What's The Best Bank To Open A Business Account

Alright, so you've finally done it. You've taken the plunge, brewed the coffee, stared longingly at your bank account balance and thought, "You know what? This is getting serious. It's time to make it official. It's time to open a business account." Congratulations! That's a huge step, like finally deciding to put your socks away in the drawer instead of the "maybe later" pile on your chair. But now comes the slightly less glamorous, but equally important, part: figuring out which bank is going to be your new financial wingman.

Picking a bank can feel a bit like choosing a favorite pizza topping. Everyone has their opinions, and what works for your buddy Brenda (who swears by anchovies, bless her adventurous soul) might just make you want to run for the hills. We've all been there, right? Standing in front of a wall of bank logos, feeling a bit like a kid in a candy store, but instead of sugary delights, you're faced with interest rates and monthly fees. It's enough to make you want to just stick with your personal checking account and hope nobody notices you're using it to sell artisanal dog treats.

But fear not, fellow entrepreneur! This isn't rocket science. It's more like figuring out how to assemble IKEA furniture without losing your sanity – a challenge, yes, but entirely doable with the right approach. Think of your business account as the trusty steed that will carry your entrepreneurial dreams to glory. You don't want a nag that's going to throw you off at the first sign of a bump in the road, do you? You want something reliable, something that understands your quirks, and maybe even throws in a little extra sparkle now and then.

