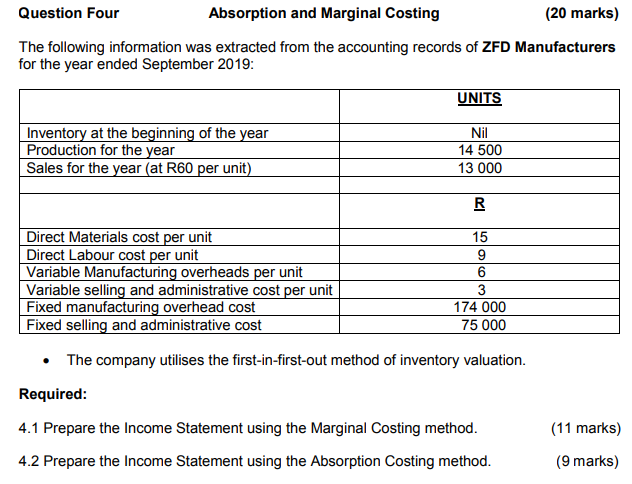

Marginal And Absorption Costing Questions And Answers Pdf

So, there I was, staring at a pile of these tiny, handmade ceramic coasters. Each one was unique, a little artistic endeavor from my friend Sarah. She was beaming, showing them off. “Look!” she chirped, “I’ve priced them at $10 each.” I, being the accountant friend (cue the dramatic organ music), immediately felt a tiny twitch in my eyebrow. My brain, in its usual, slightly annoying way, started doing calculations.

I pictured the clay, the glaze, the hours she spent meticulously painting each one. I thought about the kiln, the electricity, even the little bubble wrap she'd use for shipping. And then I thought, “Okay, $10 sounds nice, but is it enough?” This, my friends, is where the wonderful, sometimes mind-bending world of costing sneaks into our lives, even if we’re just trying to support a friend’s adorable coaster business. And specifically, it’s where marginal and absorption costing come into play. Ever heard of them? No? Well, strap in, because we’re about to dive in, and yes, there will be questions and answers, and maybe a PDF involved!

Now, Sarah’s coasters are a cute example, but this stuff is huge for businesses. Like, really, really huge. It affects pricing, profitability, and whether you’re celebrating success or quietly weeping into your spreadsheets. So, if you've ever found yourself staring at financial reports and feeling like you're deciphering ancient hieroglyphs, you're not alone. I've been there. We've all been there. And the good news? It doesn't have to be that scary. Especially when you find some handy-dandy Marginal and Absorption Costing Questions and Answers PDF resources. You know, the kind that feel like a friendly hand guiding you through the jungle.

The Great Costing Debate: Why Should You Care?

Let’s break it down, real simple. Imagine you’re making those coasters. You’ve got costs, right? Some costs are directly tied to making a coaster. That’s your variable cost. Think the clay, the glaze, the electricity for the kiln while it’s running for that specific batch. If you make one less coaster, you save on those specific materials. Pretty straightforward.

Then you’ve got costs that are there no matter what. These are your fixed costs. Sarah’s might be the rent for her little studio space, her internet bill, maybe the depreciation on her fancy kiln. Whether she makes 1 coaster or 1000 coasters, those costs are still there, ticking away. They don't change based on how many coasters you churn out in a month. This is a crucial distinction, and it’s the heart of the marginal vs. absorption costing difference.

So, why should you care about this nerdy costing stuff? Because it helps you understand your business’s true profitability. It helps you make smarter decisions. Do you raise your prices? Do you cut down on some costs? Do you run a sale to boost volume? Without understanding your costs, you’re basically flying blindfolded. And nobody wants that, trust me. It’s like trying to navigate a maze with your eyes closed. Frustrating, and you’re likely to bump into a whole lot of walls.

Enter Marginal Costing: The Lean, Mean, Decision-Making Machine

Okay, let’s talk marginal costing. This is the one that focuses purely on those variable costs. Think of it as saying, “What’s the absolute minimum it costs me to make one more coaster?” It looks at the cost of the materials, the direct labor involved in that one extra coaster, and any other costs that change with production volume.

