Is A Car Loan A Secured Loan? Here’s What’s True

Hey there, car dreamers and finance fans! Ever stared at a shiny new set of wheels, or maybe a trusty pre-loved chariot, and wondered about the magic behind making it yours? We're talking about car loans, of course! They’re like the secret handshake of the automotive world, letting you drive off the lot without emptying your piggy bank. But here's a juicy question that tickles the curiosity of many: Is a car loan a secured loan? Buckle up, because we’re about to spill the beans in a way that’s anything but boring!

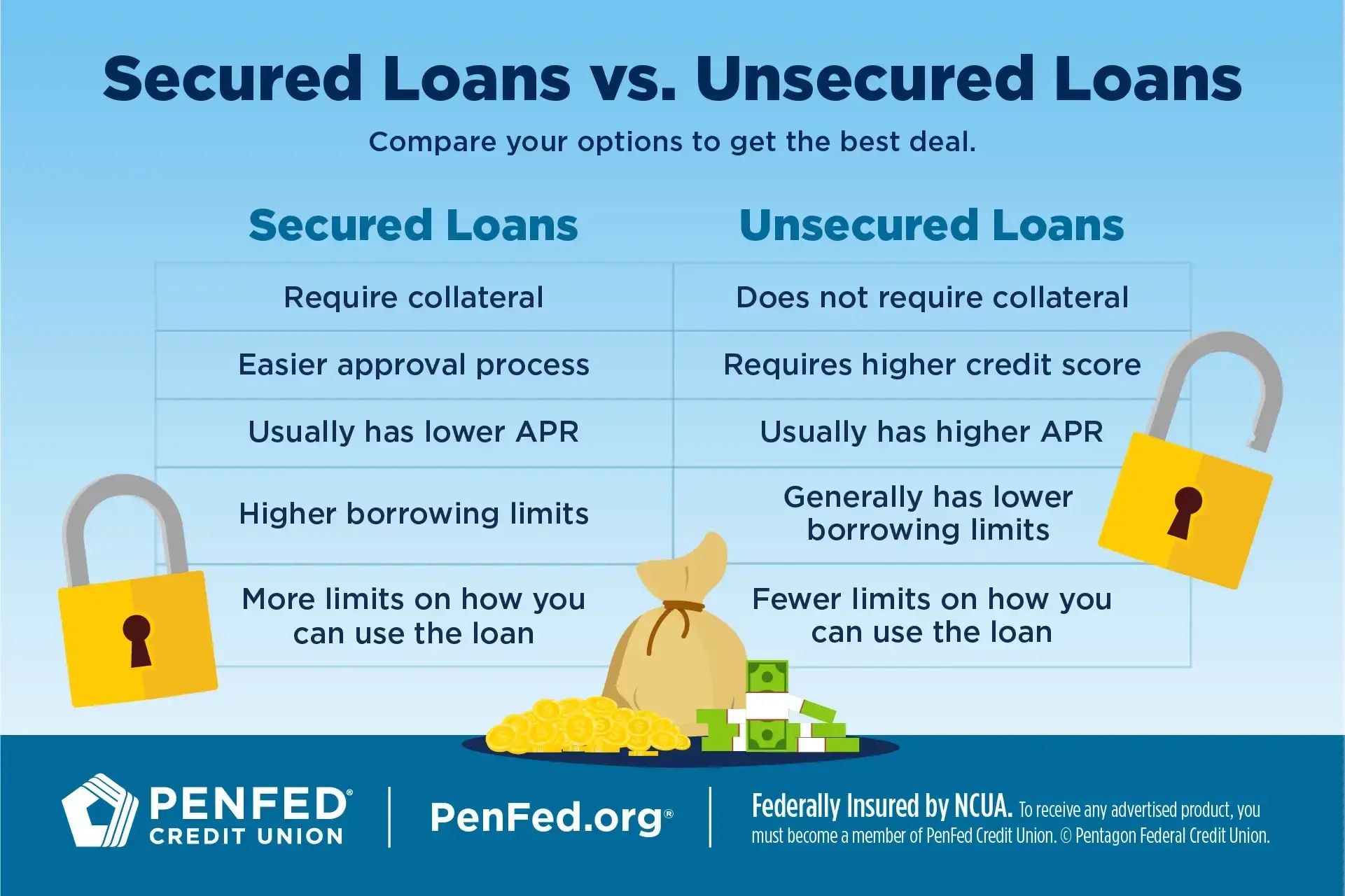

Think of it this way: when you borrow money, especially for something as significant as a car, lenders like to have a little safety net. Imagine lending your favorite (and very expensive) gaming console to a friend. You’d probably want them to promise to give it back, right? Or maybe even have them leave their super cool bike with you as a "just in case." That's kind of what a secured loan is all about. It’s a loan that’s backed up by something valuable, something the lender can hold onto if, you know, things go a little sideways.

So, what's the big secret with car loans? Drumroll, please... Yes, a car loan is almost always a secured loan! Pretty neat, huh? What makes it "secured" is the very car you’re buying. That’s right, your awesome new ride is the collateral. This is the part that makes lenders feel all warm and fuzzy inside. They’re essentially saying, "Okay, we’ll lend you the cash, and if for some reason you can’t pay us back, we can take the car. It's like a high-stakes game of automotive tag!"

This is actually super important for you, too. Because the loan is secured, lenders can often offer you better interest rates. It’s like getting a discount because you’ve shown them you’re serious. Think of it as a reward for putting your valuable possession on the line. If you were to get an unsecured loan (which are rare for car purchases, by the way), the interest rates would likely be sky-high, making your car payments feel like a dragon's fiery breath on your wallet.

Let's get a little more into the nitty-gritty, but in a fun way. When you sign that car loan agreement, you're essentially giving the lender a lien on the vehicle. A lien is like a legal claim. It means they have a right to the car until you’ve paid off the entire loan amount, plus all the interest. You get to drive the car, enjoy all its fantastic features (does it have heated seats? Ooh la la!), but the lender has that little reminder hanging over it, like a very polite but firm handshake.

Once you’ve made your very last payment – hooray! – that lien gets released. Poof! Gone! The car is officially and completely yours. No more strings attached. It’s a moment of pure automotive freedom. You can sell it, trade it in, or just drive it into the sunset with the peace of mind that it's 100% yours.

