What Is Needed For Mortgage Pre Approval

Hey there, future homeowner! So, you're thinking about diving into the wonderful world of mortgages and, more importantly, getting that magical piece of paper called pre-approval. High fives all around! It’s like getting a golden ticket to house hunting, and honestly, it makes the whole process a whole lot less stressful. Think of it as your financial superhero cape, ready to swoop in and tell sellers, "Yep, this person's serious!"

But before you start picturing yourself painting the nursery (or the man cave!), let's break down what you actually need to snag that pre-approval. Don't worry, it’s not rocket science, and we’ll keep it super chill. No need to bring out the dusty textbooks or have a panic attack. We're just having a friendly chat about getting you ready to find your dream pad.

So, what exactly is mortgage pre-approval? In a nutshell, it’s a lender’s preliminary commitment to lend you a certain amount of money for a home. They’ll peek at your finances and give you a ballpark figure of what you can afford. It’s not a guarantee, mind you, more like a super-strong suggestion based on what they see. It’s a HUGE step, though, because it tells sellers you’re not just dreaming, you’re actually in a position to buy.

Imagine you're going on a first date. Pre-approval is like doing your research beforehand. You know their likes, dislikes, and general vibe. This way, when you meet them (the seller!), you're confident and prepared. No awkward silences about your budget, right?

