Should You Have Full Coverage On An Old Car

Ah, the old car. That trusty steed that’s seen you through thick and thin. It’s the one that remembers your first date, the one that carried your tiny human home from the hospital, the one that somehow always starts, even on the chilliest mornings. It’s less a machine and more a furry, four-wheeled member of the family, isn’t it? And like any beloved family member, you want to take care of them. But when it comes to “full coverage” insurance on your venerable vehicle, things can get a little… complicated. Think of it like this: would you buy your grandma the latest, souped-up, top-of-the-line sports car insurance? Probably not. But maybe you’d spring for a really good membership at the local bingo hall. It’s all about what makes sense for them (and their wallet!).

Let’s be honest, that old beauty might have a few more… character lines than it used to. Maybe the passenger side door has a slight “kiss” from a rogue shopping cart, or the paint has a charming patina that only comes with years of dedicated sunbathing. These aren’t just dings and scratches; they’re battle scars! They tell a story. And sometimes, the cost of fixing those stories can add up faster than you can say, "where did I park this thing?" This is where the whole “full coverage” debate for an old car really kicks in. It's like deciding whether to get your old teddy bear a full spa treatment or just a good stitch-up here and there.

The heart wants what the heart wants, and sometimes, the heart has a serious soft spot for a car that rattles a little more than it used to.

