What Does This Excerpt Describe The Federal Reserve System

Alright, gather ‘round, folks! Grab your lattes, ditch those spreadsheets for a sec, and let’s talk about something that sounds drier than a week-old baguette but is actually kinda… well, important. We’re diving into the mysterious depths of something called “The Federal Reserve System.” Sounds like a secret society for accountants, right? Or maybe a brand of fancy, artisanal bread? Nope, my friends, it’s the folks who, for better or worse, are the wizards behind the curtain of the U.S. economy.

Imagine you’re trying to throw a party. You want the music to be just right – not too loud, not too quiet. You need enough snacks, but not so many that you’re tripping over empty chip bags. You want people to have a good time, mingling and dancing, not nervously eyeing the exit. The Federal Reserve, or the “Fed” as its cool, casual pals call it, is kind of like the ultimate party planner for the entire country. Except instead of punch bowls and playlists, they’re dealing with… well, money. Lots and lots of money.

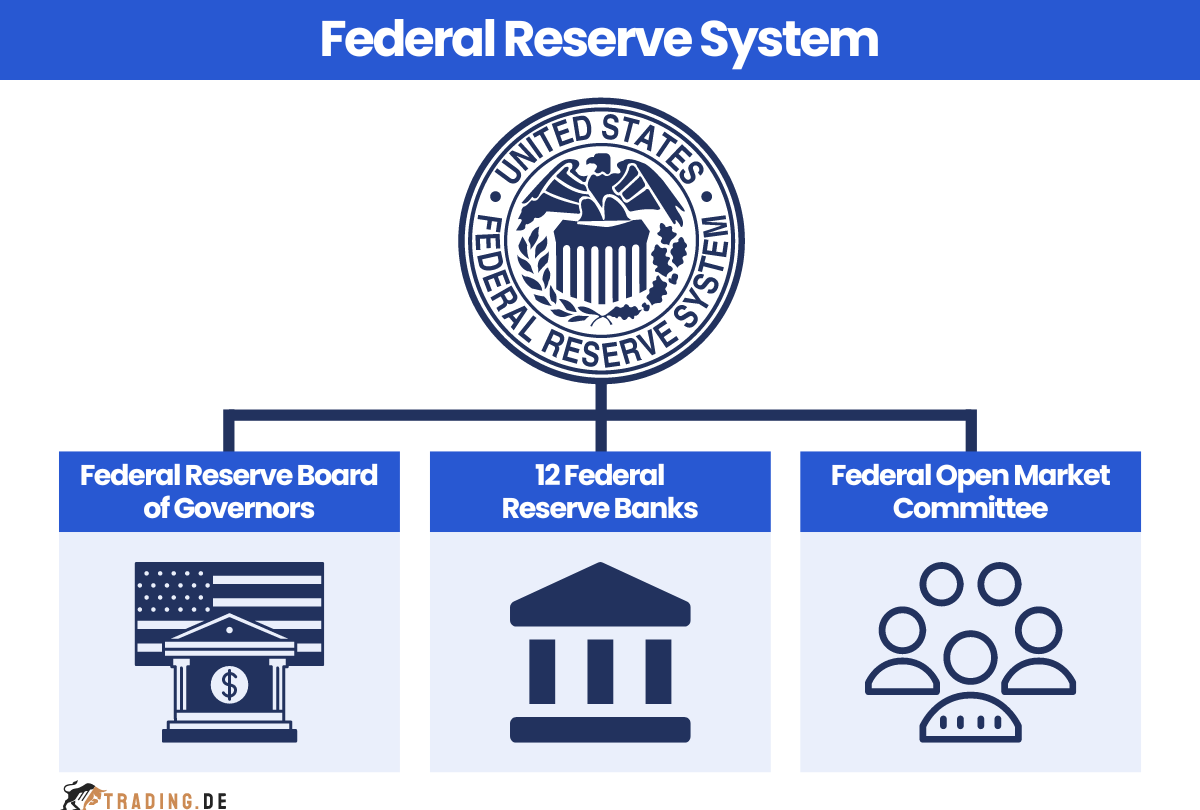

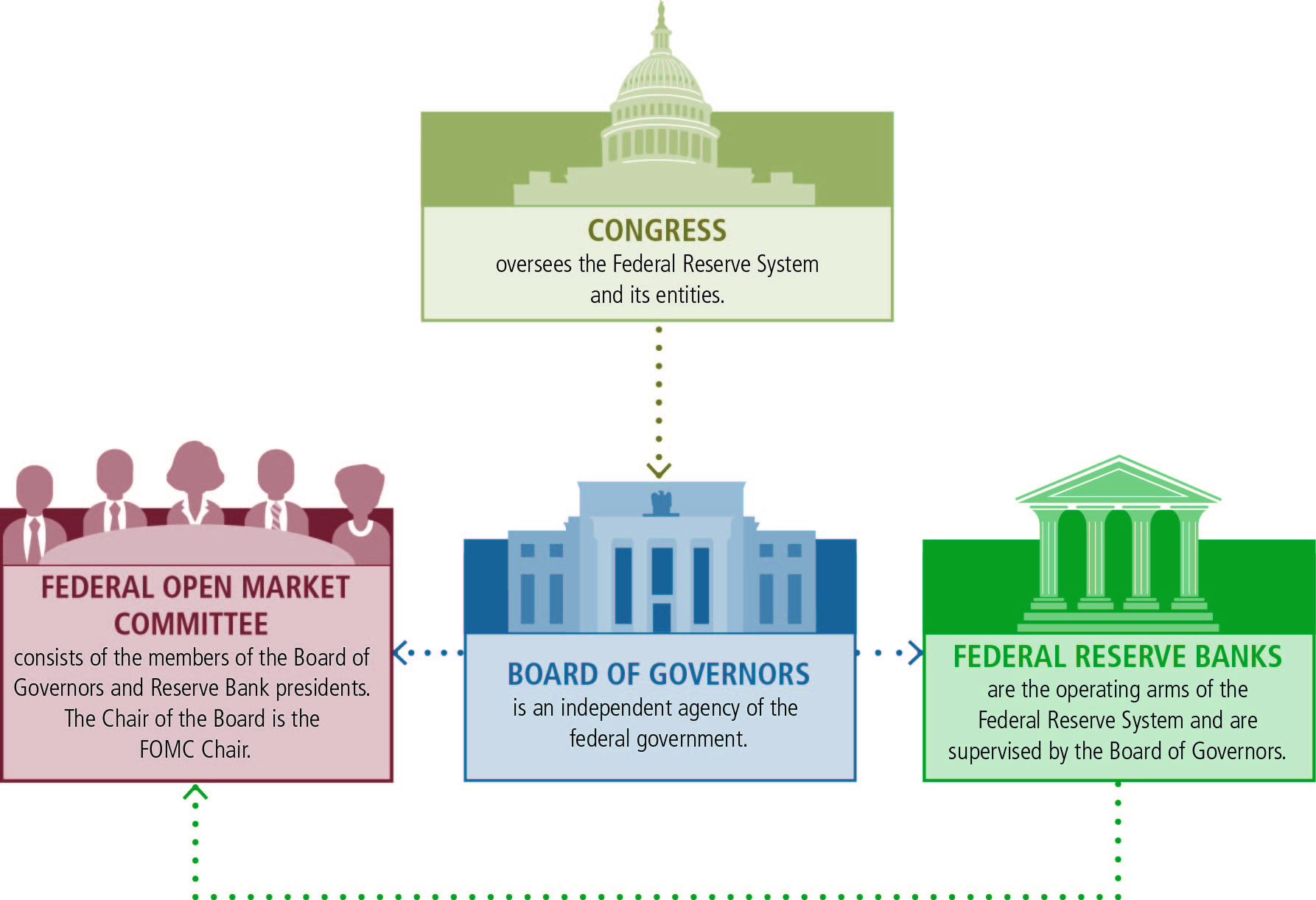

So, what exactly is this Federal Reserve System that gets its own little excerpt? Think of it as the central bank of the United States. It’s not a government agency in the traditional sense, though it’s overseen by Congress. It's more like a really, really old, very serious kid who got put in charge of the national piggy bank. They’ve got a few major jobs, and they’re all about keeping the economic party from going off the rails.