Here’s the cool part: marginal costing is brilliant for short-term decision making. If Sarah gets an order for 50 extra coasters, marginal costing helps her figure out the incremental cost of fulfilling that order. It helps her decide if the price she’s charging covers those extra variable costs and contributes to her fixed costs and profit. It’s all about the contribution margin – the revenue left after deducting variable costs, which then contributes towards covering fixed costs and generating profit. It’s a very practical, no-nonsense approach.

Think of it like this: if you’re trying to decide whether to take on a special project that involves making a few extra items, you don’t need to worry about allocating your rent for those specific items. You just need to know if the revenue from those items covers the extra materials and labor. Makes sense, right? It’s about the margin each additional unit adds.

A common question here is: "How does marginal costing help in pricing decisions?" The answer is pretty direct: it provides the floor price. If the selling price is less than the marginal cost, you’re losing money on every single unit you sell, which is a big red flag. If it’s higher, you’re at least covering your direct costs and contributing to your overhead. Easy peasy, mostly. Though, the "mostly" part is where the complexities can creep in, which is why those Q&A PDFs are lifesavers. They’ll tackle those edge cases.

And Then There's Absorption Costing: The Full Picture (Sort Of)

Now, absorption costing (sometimes called full costing) is a bit more… well, absorbent. It takes all your manufacturing costs, both variable and fixed, and allocates them to your products. So, for Sarah’s coasters, absorption costing would say, “Okay, we have the clay (variable), the glaze (variable), the electricity (variable), AND the rent for the studio (fixed), the kiln depreciation (fixed). Let’s spread all of that out across the coasters we make.”

The idea is that all manufacturing costs should be absorbed by the products that incurred them. This is the method typically required for external financial reporting (like your company’s annual report) and for tax purposes. Why? Because it’s seen as a more conservative way to value inventory. It includes a portion of fixed manufacturing overhead in the cost of each unit. So, your inventory on the balance sheet reflects not just the direct materials and labor, but also a slice of those fixed factory costs. This can make inventory look more valuable.

But here’s where things get a little… ironic. While it’s great for external reporting, absorption costing can sometimes be a bit tricky for internal decision-making. Because fixed costs are being allocated to each unit, the reported profit can fluctuate depending on how many units you produce and sell. If you produce a lot but sell only a little, some of those fixed costs get stuck in your inventory, making your reported profit for the period look higher. Conversely, if you sell a lot but produce less, you might release more fixed costs from inventory, potentially making your reported profit look lower. It’s a bit of a mathematical dance that can sometimes obscure the true underlying profitability of each sale.

A classic question you'll find in Q&As is: "When would a company choose to use absorption costing over marginal costing for internal reporting?" Honestly, most wouldn't choose it for internal decision making. It's mandated for external reporting. However, some managers might still get comfortable with it, perhaps due to habit or a belief that it provides a more 'complete' cost picture. But for true operational decisions, marginal costing often shines brighter. The key is knowing when to use which tool. It’s like having a screwdriver and a hammer; you wouldn’t use a hammer to screw in a nail, right?

The Nitty-Gritty: Questions and Answers You'll Actually Encounter

Okay, let’s get down to brass tacks. You’re probably wondering what kind of questions you’ll actually see, and how the answers are usually structured. This is where those trusty PDFs come in. They’re usually filled with practical scenarios that mirror real-life business situations, just simplified for learning.

Here are some common themes:

Scenario 1: The Special Order Dilemma

Imagine a company that makes custom phone cases. They receive an offer from a large retailer to buy 5,000 cases at a price significantly lower than their usual selling price. The company has spare production capacity.

The Question: Should the company accept this special order?

