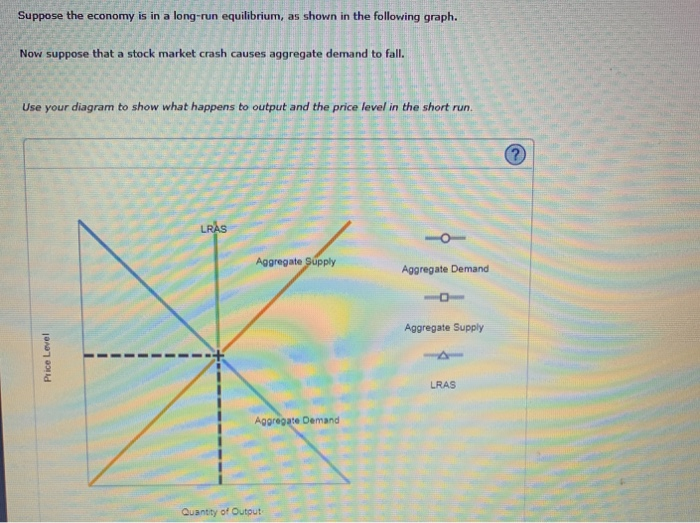

Suppose The Economy Is In A Long Run Equilibrium

So, imagine the economy is like a really chill, laid-back surfer, just kinda cruising on a wave. Not too fast, not too slow, just… vibing. That’s basically what economists mean when they say the economy is in "long-run equilibrium." It’s like everything’s in its happy place, and nobody’s freaking out. Think of it as the economic equivalent of finding that perfect spot on the couch where all your limbs feel right, and the remote is just within reach. Ah, bliss.

It's not about being wildly rich or anything. It's more about stability. Like when you’ve finally sorted out your Netflix queue and you’re not spending 20 minutes scrolling, agonizing over what to watch. You’ve hit that sweet spot where there’s always something good, but you’re not overwhelmed by choice. The economy in long-run equilibrium is like that. Businesses are chugging along at a steady pace, folks are generally employed (not necessarily with dream jobs, but jobs nonetheless), and prices are behaving themselves. No wild price spikes that make you question your life choices every time you buy milk, and no terrifying deflation where your money mysteriously gains value overnight (which, while sounding good, actually messes things up pretty badly – it’s like finding out your couch spot is too comfy and you’ll never want to move again, which isn't healthy!).

Think about your own life. When things are in equilibrium, you're not frantically chasing after a new job because you just got laid off. You're not trying to sell your prized collection of vintage Pogs because your rent doubled. You're probably just doing your thing, maybe saving a little, maybe splurging on that fancy coffee every now and then. It's that feeling of "yeah, this is fine."

And for businesses? It's like they’ve got their production line humming smoothly. They're not churning out way too much stuff that’s going to end up in a landfill, and they're not scrambling to make enough to meet a sudden surge in demand. They're just… making enough. It's the business equivalent of finally getting your sock drawer organized. Everything has its place, and it just works.

So, what does this magical "long-run equilibrium" actually look like under the hood? Well, for starters, the unemployment rate is at its natural rate. Now, this isn't zero unemployment, which would be about as likely as finding a unicorn riding a unicycle through your living room. The natural rate of unemployment is the level of joblessness that exists even when the economy is humming along nicely. Think of it as the people who are voluntarily between jobs, or who are learning new skills, or maybe just taking a well-deserved sabbatical to backpack through Europe. It’s the normal ebb and flow of the job market.

If you’ve ever been one of those people, you know it's not the end of the world. It might involve a bit of stress, sure, but you’re not staring into the abyss of permanent unemployment. You’re just in a phase. And in long-run equilibrium, that phase is a regular, expected part of life, not a crisis.

Another key player in this equilibrium fiesta is that production is happening at its potential. This means that all the factories, all the machines, all the talented people are being used to their full capacity, but without getting overheated. Imagine a baker who has just the right amount of dough, just the right oven temperature, and is making the perfect batch of cookies. They're not rushing and burning them, and they're not dawdling and letting them go stale. They're just making awesome cookies. That’s potential output.

When the economy is in equilibrium, it’s operating at this ideal level. It’s like your computer when it’s not running 50 browser tabs and your video editing software all at once. It’s responsive, it’s efficient, and it’s not making weird whirring noises that make you worry it's about to explode.

And then there are prices. In long-run equilibrium, inflation is stable and predictable. It’s not that crazy rollercoaster where your rent goes up 10% one month and then miraculously drops 5% the next. It's more like a gentle, predictable rise, the kind that makes you adjust your grocery budget slightly each year. Think of it as the slow, steady growth of your favorite houseplant. You notice it over time, but it doesn’t disrupt your life.

