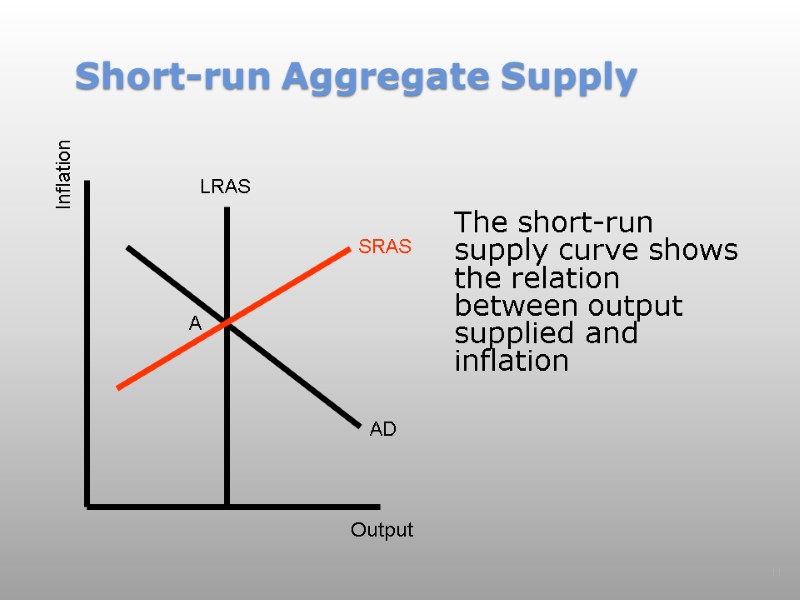

The Following Graph Shows Aggregate Demand And Short-run Aggregate Supply

Ever feel like the whole darn economy is just a giant, super-complicated party? Well, guess what? It kinda is! And just like any good bash, there’s always a push and pull between what everyone wants to buy and what everyone’s willing to sell. We're talking about <Aggregate Demand> and <Short-Run Aggregate Supply>, folks, and it’s not as scary as it sounds. Think of it like this: Aggregate Demand is basically all the people, businesses, and governments saying, "Yo, we're ready to party and we've got the cash to prove it!" Short-Run Aggregate Supply is the kitchen staff, frantically trying to whip up enough snacks and drinks to keep everyone happy, but only for a little while.

Let's break down <Aggregate Demand> first. Imagine you’re at that epic party, and suddenly, the DJ drops your absolute favorite song. What happens? Everyone gets jazzed! More people want to hit the dance floor, maybe grab another overpriced cocktail, or even splurge on that slightly-too-expensive party favor. That’s a surge in Aggregate Demand! It’s when the overall desire and ability to buy stuff across the entire economy goes up. It’s not just you wanting that extra slice of pizza; it's everyone, from your grandma buying a new knitting kit to the government deciding to build a new highway.

What makes this party demand go up or down? Loads of things! Think about your own wallet. If you suddenly get a bonus at work, you’re probably feeling a bit more generous, right? Maybe you'll finally buy those ridiculously comfortable slippers you’ve been eyeing, or treat yourself to a fancy dinner. That’s like <consumer spending> going up. When people feel good about their jobs and their money, they spend more. It’s the economic equivalent of suddenly deciding to wear your dancing shoes to the party.

Then there's <investment>. This is a bit like the party organizers deciding to invest in a better sound system or hire a magician. Businesses are basically doing the same thing. If they think people are going to keep buying their stuff, they’ll invest in new machines, expand their factories, or even hire more workers. This is them saying, "Hey, this party's gonna be a hit, let's make sure we can handle the crowd and maybe even make a bigger profit next time!" So, when businesses are feeling optimistic, investment goes up, and that boosts Aggregate Demand.

Don't forget the <government>! They’re like the ultimate party planner. They can decide to spend more on public services, infrastructure projects (hello, new roads!), or even give everyone a little stimulus check. When the government opens up its wallet, that’s <government spending> increasing, and guess what? More cash flowing around means more people and businesses are ready to buy. It's like the host suddenly deciding to foot the bill for everyone's drinks – suddenly, everyone’s feeling thirsty!

And finally, <net exports>. This one’s a little trickier, but stick with me. Imagine your party is so cool that people from other neighborhoods (other countries) want to come. They’ll be buying your local brews and goodies. That’s exports! But then, you might also be tempted to go to a party across town and buy their fancy snacks. That’s imports. <Net exports> are just the difference between what foreigners buy from you and what you buy from them. If foreigners are suddenly loving your party's signature punch (our country's goods), and you’re not really into their sad little cheese platters, your net exports go up, giving a little boost to Aggregate Demand.