The Answer (Hinting at Marginal Costing): You’d analyze the incremental costs of producing these 5,000 cases. These would be the variable costs per case (direct materials, direct labor, variable manufacturing overhead). You’d then compare this total incremental cost to the revenue generated by the special order. If the revenue exceeds the incremental costs, and there's no negative impact on regular sales, it's usually a good idea to accept. Fixed costs don’t usually factor into the decision for special orders if you have spare capacity, because those fixed costs will be incurred anyway.

This is a prime example of where marginal costing is your best friend. You're just asking, "Does this extra business cover the extra costs?"

Scenario 2: Inventory Valuation Woes

A manufacturing company produces widgets. In a period of low sales, they produce significantly more widgets than they sell.

The Question: How will this affect reported profit under absorption costing versus marginal costing?

The Answer (Highlighting the Difference): Under absorption costing, the fixed manufacturing overhead is allocated to each widget produced. Since more widgets were produced, more fixed overhead will be "absorbed" into the cost of those widgets and sit in inventory on the balance sheet. This means less fixed overhead is expensed on the income statement, leading to a higher reported profit for the period, even though sales haven't increased.

Under marginal costing, fixed manufacturing overhead is treated as a period cost and is expensed in the period it’s incurred, regardless of production volume. Therefore, the profit reported under marginal costing would be lower in this scenario, reflecting the actual costs incurred during the period. This is the key difference that can cause confusion! It's not that one is 'wrong' and the other is 'right', they're just answering slightly different questions.

See? This is why you’ll find tons of questions like this in Q&As. They want to make sure you grasp the impact of inventory changes on profit under each method.

Scenario 3: Make or Buy Decisions

A furniture company is deciding whether to continue manufacturing a specific component for their chairs or to outsource its production to an external supplier.

The Question: What costing approach is most useful for this decision?

The Answer (Focusing on Relevant Costs): For a make-or-buy decision, you need to look at the relevant costs. This often leans heavily on marginal costing principles. You compare the incremental costs of making the component in-house (direct materials, direct labor, variable overhead, and any additional fixed costs incurred only if you make it) with the price quoted by the external supplier. You also need to consider any opportunity costs (e.g., if the factory space used for making the component could be used for something more profitable).

Opportunity costs are a whole other can of worms, but they often come up in these decision-making contexts. Don't forget them!

Where to Find Your Magical PDF

So, you’re probably thinking, “Okay, this is fascinating, but where do I get my hands on these magical Marginal and Absorption Costing Questions and Answers PDF documents?” Good question! There are a few avenues:

- University/College Websites: Many business schools and accounting departments make past exam papers, study guides, and sample questions available online. Search for “[University Name] accounting department marginal absorption costing questions pdf” or similar.

- Online Learning Platforms: Sites like Coursera, edX, Udemy, and even YouTube often have free or paid courses on management accounting that include downloadable resources.

- Accounting Forums and Blogs: Sometimes, dedicated accounting communities or bloggers will share useful PDFs or links to them. A quick Google search for "accounting study resources marginal absorption costing" can yield results.

- Textbook Companion Websites: If you’re using a specific management accounting textbook, check if it has a companion website. These often provide supplementary materials, including practice questions.

Just remember to be a little discerning. Ensure the PDFs are from reputable sources. While a random blog post might have some good insights, official study materials or university resources are usually more reliable for structured learning.

Final Thoughts: It’s All About the Perspective

Ultimately, the difference between marginal and absorption costing boils down to perspective. Marginal costing is your go-to for short-term, operational decisions. It asks, "What’s the direct impact of this action on our cash flow and profitability right now?" Absorption costing is for the bigger, external picture. It’s about valuing inventory accurately for financial statements and reporting a cost that reflects the total manufacturing effort.

Neither is inherently "better" than the other; they serve different purposes. Understanding both, and crucially, knowing when to apply each one, is what makes you a savvy business person (or at least, a very helpful friend to your ceramic coaster-making buddies). So, next time you’re faced with a pricing decision or a production query, don’t just guess. Think about your costs. Think about your margins. And maybe, just maybe, you’ll find that PDF that clarifies everything for you. Happy costing!