This stability in prices is super important because it allows businesses to plan. They can confidently decide how much to invest, how many workers to hire, and what prices to set for their products, because they have a pretty good idea of what the future holds. It's like knowing that if you save $10 a week, you'll have enough for that new video game in six months. No nasty surprises.

Now, you might be thinking, "Okay, this sounds pretty nice, but how does the economy get there?" Ah, that's the million-dollar question, isn't it? It's like asking how you got into that perfect couch spot. It's usually a combination of factors, and sometimes a bit of luck. In the real world, the economy isn't always perfectly in long-run equilibrium. It's more like a perpetual game of catch-up.

Think about what happens when the economy is not in equilibrium. Sometimes it’s like that time you accidentally downloaded a virus, and your computer started acting all weird and slow. That’s a recession. Or sometimes it’s like you’ve had way too much caffeine, and you’re bouncing off the walls, spending money like it’s going out of style. That’s inflation getting a bit out of hand.

When the economy is in a recession, unemployment goes up, businesses aren't producing much, and everyone's feeling a bit glum. It's like your favorite pizza place suddenly running out of dough and you have to eat… salad. The horror! In this situation, there are usually forces at play that try to nudge the economy back towards equilibrium. For example, if businesses are struggling, they might start lowering prices to attract customers. This can, over time, stimulate demand and get things moving again.

On the flip side, when the economy is booming too much, prices start to rise rapidly, and there's a risk of overheating. It's like trying to run your fancy new gaming PC with the case open in the desert. It’s going to get too hot, too fast. In this scenario, things like higher interest rates can come into play. The central bank might say, "Whoa there, buddy, let's cool it down a bit," making it more expensive to borrow money, which tends to slow down spending and investment.

These adjustments, the pushing and pulling of prices, wages, and interest rates, are what economists believe eventually guide the economy back to that long-run equilibrium. It's a bit like how, after a chaotic party, things gradually settle down. The music stops, the guests leave, and eventually, you’re left with a quiet house again. It might take a while, and there might be some mess to clean up, but order is restored.

So, why is this "long-run equilibrium" thing such a big deal? Well, for most people, it means a stable and predictable life. It means you can make plans for the future without worrying about your job disappearing overnight or your savings becoming worthless. It’s the economic equivalent of having a sturdy, reliable car. It might not be the fastest or the fanciest, but it gets you where you need to go, day in and day out.

For businesses, it means they can invest and grow with confidence. They can hire more people, develop new products, and contribute to the overall prosperity of society. It’s like having a well-stocked pantry; you know you’ve got what you need to cook up something delicious.

And for governments, a stable economy makes it easier to manage public finances. They can plan tax revenues and government spending more effectively. It's like having a clear budget for your household – you know where the money is coming from and where it needs to go. No more panicky calls to the bank because you forgot to factor in that unexpected car repair.

However, it’s important to remember that "long-run equilibrium" is a bit of an idealized concept. The real world is messy. There are always shocks and surprises. Think of the economy like a person trying to balance on a yoga ball. They can maintain equilibrium for a while, but a sudden sneeze or a gust of wind can knock them off.

Economies are constantly being hit by things like new technologies, natural disasters, or shifts in global demand. These events can push the economy out of equilibrium. For example, a sudden surge in oil prices can make it more expensive to produce and transport goods, leading to higher prices for almost everything. That's like the universe deciding your perfect couch spot is suddenly too sunny and you have to readjust.

When these shocks happen, the economy has to adjust. And as we discussed, these adjustments involve changes in prices, wages, and employment. These adjustments can be painful in the short term. People might lose jobs, businesses might struggle, and prices might fluctuate. It’s like going through a really intense workout session. You might be sore afterwards, but you’re ultimately getting stronger.

So, while the idea of a perfectly stable, long-run equilibrium is a nice theoretical goal, the reality is that economies are dynamic and ever-changing. The goal for policymakers is often to steer the economy towards that equilibrium as smoothly and as quickly as possible when it gets knocked off course. It’s like being a skilled driver who can navigate unexpected potholes and traffic jams without losing their cool.

In essence, when we talk about the economy being in long-run equilibrium, we’re talking about a state of relative stability. It’s not about being static, but about being balanced. It’s the economic equivalent of a perfectly brewed cup of coffee – not too bitter, not too weak, just right. It's a state where the fundamental forces of supply and demand are in harmony, allowing for sustainable growth and prosperity.

It's the economic version of when all the stars align, and your internet connection is fast, your favorite show is on, and you’ve managed to get that last slice of pizza. It’s not something that lasts forever, but when it’s happening, you definitely notice and appreciate it. And that, my friends, is the beauty of economic equilibrium – it’s the sweet spot where things just… work.