Job number one, and this is a biggie: keeping the economy humming along. They want jobs to be plentiful, businesses to be healthy, and for us regular folks to be able to, you know, buy groceries without selling a kidney. This is often referred to as their "dual mandate" – maximum employment and stable prices. Think of it as wanting everyone to have a job and for that job’s paycheck to actually buy stuff, not just turn into Monopoly money overnight. They try to steer the economy like a giant, slightly wobbly ship, trying to avoid hitting icebergs (recessions!) or sailing too fast into a hurricane (runaway inflation!).

Now, how do these financial maestros actually do this steering? They have a few nifty tools in their belt. One of the most talked-about is their ability to influence interest rates. Imagine interest rates as the price of borrowing money. If the Fed wants people to spend more and businesses to invest, they might lower interest rates. It’s like putting up a “Going Out of Business Sale” sign on borrowing costs – “Come on down, cheap loans await!” This can get more people buying houses, cars, and those fancy gadgets you’ve been eyeing. Who doesn’t love a good discount, especially on future debt?

On the flip side, if the economy starts overheating, like a pot of chili left on the stove too long, and prices start to skyrocket (that’s inflation, folks, and nobody likes their money losing its zing), the Fed can hit the brakes. They might raise interest rates. This makes borrowing more expensive, which can cool down spending and investment. It’s like the waiter coming over and saying, “Whoa there, slow down on the ordering, we’ve got a lot of hungry mouths to feed and the kitchen’s backed up!” It’s a delicate dance, and sometimes it feels like they’re trying to conduct a symphony with a bunch of toddlers.

Another cool trick they have up their sleeve is something called "open market operations." This sounds super intimidating, like something you’d see in a spy movie, but it’s actually pretty straightforward. The Fed can buy or sell government securities (think of them as IOUs from Uncle Sam) on the open market. When they buy these securities, they inject money into the banking system. It’s like they’re literally printing money (well, not exactly, but you get the idea) and handing it out to banks. More money in the system means more money available for loans, which can encourage lending and spending.

When they want to take money out of the system, they sell those securities. This sucks money back up, like a financial black hole. It's their way of controlling the money supply, ensuring there isn't too much cash sloshing around chasing too few goods, which, as we’ve established, is bad news for your wallet. They’re basically playing a giant game of financial Tetris, trying to fit the right amount of money into the economy without things collapsing.

The Fed also has a role in regulating banks. They’re the ones checking to make sure your local bank isn’t making wildly risky bets with your savings. Think of them as the strict but fair head librarian, making sure everyone’s following the rules and the library (the financial system) doesn’t go up in flames. They set rules about how much cash banks need to keep on hand (reserves) and generally keep an eye on their financial health. This is crucial for preventing bank runs, those chaotic moments when everyone rushes to pull their money out because they’re scared the bank will go belly-up. Nobody wants that kind of drama, especially not before their paycheck clears.

So, who’s in charge of all this finagling? The Fed is structured a bit like a decentralized empire. There’s the Board of Governors in Washington D.C., a bunch of really smart people appointed by the President and confirmed by the Senate. They’re like the council of elders. Then there are 12 regional Federal Reserve Banks scattered across the country. Each one serves its own district, kind of like regional managers who report back to the main office. They’re supposed to represent the interests of their local economies, which is a nice idea, right? Imagine if your neighborhood coffee shop had a direct line to the people deciding how much your latte costs!

And then there's the big kahuna, the ultimate decision-maker: the Federal Open Market Committee (FOMC). This is the group that actually decides on interest rates and other key monetary policy actions. It’s a powerful committee, and their meetings are watched by the entire financial world like it’s the season finale of a really intense reality show. When they speak, markets listen. Sometimes they’re like cryptic prophets, dropping hints that send stock markets soaring or plummeting. It’s a lot of pressure, like being the only one who knows the Wi-Fi password at a party.

It’s important to remember, though, that the Fed doesn’t have a magic wand. They can influence the economy, but they can’t control it perfectly. There are always outside factors, global events, and just plain old human behavior that can throw a wrench into their best-laid plans. They’re trying their best to navigate a complex, ever-changing landscape, armed with data, economic models, and a whole lot of caffeine.

So, the next time you hear about the Fed raising or lowering interest rates, or read a headline about their latest policy decision, you’ll have a slightly better idea of what’s going on. They’re the keepers of the economic keys, the wizards of interest rates, and the ultimate party planners for the nation’s finances. It’s a tough gig, but someone’s gotta do it, right? Now, if you’ll excuse me, I think I need another latte after all that talk of money and interest rates.