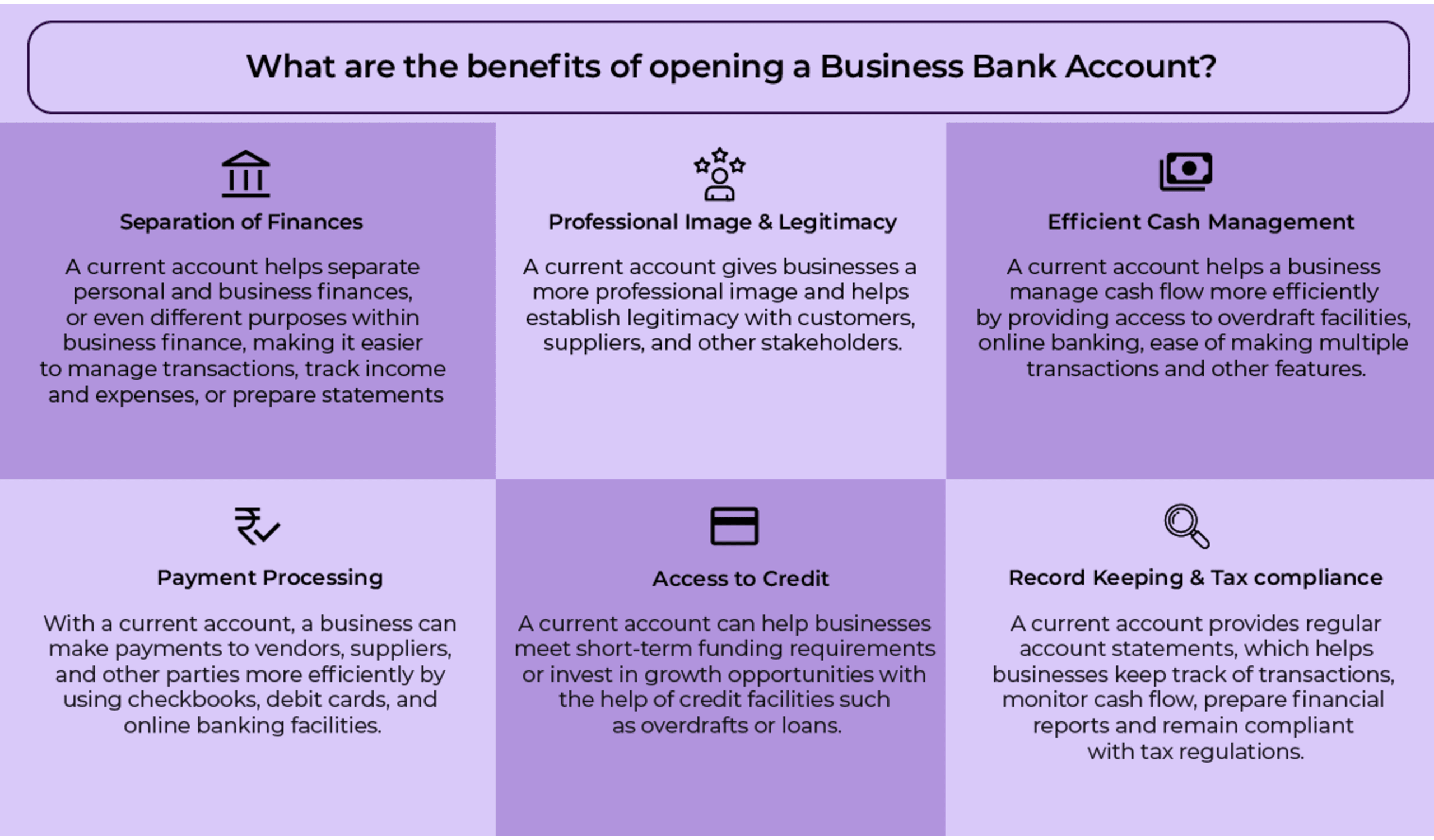

So, what makes a bank "the best" for your budding empire? It's not just about the flashiest brochures or the tellers with the most dazzling smiles (though a friendly face never hurt anyone, especially when you're depositing that first big check!). It’s about finding a place that understands the rhythm of your business, the ebb and flow of your cash, and the fact that sometimes, you’ll need to transfer money at 3 AM because inspiration (or a desperate supplier) struck.

Let's break it down, shall we? Think of it like this: you’re not just opening an account; you’re forging a relationship. And like any good relationship, it needs to be built on trust, communication, and a shared understanding of what makes you tick. Your business banking needs are unique, just like your secret ingredient for that award-winning chili. So, instead of blindly following the herd, let's explore what you actually need.

The Big Three: What to Look For

When you’re scanning the financial horizon, you’ll notice a few key things that tend to pop up. These are the bread and butter of business banking, the foundational elements that will either make your life a breeze or a constant headache. Let’s dive in!

Fees, Glorious Fees! (Or Lack Thereof)

