they might offer in-house financing. This can be a lifesaver, but always, always read the fine print. Understand all the terms and fees before you sign anything!

Remember, buying a car is a marathon, not a sprint. Even if your credit score isn't where you want it to be right now, there are steps you can take to improve it. Paying your bills on time, reducing your debt, and checking your credit report for errors are all fantastic ways to boost your score. It might take a little time and effort, but the payoff is enormous. Imagine the satisfaction of driving off in your new car, knowing you achieved it through smart financial moves. That’s a feeling better than finding a forgotten twenty-dollar bill in your pocket!

So, what’s the minimum credit score? It's not a rigid rule, but a guiding star. Aim for 600 and above for smoother sailing, but even if you’re below that, don't throw in the towel. With a little research, a smart approach, and maybe a bit of patience, that dream car is still within reach. Happy car hunting!