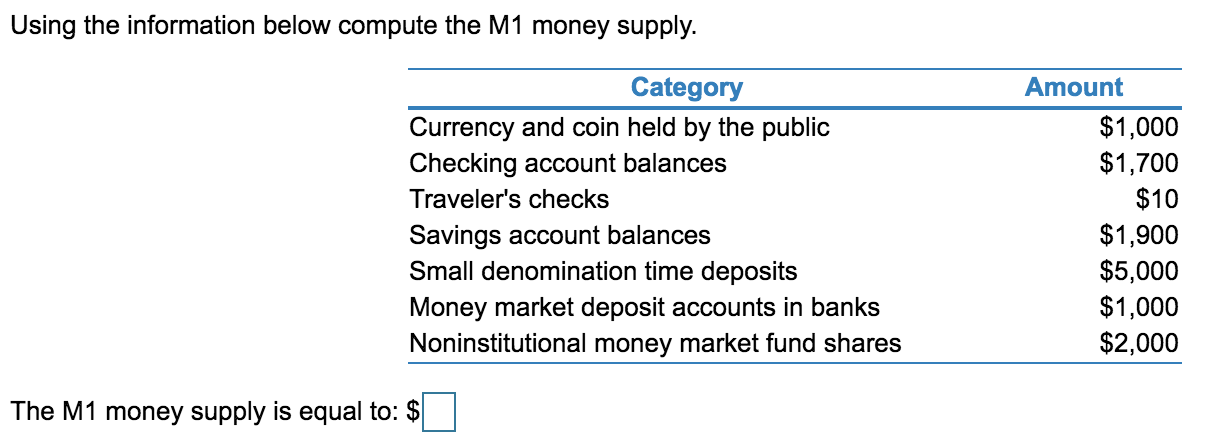

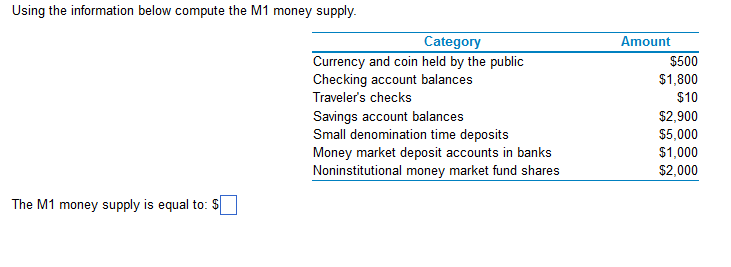

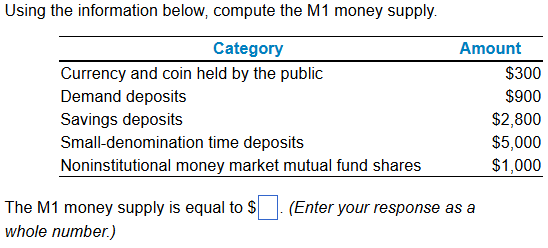

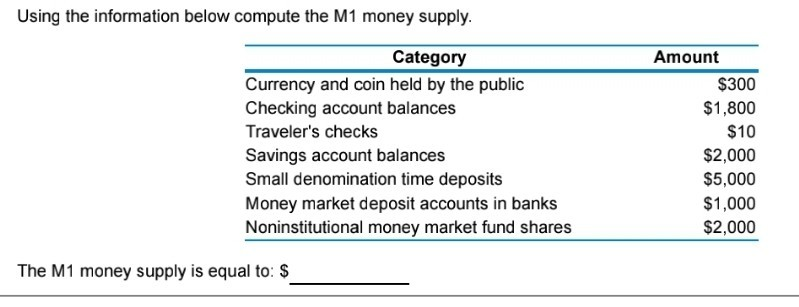

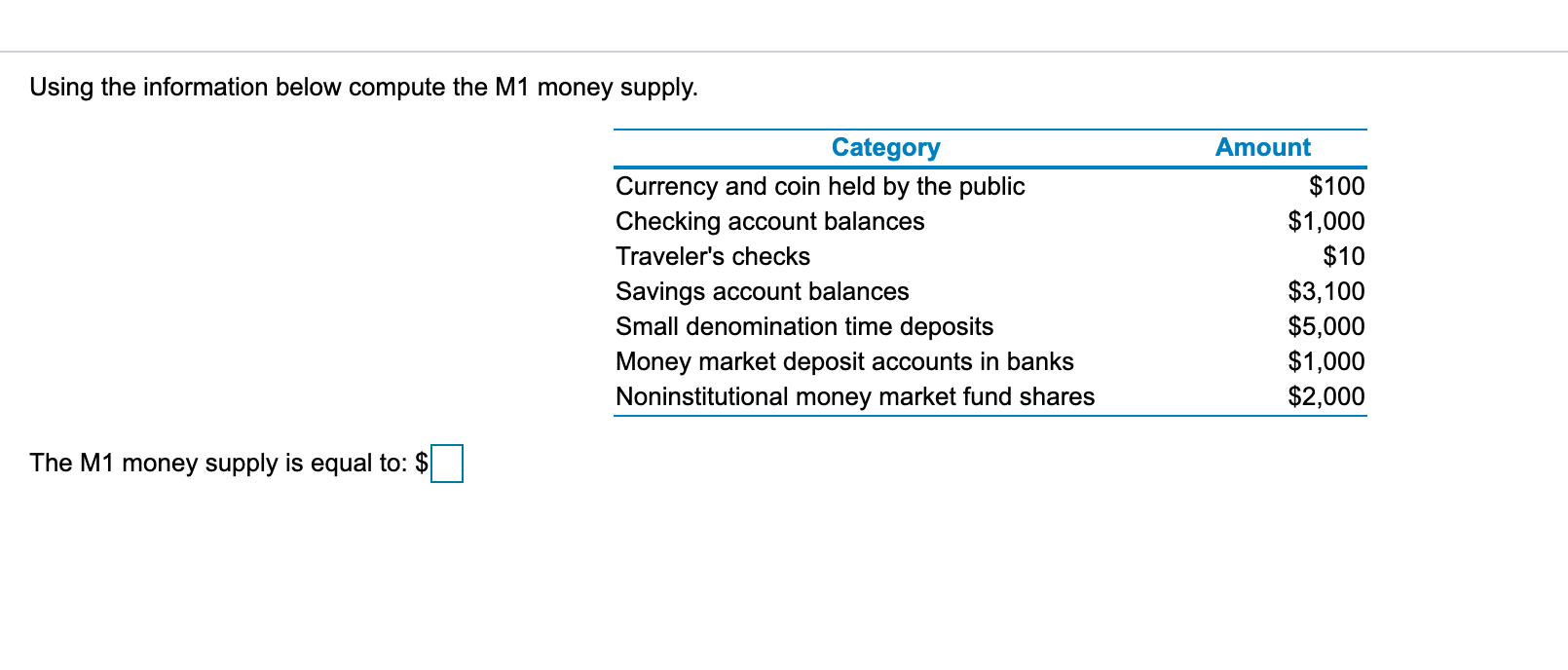

Using The Information Below Compute The M1 Money Supply

Hey there, curious minds! Ever wonder what all those fancy economic terms mean, like "money supply"? It sounds a bit intimidating, right? Like something only folks in suits with calculators understand. But honestly, it's not as complicated as it seems. In fact, understanding a little bit about the money supply can be pretty fascinating, and today, we're going to dip our toes into one specific part of it: the M1 money supply.

So, what exactly is the M1 money supply? Think of it as the most liquid money in our economy. Liquid means easy to spend, right? Like water flowing from a faucet, it's readily available. We’re talking about the cash you have in your wallet, the coins jingling in your pocket, and the money sitting in your checking account. This is the stuff you can whip out to buy your morning coffee, pay for that impulse book purchase, or send a quick Venmo to a friend.

Why should we even care about this? Well, the amount of money circulating in an economy has a big impact on… well, pretty much everything! It influences how much things cost (inflation!), whether businesses are hiring, and how healthy the economy is overall. So, understanding M1 is like getting a little peek behind the curtain of how our money world works.

Now, imagine you're trying to figure out how much money is "out there" for people to spend. It's not just about the physical cash printed by the government, is it? A huge chunk of it is digital, tucked away in our bank accounts. And that's where M1 comes in. It tries to capture all the money that's immediately spendable. Pretty neat, huh?