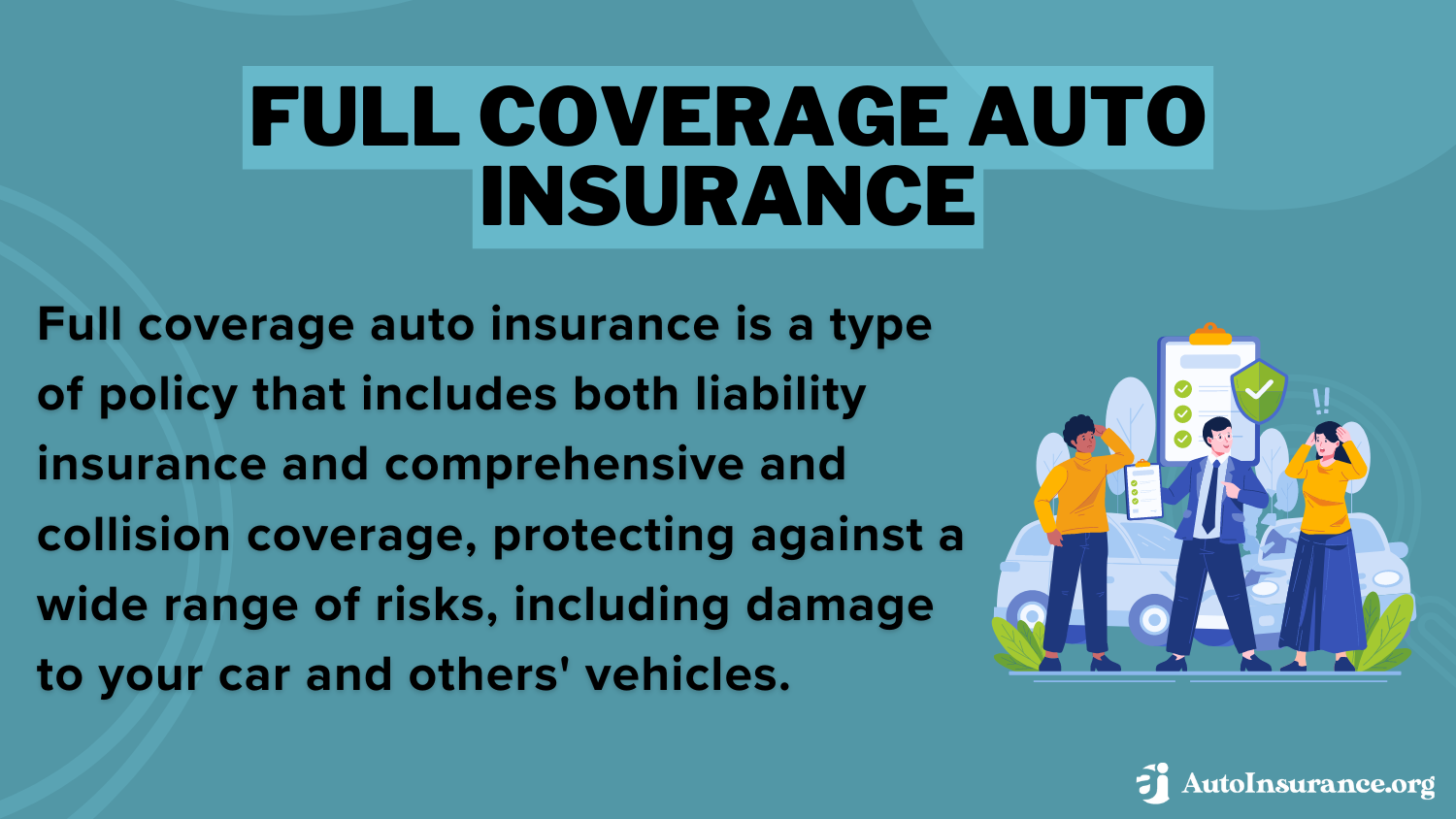

So, what exactly is this "full coverage" we keep hearing about? In simple terms, it’s usually a bundle. You’ve got your liability, which is the must-have. It’s like saying, "If I accidentally cause a flap, I’ve got the money to help fix it for others." Then there’s collision, which covers damage to your car if you bump into something. And comprehensive, which is your superhero for stuff like theft, vandalism, or that time a rogue flock of geese decided your windshield was a personal trampoline. For a brand new, shiny car, this feels like a no-brainer. It's like insuring your prized sourdough starter – you don’t want anything to go wrong!

But for ol’ reliable? The one whose engine sounds like a gentle jazz improvisation and whose upholstery has seen more snacks than a movie theater? This is where the numbers game gets interesting. Imagine you’ve got a car worth, let’s say, a few thousand dollars. Now, let’s think about the cost of full coverage. If you’re paying a hefty monthly premium for coverage that might exceed the car’s actual worth, you might start to question things. It's like buying a designer suit for your garden gnome. Adorable, but perhaps not the most practical investment. Your insurance company, bless their analytical hearts, is looking at the potential payout versus the premiums you're paying. If the car is worth less than what they’d potentially have to pay out in a major accident, they might look at you with their spreadsheets and say, "Hmm, maybe we can offer you a less… enthusiastic plan."

However, there’s a heartwarming twist to this tale. Sometimes, the sentimental value of that old car is immeasurable. It’s not just metal and rubber; it’s a vessel of memories. Think about the road trips, the singing at the top of your lungs with the windows down, the sheer relief of making it to your destination without a single hiccup. This is where insurance decisions can get emotional. You might decide that the peace of mind, knowing that if something truly catastrophic happens, you’ve got a safety net, is worth more than the depreciated dollar value of the car itself. It’s like insuring your childhood diary. The monetary value might be zero, but the thought of losing it? Priceless.

There’s also the practical side. Does this old car get you to work reliably? Is it your only mode of transportation? If you were to lose it, would replacing it with something else, even a newer used car, be a huge financial strain? If the answer is yes, then keeping a bit of extra protection, even on an older vehicle, starts to make a lot of sense. It’s like having a really good umbrella. You might not use it every day, but when the sky opens up, you’re incredibly grateful you have it. Perhaps the “full coverage” you need isn’t necessarily the most expensive, cutting-edge package, but rather a smart, tailored approach. Think of it as a comfortable cardigan, not a haute couture gown.

Ultimately, the decision is a dance between practicality and passion. You’re looking at the numbers, sure, but you’re also listening to your heart, the one that hums a little louder when you slide into that familiar driver's seat. Maybe the answer isn't a strict "yes" or "no" to full coverage, but a thoughtful "what kind of coverage best suits my beloved, aging companion and my peace of mind?" It’s about finding that sweet spot where you feel protected, your memories are respected, and your old car can keep chugging along, carrying you to your next adventure, whatever it may be.