What Is The Difference Between And Ira And A 401k

Alright, settle in, grab your metaphorical latte, and let’s talk about money. Not the ‘where’d my paycheck go?’ kind of money, but the ‘how do I not live on ramen noodles when I’m 80?’ kind of money. We’re diving into the wild, wonderful world of retirement accounts, specifically the notorious duo: the IRA and the 401(k). Think of them as cousins in the savings family – related, but with very different personalities. And maybe one of them is a little more prone to wearing a fanny pack.

So, what’s the deal? Why are there two (and a million other acronyms that sound like robot names)? Well, it boils down to who’s offering them and how they work. Let’s break it down, shall we? Imagine you’re at a buffet of financial freedom. The 401(k) is like the employer-provided buffet. It’s convenient, often comes with a special sauce (more on that later), and you don’t have to do too much digging to get your plate filled.

The 401(k): Your Work Buddy with a Wallet

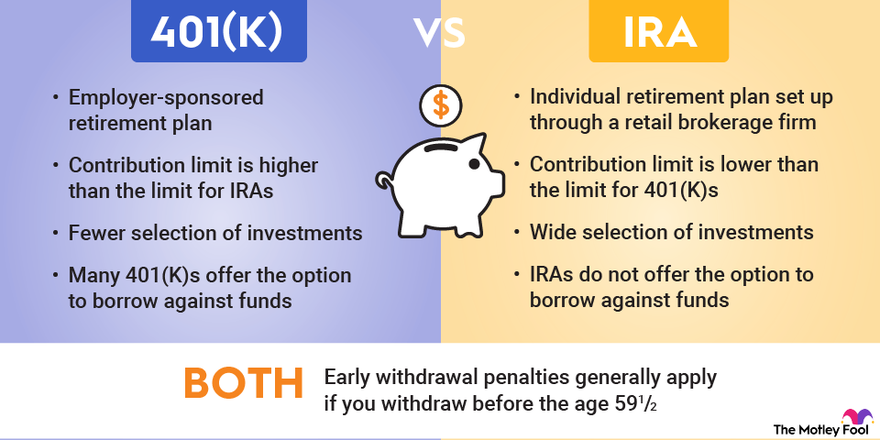

The 401(k) is almost always tied to your job. Your employer sets it up, and you, my friend, can decide to contribute a portion of your paycheck directly into it. It’s like having a tiny, tax-advantaged piggy bank living inside your employment contract. Pretty neat, right?

Now, the real magic of a 401(k) often comes in the form of employer matching. This is where your boss basically says, “Hey, you’re saving for your future? That’s awesome! Here, have some of my money too!” It’s like finding an extra fry at the bottom of the bag – a delightful surprise. Some employers will match you dollar-for-dollar up to a certain percentage of your salary. This is essentially free money, people! Seriously, not taking advantage of employer matching is like leaving a perfectly good slice of cake on the table at a birthday party. A cardinal sin, in my book.