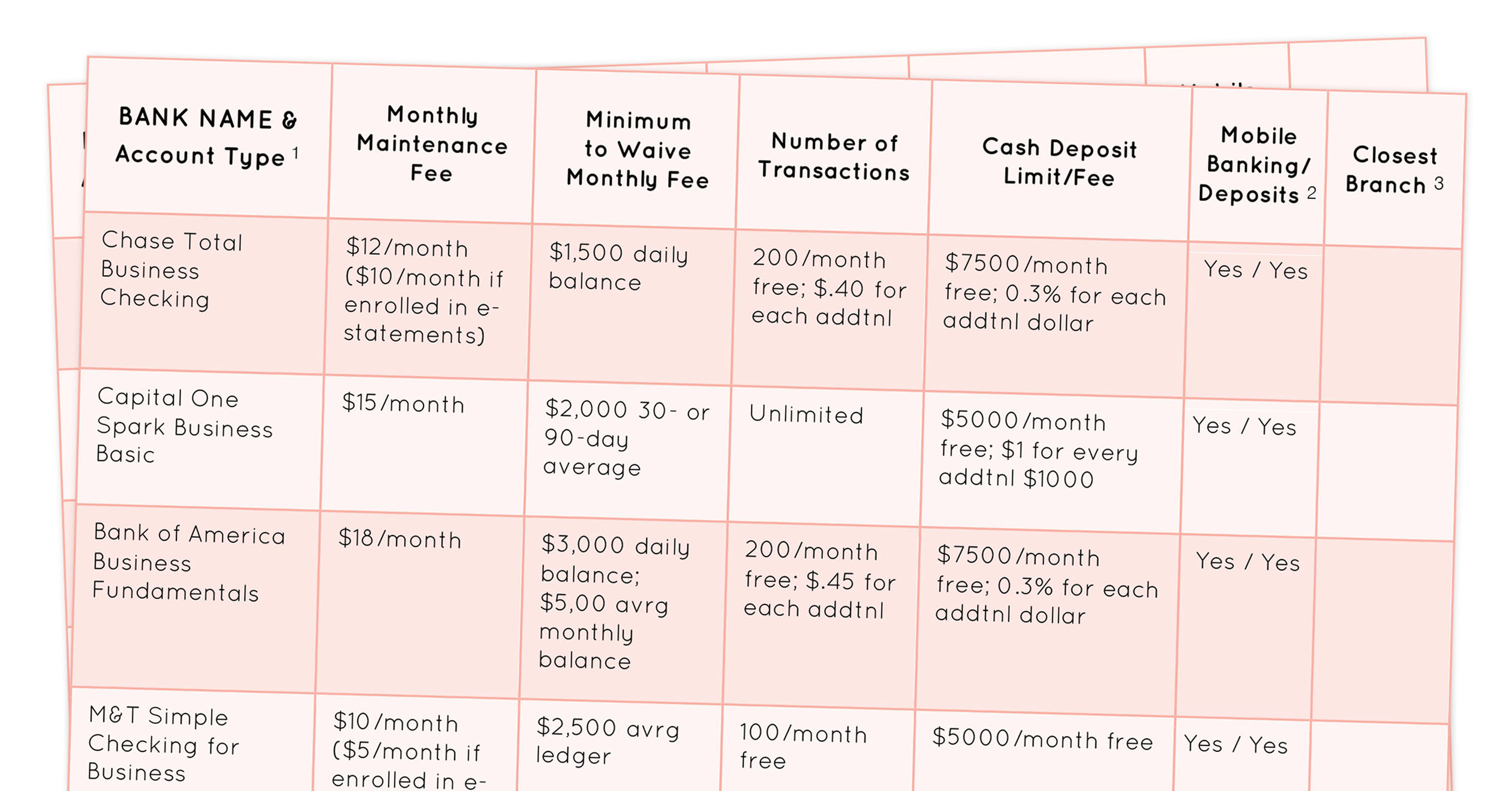

Ah, fees. The bane of our financial existence. It’s like finding an extra wrinkle in your favorite shirt right before a big meeting. Nobody likes them, but they’re often unavoidable. However, when it comes to business accounts, some banks are more fee-happy than a squirrel with a nut hoard. You’ll want to look for accounts with low or waived monthly maintenance fees. Many banks will waive these if you maintain a certain minimum balance, which, let's be honest, is often easier said than done when you're just starting out.

Then there are the transaction fees. This is where things can get sneaky. Are you making a lot of deposits? A lot of withdrawals? Do you need to send money internationally? Each of these actions can come with a price tag. Some banks offer a set number of free transactions per month, which is a lifesaver. Others charge per transaction, and it can add up faster than you can say "profit margin." Imagine handing over a dollar for every single latte you buy – that’s what per-transaction fees can feel like for your business!

And don’t forget the overdraft fees. Nobody intends to overdraw their account, but sometimes life happens. Maybe a crucial client pays a week late, or you accidentally buy enough glitter for a small nation. You want a bank that offers reasonable overdraft protection options, or at least doesn’t charge you the equivalent of a small ransom if you slip up. It’s like having a safety net that doesn’t have gaping holes in it.

Online and Mobile Banking: Your Digital Sidekick

In today’s world, if a bank doesn't have a decent online and mobile banking platform, they might as well be offering fax machines as their primary communication method. This is non-negotiable. You need to be able to check your balance, transfer funds, pay bills, and deposit checks (yes, with your phone!) without having to physically trek to a branch. Think about it: you’re out at a market, you just sold your masterpiece, and you need to send an invoice now. You don't want to be fumbling around looking for a Wi-Fi hotspot and praying the website loads.

A good online platform is intuitive, fast, and secure. You should feel confident managing your money on the go. Does it have a clunky interface that makes you feel like you’re navigating a 1990s video game? That’s a red flag. Does it offer real-time alerts for transactions or low balances? That’s a gold star. It’s your digital command center, so make sure it’s user-friendly and empowering. It's the difference between a helpful assistant and a demanding boss.

Customer Service: The Human Touch

This is where it gets personal. While online banking is crucial, sometimes you just need to talk to a real human being. Maybe you have a complex question, a weird error, or you’ve just had a truly awful day and need to vent (politely, of course). How does the bank handle this? Are their customer service lines notoriously long? Are the representatives knowledgeable and helpful, or do they sound like they’re reading from a script written in ancient Sumerian?

For small businesses, this is especially important. You're not a faceless corporation; you're a person with a dream. You want a bank that treats you like you matter. Some banks offer dedicated business bankers who can get to know your specific needs and offer tailored advice. This is like having a financial fairy godmother who can wave her wand and solve your money woes. Others just throw you into the general queue, which can be frustrating when you’re on a tight deadline.