Breaking Down M1

Let's get a little more specific. What are the ingredients that go into this M1 pie? We've already touched on a couple, but let's make it official:

1. Currency: This is the physical stuff – the bills and coins. The coins in your couch cushions? Yep, that counts! The dollar bill you just pulled out of an ATM? Absolutely. This is the most tangible form of money we have.

2. Demand Deposits: This is the big one. These are the funds you have in your checking accounts. Why "demand" deposits? Because you can demand that money from your bank at any time. You write a check, use your debit card, or withdraw cash – the bank has to give it to you. It's like having a little money vault at the bank that you can access instantly.

3. Traveler's Checks: You might not see these as much anymore, but they're still technically part of M1. Think of them as pre-paid checks that were super popular for… well, travelers! They're designed to be safe and easy to use when you're away from home.

4. Other Checkable Deposits (OCDs): This category includes things like money market deposit accounts (MMDAs) and negotiable order of withdrawal (NOW) accounts. These are like checking accounts, but sometimes they might offer a little bit of interest. The key is that you can still access the money easily, usually with checks or a debit card.

So, when economists want to get a snapshot of the most readily available money in the economy, they'll look at the total of these components. It’s like gathering all the ingredients for a delicious cake before you start baking.

Why Is M1 So Special?

You might be thinking, "Okay, so it's the spendy money. Big deal." But think about it this way: if you have a million dollars tied up in a certificate of deposit (CD) that you can't touch for five years, that's money, sure, but it's not money you can use right now to buy groceries. M1, on the other hand, is the money that's actively flowing through our hands and our digital wallets.

It's the fuel for our everyday transactions. When M1 increases, it can signal that there's more money available for spending, which could lead to increased demand for goods and services. Conversely, a decrease in M1 might suggest less spending is happening. It's like observing the water level in a river – a higher level means more water is flowing, a lower level means less.

Economists and policymakers use M1 (and other money supply measures, like M2, which we won't dive into today!) to try and understand the pulse of the economy. Is it revving up? Is it slowing down? M1 is one of the gauges they check. It's not the only indicator, of course, but it's an important piece of the puzzle.

Let's Crunch Some (Hypothetical) Numbers!

Okay, so how would you actually compute the M1 money supply? It's actually quite straightforward with the right information. Imagine you're a super-sleuth collecting clues. You need to find the values for each component of M1.

Let's say, for instance, that the central bank (like the Federal Reserve in the US) releases the following figures:

Currency in circulation: $2.3 trillion

Demand Deposits: $15.1 trillion

Traveler's Checks: $1 billion (let's be generous and say it's still relevant!)

Other Checkable Deposits (OCDs): $2.8 trillion

To find the M1 money supply, all you have to do is add them all up!

So, our hypothetical M1 would be:

$2.3 trillion + $15.1 trillion + $0.001 trillion (that's $1 billion converted to trillions) + $2.8 trillion = $20.201 trillion

See? It's basically just adding a few big numbers together. The tricky part for economists isn't the math itself, but collecting and defining those numbers accurately and consistently. They have to be really careful about what they include and exclude.

It's like baking that cake. You need the right ingredients in the right amounts. If you accidentally add salt instead of sugar, your cake is going to be a disaster! Similarly, if economists misclassify a type of deposit, their M1 calculation will be off.

The Big Picture: Why It Matters

So, why do we go through all this trouble? Why do central banks track M1 so closely?

Well, it's all about managing the economy. If the economy is sluggish, a central bank might try to increase the money supply (including M1) to encourage more spending and investment. They can do this through various tools, like lowering interest rates. When interest rates are low, borrowing money becomes cheaper, which can spur businesses to expand and individuals to spend more.

On the flip side, if the economy is overheating and inflation is a concern (meaning prices are rising too quickly), a central bank might try to reduce the money supply or slow its growth. This can make borrowing more expensive and cool down spending.

M1 is like the canary in the coal mine for certain economic activities. It gives us a tangible measure of the money that's ready to be deployed. It’s the engine oil that keeps the economic machine running smoothly.

So, the next time you hear about the M1 money supply, don't let it scare you. Just remember it's the readily available cash and checking account balances that are out there, ready to be spent. It's a simple concept with some pretty profound implications for how our economy ticks. And understanding it, even a little bit, is a pretty cool way to feel a bit more in the loop about the world around you!