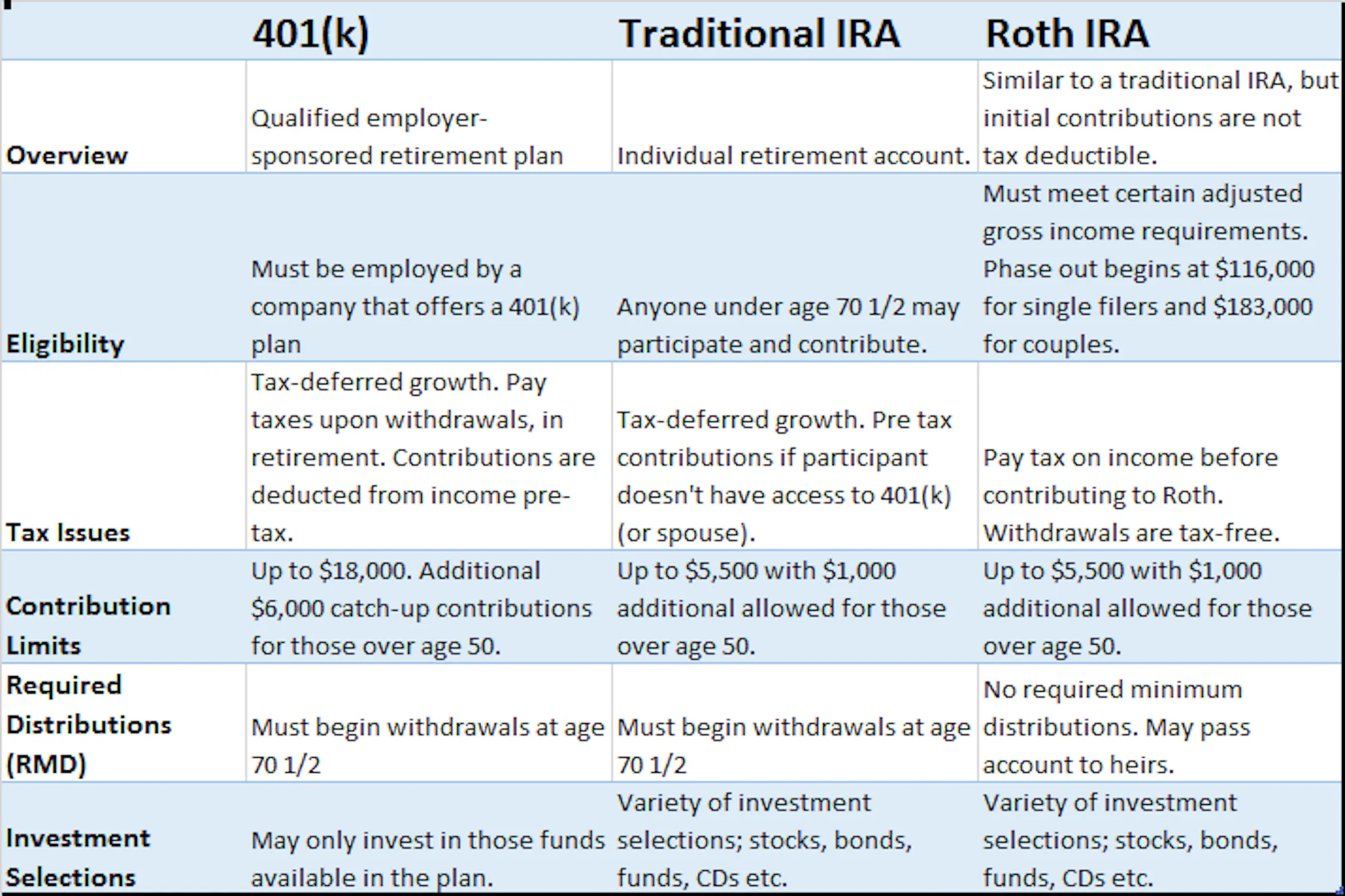

There are two main flavors of 401(k)s: the Traditional and the Roth. In a Traditional 401(k), your contributions are typically made before taxes are taken out. This means your taxable income is lower now, giving you a bit of a break today. But, and here’s the kicker, when you eventually retire and start taking money out, those withdrawals are taxed. It’s like getting a present now, but you have to pay for the wrapping paper later.

Then there’s the Roth 401(k). With this one, you contribute money that’s already been taxed. The big payoff? Your qualified withdrawals in retirement are completely tax-free. Imagine a magic money tree that grows money you never have to declare on your taxes. It’s pretty sweet, especially if you think you’ll be in a higher tax bracket in retirement than you are now.

The downside to 401(k)s? They’re tied to your employer. If you switch jobs, your 401(k) usually has to come with you. You’ll have to decide whether to roll it over into your new employer’s plan, roll it into an IRA (more on that in a sec!), or cash it out (which, trust me, you generally don’t want to do because taxes and penalties are usually involved. It’s like trying to escape a fun party and the bouncer makes you pay a fine to leave). Also, the investment options within a 401(k) are often limited to what your employer chooses. Sometimes it's a decent selection, other times it feels like picking between beige, off-white, and a slightly different shade of beige.