The Contenders: Where to Look

Now that we know what we’re looking for, let’s talk about who’s in the running. The banking landscape can seem vast, but there are a few main players that tend to dominate the small business scene.

The Big Guys: Established and Reliable

Think of your national banks – the ones you see on every corner, with their familiar logos and decades of history. These banks often have a wide range of services, from basic checking and savings to more complex business loans and lines of credit. They also tend to have a vast network of branches, which can be convenient if you still value face-to-face interactions or need to handle cash deposits regularly.

The upside? Stability and a comprehensive suite of tools. The downside? They can sometimes be a bit more bureaucratic. Their fee structures might be less flexible, and their customer service can feel a bit… corporate. It’s like dating someone who’s incredibly successful and stable, but maybe not the most spontaneous partner.

Examples include Chase, Bank of America, Wells Fargo. These are the dependable workhorses of the banking world. They’ve been around the block, seen it all, and can probably handle most of your business needs without breaking a sweat. Just be prepared to navigate their systems and understand their fee schedules like you’re studying for a final exam.

The Online Innovators: Convenience at Your Fingertips

Then you have the newer, digitally-focused banks. These guys are all about sleek interfaces, lightning-fast apps, and minimal overhead. They often offer extremely competitive fee structures, sometimes even with no monthly fees and unlimited free transactions. They’re the tech-savvy friends who are always up-to-date with the latest gadgets and trends.

The upside? They’re often incredibly cost-effective and incredibly convenient for digital natives. You can manage everything from your phone, and they’re usually great at integrations with other business software. The downside? Fewer (or no) physical branches. If you deal with a lot of cash or need in-person support for complex issues, this might not be your ideal setup. It’s like having a brilliant online tutor who can teach you anything, but can’t help you tie your shoes.

Examples include Novo, Bluevine, Mercury. These are the up-and-comers, the rebels with a cause (the cause being easier, cheaper banking). They’re perfect if your business is predominantly online, or if you’re comfortable handling most things digitally. You’ll likely save a bundle on fees, and their apps are usually a joy to use.

Local Stars: The Community Champions

Don’t forget about your local credit unions and community banks! These institutions are often deeply invested in the success of businesses in their area. They might not have the glitzy apps of the online banks or the national reach of the big players, but they often excel in personalized customer service and a genuine understanding of the local market.

The upside? You can often build strong relationships with your bankers, and they might be more willing to work with you on unique situations. They’re the friendly neighbors who are always willing to lend a hand. The downside? Their technology might not be as cutting-edge, and their branch network can be limited. It’s like having a favorite local diner – the food is amazing and the staff knows your order, but you can’t get it delivered across the country.

Examples include your local credit union or a smaller regional bank. These are the unsung heroes of the banking world. They might not be as well-known, but they can offer a level of personal attention and community support that the larger banks simply can’t match. If you value a human connection and supporting local businesses, these are definitely worth exploring.