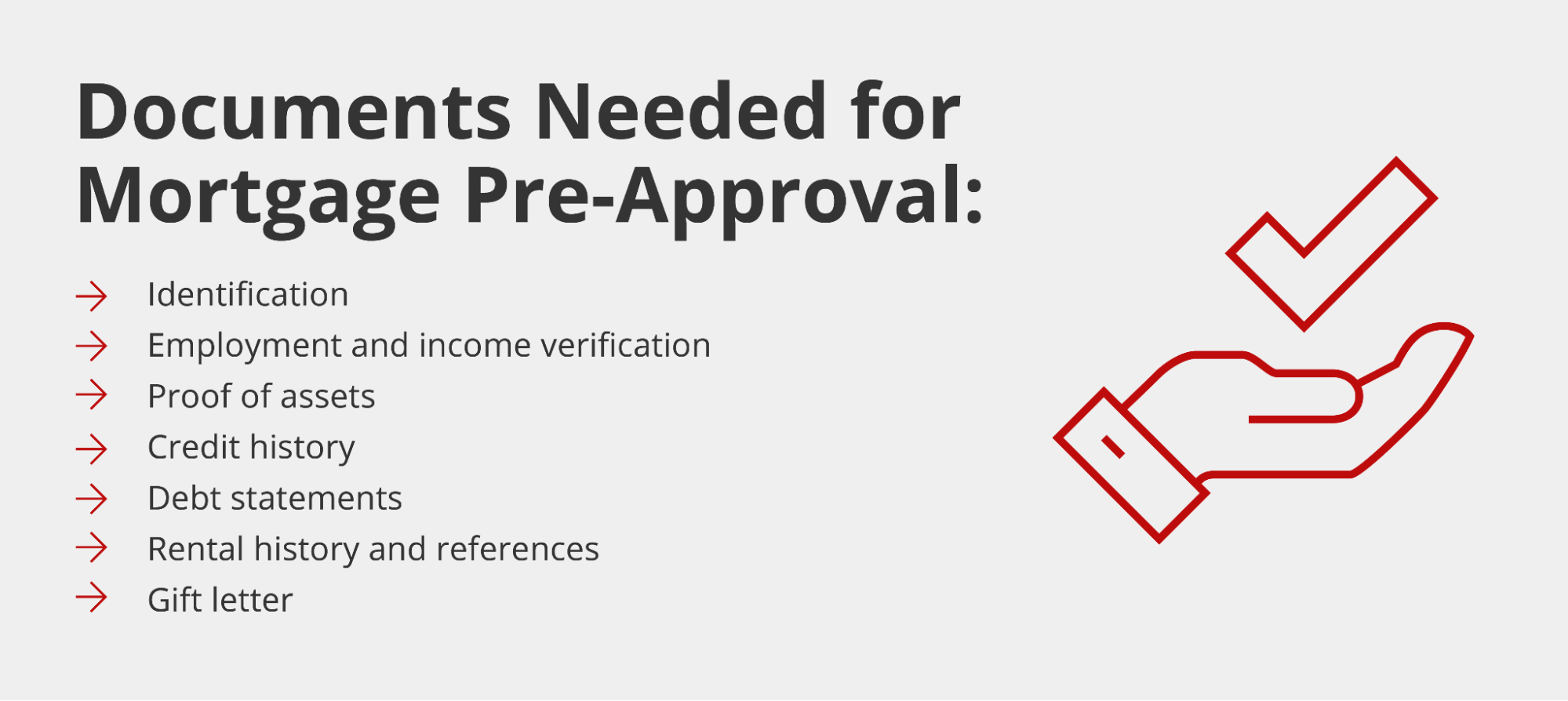

Now, let’s get down to the nitty-gritty. What documents are usually on the lender’s shopping list? Think of it as gathering your financial ID. They want to see the whole picture, so they can feel comfortable handing over a chunk of cash. And guess what? It's not as overwhelming as it sounds!

The Big Three: Income, Assets, and Debt

These are the pillars of your pre-approval quest. Lenders want to understand your ability to earn, your savings, and your existing financial obligations. It’s like building a sturdy house – you need a solid foundation!

1. Showing Off That Gorgeous Income

This is where you prove you’ve got the moolah coming in. Lenders want to see that your income is stable and sufficient to cover mortgage payments. And no, your passion for collecting vintage socks doesn't count as a verifiable income stream (sadly!).

Pay Stubs: They’ll likely ask for your most recent pay stubs, typically from the last 30 days. This shows your current earnings. If you’re paid weekly, they might want four stubs. If bi-weekly, two. Keep 'em handy!

W-2 Forms: These are your annual income statements from employers. They’ll usually want the last two years. This shows a consistent earning history. Think of it as your employment report card.

Tax Returns: Ah, the tax man cometh! Lenders will almost always request your federal tax returns for the past two years. This is super important, especially if you’re self-employed or have any other interesting income sources. It provides a broader look at your financial picture.

Self-Employed Folks, Unite! If you’re your own boss, you’ll likely need more documentation. This could include profit and loss statements, a balance sheet, and possibly even a year-to-date P&L. They want to be extra sure your business is thriving, not just surviving on caffeine and good intentions.

Other Income Streams: Got a side hustle? Rental properties? Alimony or child support (and it’s consistent)? Make sure to let your lender know and have documentation ready. They like seeing a diverse income portfolio! It’s like having a well-rounded investment strategy, but for your cash flow.

2. Flaunting Your Fabulous Assets

This is where you show off your savings and investments. Lenders want to see that you have funds for a down payment, closing costs, and a little cushion for emergencies. Think of these as your financial safety net. Nobody wants to buy a house and then immediately be eating ramen noodles every night, right?

Bank Statements: Get ready to share those checking and savings account statements. Lenders usually want the last two to three months. They’re looking for consistent deposits and to ensure large, unexplained sums haven’t just appeared out of thin air (unless you sold a kidney, which, please don't!).

Investment Accounts: If you have stocks, bonds, mutual funds, or retirement accounts (like a 401k or IRA), you’ll need statements for those too. They’ll want to see the current value. Just be aware that some lenders might discount certain investments a bit, so don't be surprised if they don't count the full market value of your beanie baby collection.

Gift Letters: Receiving a gift from family for your down payment? Awesome! You'll likely need a formal gift letter from the donor stating it's a gift and doesn’t need to be repaid. It’s a little formality, but it keeps things clean and above board.

Other Assets: Depending on the loan type, other assets like equity in other properties might be considered. But for standard pre-approval, bank and investment accounts are usually the main players.

3. Tackling Those Treasured Debts

This is where you show your lenders how you handle your existing financial obligations. They’re not just looking at how much you owe, but also at how reliably you pay it back. It's all about proving you're a responsible borrower. Imagine your debt is like a backpack you're carrying. They want to see that you can comfortably carry it without getting too weighed down.