So, Aggregate Demand is this big, sprawling beast that's made up of all these different appetites for buying. It's like the collective craving for fun, for new things, for that feeling of abundance. When it’s high, the party’s jumping!

Now, let’s talk about the poor souls in the kitchen: <Short-Run Aggregate Supply>. These are the businesses, the producers, the folks actually making all the stuff everyone wants to buy. In the short run, they’re like a really talented caterer who can whip up a ton of appetizers, but they can’t magically conjure up more ovens or hire an army of extra chefs overnight. They’re working with what they’ve got right now.

Think about a bakery. They’ve got their ovens, their flour, their sugar, and their bakers. If suddenly everyone wants croissants, they can probably bake more croissants, right? They might push their bakers to work a little harder, maybe leave the ovens on a bit longer. That’s increasing their <short-run output>. But they can’t just build a new wing onto the bakery in an afternoon. There are limits.

What influences how much stuff these kitchen folks can churn out in a hurry? Well, the biggest factor is <input prices>. Imagine if the price of flour suddenly went through the roof! The bakery would think, "Whoa, this is getting expensive. Maybe we can't afford to make as many croissants, or we'll have to charge a fortune!" So, if the cost of raw materials, wages, or energy goes up, it becomes more expensive for businesses to produce things. This means, at any given price level, they'll be willing to supply less. It’s like the caterer looking at the soaring price of shrimp and deciding to serve fewer shrimp cocktails. Sad, but true.

On the flip side, if the price of flour suddenly dropped (maybe a massive wheat harvest!), the bakery would be doing a happy dance! They could afford to make more croissants, maybe even offer a special deal. So, when input prices fall, businesses are more willing and able to produce more. It’s like finding out that fancy cheese is suddenly on sale – more cheese platters for everyone!

There’s also the idea of <technology and productivity>. If the bakery invests in a fancy new dough mixer that doubles its speed, or if the bakers find a more efficient way to proof the dough, they can produce more with the same amount of effort and resources. This is like the kitchen staff getting a secret shortcut or a super-powered gadget. It allows them to crank out more goods at a lower cost, increasing their Short-Run Aggregate Supply.

And finally, <expectations>. If the bakery expects that croissant demand is going to stay super high for a long time, they might be more willing to invest in that new oven we talked about. But in the short run, their expectations are more about things like future input prices. If they expect flour prices to skyrocket next month, they might try to produce as much as they can now while prices are stable, or they might hold back a bit if they think costs will be lower later. It's a bit like a chef deciding to make a big batch of soup now because they heard a rumor that vegetables are going to be super expensive next week.

So, Short-Run Aggregate Supply is all about the producers' ability and willingness to make stuff, given their current constraints and costs. They’re doing their best to keep up with the partygoers, but they can’t just pull rabbits out of hats.