Making Your Choice: The Decision-Making Process

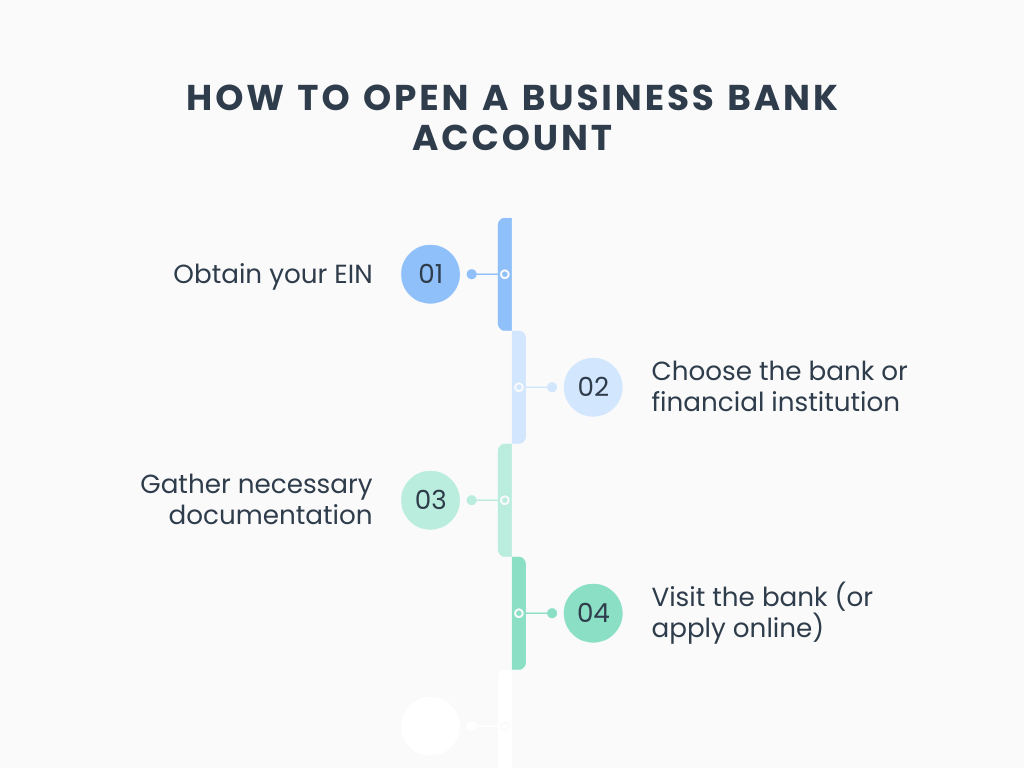

So, how do you actually pick? It’s not about finding the one perfect bank that fits everyone. It’s about finding the one that fits you. Here’s a little roadmap to guide your decision:

1. Assess Your Business Needs

Before you even look at a bank’s website, sit down and think about your business. This is your business plan, but for banking! * How much cash do you expect to handle? If it's a lot, you’ll need good cash deposit options. * How many transactions do you anticipate? This will inform your fee tolerance. * Do you need international wires? Some banks are better (and cheaper) than others. * What kind of technology do you rely on? Do you need integrations with accounting software?

Seriously, grab a notebook and jot this down. It’s like making a list for a grocery run – you don’t want to forget the milk (or the credit card processing integration). * Are you a freelancer sending out invoices every other day? You’ll need easy invoicing and low transfer fees. * Are you a brick-and-mortar shop that deals with a lot of physical cash? Branch access and deposit limits will be key. * Are you an e-commerce whiz that sells globally? International transaction fees and exchange rates will matter.

2. Do Your Research (But Don't Get Overwhelmed!)

Once you know what you need, start comparing. Look at the websites of a few banks from each category (big national, online innovator, local). Pay close attention to their business checking account pages. Look for the fine print – the fee schedules are often hidden in PDFs that look like they were designed by accountants who moonlight as origami artists.

Don't be afraid to call their business banking departments. Ask specific questions. "What's the fee for an outgoing wire transfer?" "What's your policy on returned items?" Their answers, and how quickly they give them, can tell you a lot about their customer service. It’s like test-driving a car – you want to kick the tires, open the trunk, and see how it handles.

3. Read Reviews (But Take Them with a Grain of Salt)

Online reviews can be helpful, but remember that people are often more motivated to complain than to praise. If you see a pattern of complaints about a specific issue (e.g., long hold times, hidden fees), take note. But also look for positive reviews that highlight things you care about, like responsive customer service or helpful business features.

Think of it as getting advice from friends. One friend might rave about a new restaurant, while another might complain about the service. You take both pieces of information and make your own judgment. It’s good to hear both the raves and the rants.

4. Consider the Future

What are your growth plans? Will the account you choose today still be suitable in a year or two? Some accounts have tiered features that unlock as your business grows. Others might have limitations that will quickly become restrictive.

It’s like choosing a starter home. You want something that’s perfect for now, but also has the potential to grow with you. You don't want to be looking for a new bank every six months. Think about whether the bank offers things like business loans, merchant services, or payroll processing, which you might need down the line.

The Bottom Line: It's Your Call!

Ultimately, the "best" bank for your business account is the one that makes your life easier, supports your financial goals, and doesn't nickel-and-dime you to death. It's the bank that feels like a partner, not just a service provider. It’s the bank that lets you focus on what you do best – building your amazing business – without constantly worrying about your money.

So take a deep breath, do your homework, and trust your gut. Whether you go with a big, stable institution, a nimble online disruptor, or a friendly local credit union, the most important thing is that you’ve taken that crucial step. Now go forth and conquer the business world, one well-managed bank account at a time!