The IRA: Your Independent Retirement Sidekick

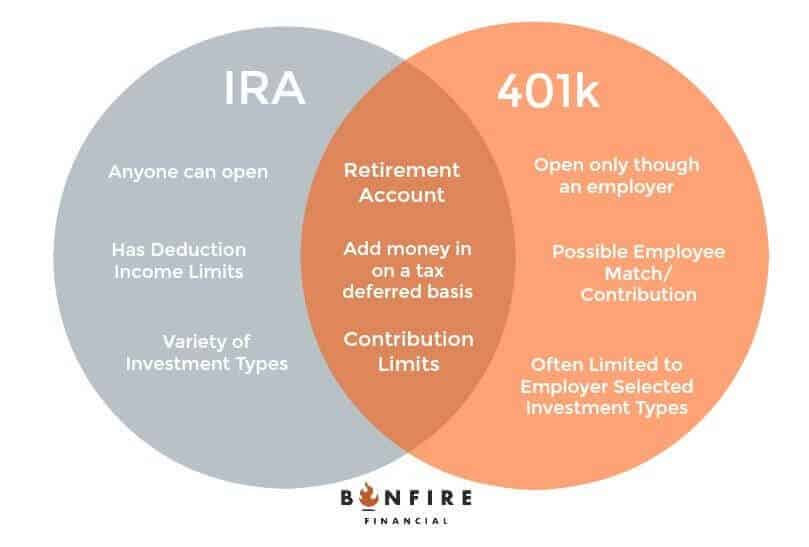

Now, let’s talk about the IRA, or Individual Retirement Arrangement (or Account, depending on who you ask). This is your personal, do-it-yourself retirement savings account. It’s not tied to your employer, which means you are in the driver’s seat. Think of it as your own private financial superhero, ready to leap into action whenever you decide.

IRAs come in two main flavors, much like their 401(k) cousins: the Traditional IRA and the Roth IRA.

The Traditional IRA is similar to the Traditional 401(k). You can potentially deduct your contributions on your taxes now, lowering your current tax bill. Again, the money grows tax-deferred, and you pay taxes on it when you withdraw it in retirement. This can be a good option if you’re in a higher tax bracket now and expect to be in a lower one later. It’s like getting a discount when you buy your groceries, and then paying the full price for the delicious meal you cook later.

The Roth IRA, on the other hand, is where things get really interesting for many people. You contribute money that’s already been taxed. The magical part? Qualified withdrawals in retirement are completely tax-free. This is the dream for many, especially younger folks who might be in a lower tax bracket now. Imagine all that investment growth, and you never owe a single penny in taxes on it. It’s like finding a secret backdoor to a tax-free vacation island.

A surprising fact: there are income limitations for contributing directly to a Roth IRA. If you earn too much, you might not be able to put money in directly. But don't despair! There are “backdoor Roth IRA” strategies that can still get your money into that tax-free haven. It’s like finding a secret handshake to get into an exclusive club. (Disclaimer: always consult a financial professional for these strategies, don’t just wing it like I might at karaoke.)

The beauty of an IRA is its flexibility. You can open one at pretty much any brokerage firm, and you often have a much wider range of investment choices than you’d find in a typical 401(k). Think stocks, bonds, mutual funds, ETFs – you can build a portfolio that’s as unique as your taste in socks.

When you leave a job with a 401(k), you can roll that money over into an IRA. This gives you more control over your investments and can sometimes lead to lower fees. It’s like taking your superhero from the company cafeteria to your own private headquarters, where they can really let loose.

The Nitty-Gritty: Key Differences

So, to recap the main differences, like a well-organized recipe card:

- Employer vs. Individual: The 401(k) is employer-sponsored; the IRA is opened by you.

- Matching: 401(k)s often have employer matching (free money!); IRAs do not. This is a HUGE deal.

- Contribution Limits: 401(k)s generally have much higher annual contribution limits than IRAs. This means you can squirrel away more money in a 401(k) if you have the cash.

- Investment Options: IRAs typically offer a broader range of investment choices. 401(k)s are usually limited to a pre-selected menu.

- Income Restrictions: There are no income limits to contribute to a Traditional 401(k). Roth IRAs, however, have income limitations for direct contributions.

Think of it this way: a 401(k) is a powerful tool provided by your employer, often with a built-in incentive (that match!). An IRA is your personal, versatile savings vehicle that you control completely. Many people benefit from having both. It’s like having a superhero sidekick and a superhero mentor.

Ultimately, the best choice (or combination of choices) for you depends on your personal financial situation, your income, your employer’s offerings, and your retirement goals. Don’t let the acronyms scare you. These are simply tools to help you build a more secure and less ramen-noodle-filled future. So, go forth, understand your options, and start saving like your future self is high-fiving you from a tropical beach somewhere. Because, let’s be honest, that’s the goal, right?