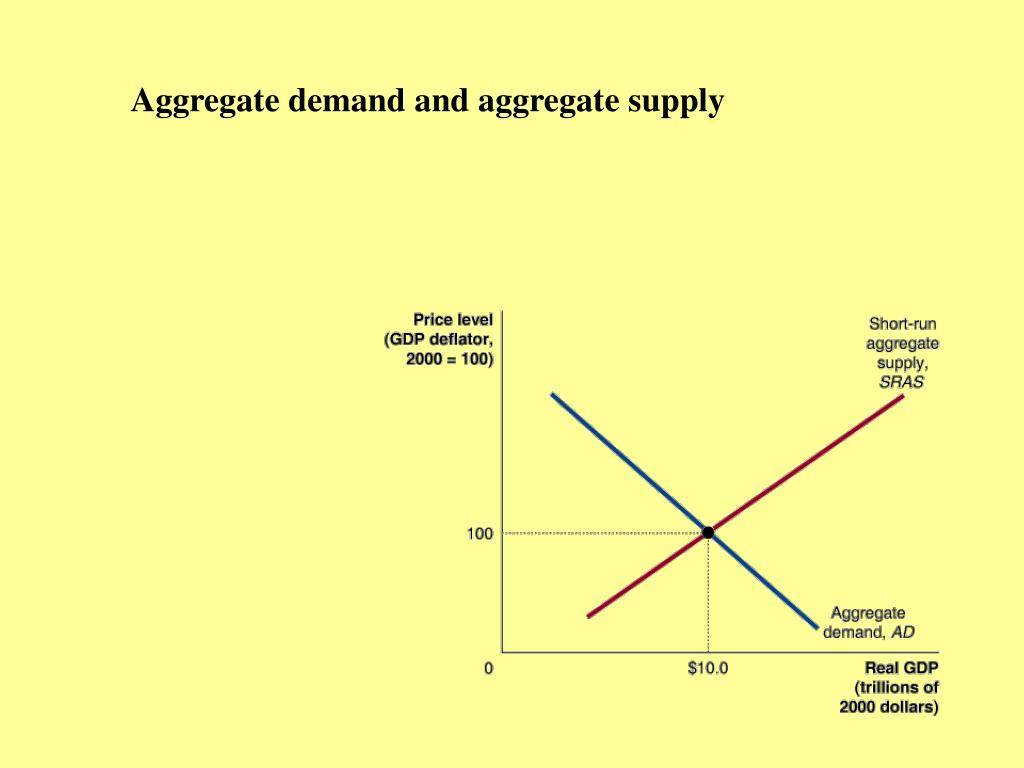

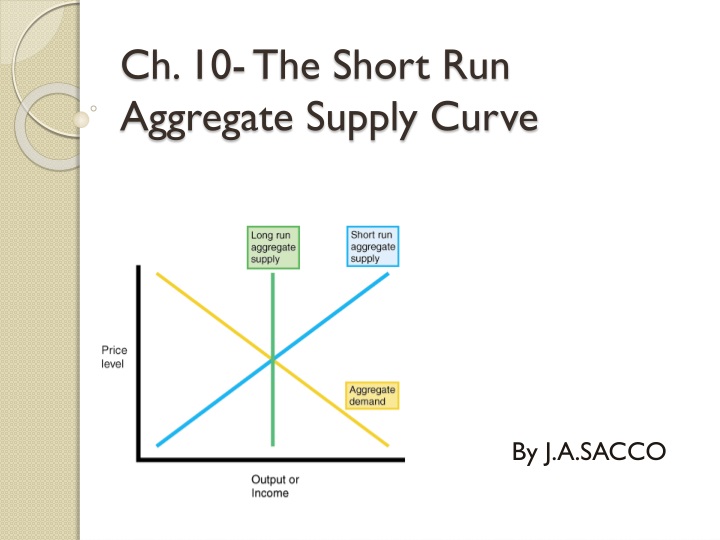

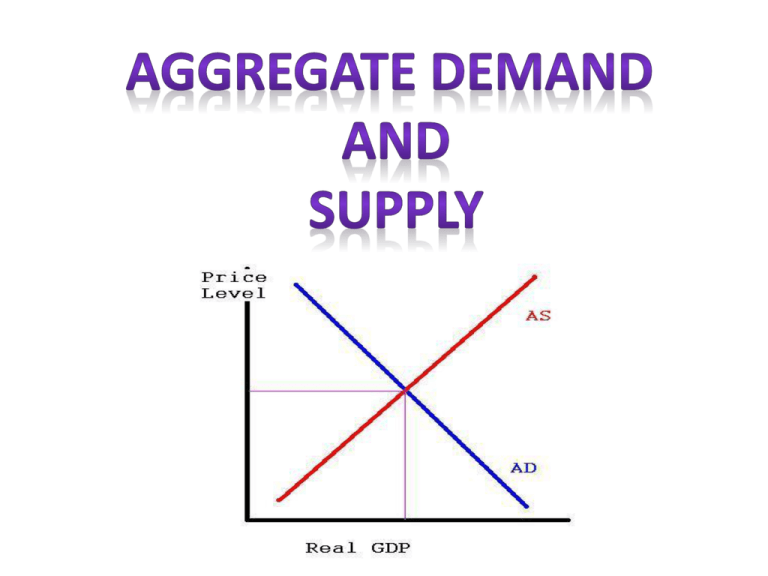

Now, the real magic happens when we put these two together on a graph. You’ve got your Aggregate Demand curve, which slopes downwards (because when prices are higher, people generally buy less, just like at a pricier bar). And you’ve got your Short-Run Aggregate Supply curve, which slopes upwards (because when prices are higher, businesses are more incentivized to produce more, given their current costs).

Where these two lines cross? That’s your <equilibrium>! It’s the sweet spot where the total amount of stuff people want to buy at a certain overall price level perfectly matches the total amount of stuff businesses are willing and able to sell at that same price level, in the short run. It’s like the moment at the party when there’s just enough food and drink for everyone, and everyone’s happy, and nobody’s having to fight over the last mini quiche. It’s the perfect balance!