So, why is this even a fun topic to chat about? Because understanding this stuff makes you a smarter car buyer! It’s like having a secret superpower at the dealership. When you know that your car is the collateral, you understand why lenders are willing to offer you that loan. You also understand the responsibility that comes with it. It's not just about the cool Bluetooth system; it’s about a financial commitment!

It’s also what makes car loans so accessible for so many people. Imagine if you had to pay for a car entirely upfront. For most of us, that would be a serious challenge. Car loans, being secured, allow lenders to take on a bit more risk, which in turn helps them offer funds to a wider range of buyers. They’re the unsung heroes of making car ownership a reality for millions!

Think about it: if you were buying a house, that's also a secured loan – the house itself is the collateral. The principle is the same, just a much bigger scale and often a much longer payment plan. Cars are just a more accessible, everyday version of this financial magic.

Now, what happens if you miss payments? This is where the "secured" part really hits home. If you fall behind on your car payments, the lender has the right to repossess your vehicle. Repossession is the fancy word for them taking the car back. It's not a pleasant experience, and it can seriously damage your credit score, making future borrowing much tougher. This is why it’s so crucial to be confident you can manage the monthly payments before you sign on the dotted line.

But let’s not dwell on the "what ifs" too much! The vast majority of people get car loans and sail through their repayment period with flying colors. The secured nature of the loan is what makes it work, and it’s a brilliant system that benefits both the borrower and the lender. It’s a partnership, really, all centered around your sweet ride.

So, to wrap it up with a bow on top: A car loan is indeed a secured loan. Your car is the collateral. This is what allows lenders to offer you better terms and makes the whole process work smoothly for millions of happy drivers out there. It’s not just a loan; it's your ticket to freedom, paved with a little financial responsibility and a whole lot of awesome driving!

Isn’t that fascinating? The next time you see a car loan offer, you’ll know the clever mechanism behind it. It's like understanding how your favorite toy works – it just makes it more amazing! So go ahead, dream big, and when you’re ready to make that dream a reality, you’ll have this little piece of financial wisdom in your pocket. Happy car hunting!