Credit Report: This is a biggie! Your lender will pull your credit report to see your credit score and history. This is crucial. A good credit score shows lenders you're a reliable borrower who pays bills on time. If your score is a bit… meh, don't despair! There are ways to improve it.

Loan Statements: You’ll need to provide information on any outstanding loans. This includes:

- Mortgage Statements: If you currently own a home and have a mortgage, they'll want to see that.

- Auto Loan Statements: If you’ve got a car loan, they’ll need details.

- Student Loan Statements: Even if you're making minimal payments, they need to know about them.

- Personal Loan Statements: Any other installment loans.

Credit Card Statements: They'll want to see your most recent credit card statements, showing your current balances and minimum payments. They’re particularly interested in your credit utilization ratio (how much credit you’re using compared to your total available credit).

Alimony or Child Support Payments: If you’re obligated to pay these, you’ll need to provide proof of payment history. This is factored into your debt-to-income ratio.

The Nitty-Gritty Details (That Still Matter!)

Beyond the big three, there are a few other things lenders might poke around for. These are less about numbers and more about you!

Identification, Please!

Yes, they need to know who you are! This is standard procedure for any financial transaction.

- Government-Issued ID: Think your driver’s license or passport. Make sure it’s current and not expired. No one wants to be rejected because their ID looks like it belongs to a historical figure.

- Social Security Number: You’ll need your Social Security number to pull your credit report and for other background checks.

Employment Verification

They want to make sure your income source is legit and stable.

Employment History: You’ll likely need to provide a list of your employers for the past couple of years, including addresses and phone numbers. This allows them to do an employment verification call. So, be nice to your boss!

The Mystery of the Loan Estimate (Later On, But Good to Know!)

While not strictly for pre-approval, once you're under contract, you'll receive a Loan Estimate. This document outlines the terms of your mortgage, including your interest rate, monthly payment, and estimated closing costs. It’s super important to review this carefully!

What NOT to Do When You're Aiming for Pre-Approval

This is almost as important as knowing what to have! Think of it as avoiding common pitfalls on your path to homeownership.

- Don't Make Any Major Financial Changes: Seriously, hold off on buying that flashy sports car or taking out a new personal loan. Lenders like stability. A sudden influx of new debt or a huge purchase can seriously impact your pre-approval status. It's like trying to sneak a surprise cake into a diet – not a good idea!

- Don't Close Any Existing Credit Accounts: Even if you have a credit card you rarely use, don't close it! Closing an account can negatively affect your credit utilization ratio and your overall credit history. Leave those old friends where they are.

- Don't Forget to Be Honest: It might be tempting to fudge a number or two, but trust us, it will come back to bite you. Lenders have ways of finding out, and honesty is always the best policy. Plus, it saves you a lot of headaches down the line.

The "Pre-Approval" vs. "Pre-Qualification" Conundrum

Quick detour! You might hear the terms "pre-qualification" and "pre-approval" thrown around. While they sound similar, they’re not quite the same.

Pre-qualification is a more informal estimate. It's based on information you tell the lender, often without them verifying much. It gives you a rough idea, but it's not as strong as pre-approval.

Pre-approval is the real deal. It involves the lender actually verifying your income, assets, and credit. This is what sellers want to see!

So, aim for pre-approval. It’s worth the extra effort!

Wrapping it Up with a Smile

So there you have it! The essential ingredients for your mortgage pre-approval recipe. Gather your documents, be upfront and honest, and try to keep your financial life on an even keel during the process. It might seem like a lot of paperwork, but it’s truly a small price to pay for the excitement of finding your perfect home.

Think of this as your pre-game warm-up. You’re getting your team (your finances!) in the best shape possible before the big match (house hunting!). And once you have that pre-approval letter in hand, you’ll feel a sense of confidence and empowerment that’s absolutely priceless. You'll walk into open houses with a clear understanding of your budget, ready to fall in love with a place that’s truly you.

So, take a deep breath, grab your coffee (or your favorite relaxing beverage), and start gathering those documents. You’ve got this! And soon, you’ll be unlocking the door to your very own little slice of heaven. Happy house hunting, you amazing future homeowner!