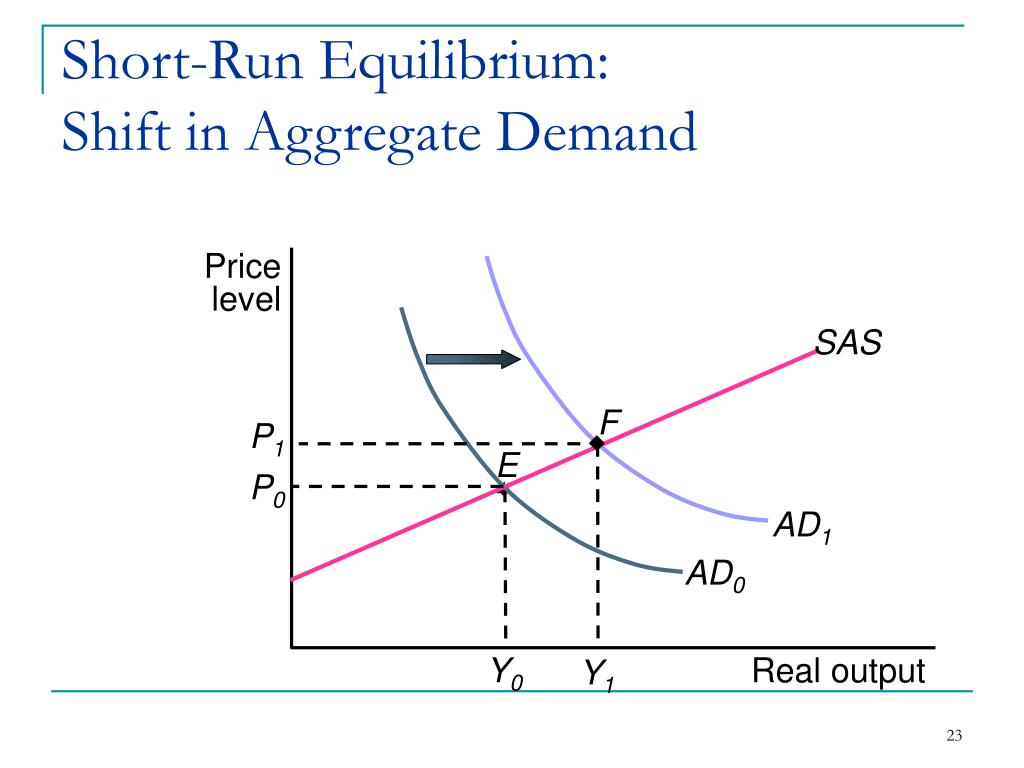

But here’s the fun part (and sometimes, the not-so-fun part): this equilibrium can change! Imagine if suddenly everyone at the party gets a massive influx of energy and wants to dance even more. That’s a <shift in Aggregate Demand> to the right. More people want to buy stuff at every price level. What happens? The intersection point moves! Businesses, seeing all this enthusiasm, might try to ramp up production. They’ll push those bakers and cooks harder. This means the <overall price level> tends to go up, and the <quantity of output> also goes up. It’s like the party getting so popular that you have to charge a bit more for entry, but at least everyone’s having a blast!

Conversely, if everyone suddenly decides to go home early (a <shift in Aggregate Demand> to the left), then businesses will find themselves with too much inventory and not enough buyers. The overall price level might fall, and the quantity of output will decrease. It’s like the party fizzling out, and the hosts are left with a ton of uneaten snacks.

Now, what if something happens in the kitchen? Let’s say the cost of electricity goes way up (a <shift in Short-Run Aggregate Supply> to the left). Now, it’s more expensive for businesses to produce anything. At every price level, they're willing to supply less. What happens to our equilibrium? Well, to get businesses to produce what they can, the overall price level has to go up even higher. But, because it's more expensive to produce, they’ll end up producing less output overall. This is the dreaded <stagflation> scenario: higher prices and less stuff being made. It's like the party getting really expensive, and the food portions getting smaller. Nobody likes that!

But, if there’s a technological breakthrough that makes everything cheaper to produce (a <shift in Short-Run Aggregate Supply> to the right), businesses are willing to supply more at every price level. This can lead to lower prices and more output. It’s like the caterer discovering a magic trick that lets them create delicious, abundant food at half the cost. Everyone wins!

So, this dance between Aggregate Demand and Short-Run Aggregate Supply is what shapes our economy on a day-to-day basis. It’s why prices go up sometimes, why jobs are plentiful at other times, and why we might have to wait a bit longer for that artisanal sourdough if there’s a global shortage of yeast.

It's not just abstract lines on a graph; it's the collective heartbeat of our economic party. It’s about our collective desire to buy and their collective effort to produce, all in this ever-shifting, sometimes chaotic, but always fascinating economic fiesta. And understanding this basic push and pull helps us make sense of why things are the way they are, from the price of our morning coffee to the big economic headlines we see every day. So next time you’re at a party, or even just at the grocery store, think about the dance of Aggregate Demand and Short-Run Aggregate Supply. You're living it!