How To File A Fraud Alert With Credit Bureaus

/images/2023/07/12/fraud-alert_06.png)

Hey there! So, you’ve had a little scare, huh? Maybe a weird credit card charge popped up that wasn't yours, or you got a creepy email saying your identity might be in jeopardy. Whatever it is, it’s totally normal to feel a bit freaked out. But guess what? You're not helpless! We can totally tackle this thing together. Think of me as your friendly guide through the sometimes-confusing world of credit bureaus. We're gonna break down how to slap a fraud alert on your credit report, which is basically like putting a big, neon sign up saying, "Hey, this person might be a target, so double-check everything before you approve a new loan in their name!" Pretty neat, right?

First things first, let's get our heads straight. A fraud alert isn't going to magically fix any damage that's already been done. It's a proactive step to prevent future shenanigans. So, if you’ve already spotted some unauthorized activity, you'll need to report that separately to the company involved and potentially the police. But for stopping new accounts from being opened in your name without your knowing wink, a fraud alert is your new best friend. And the best part? It's absolutely free! Yep, you read that right. No hidden fees, no sneaky subscriptions. Just pure, unadulterated protection. So, ditch the stress wrinkles for a sec, and let’s get this done.

The Big Three: Who Are These Credit Bureaus Anyway?

Before we dive into the "how-to," we gotta know who we're talking to. In the good ol' United States, there are three main credit bureaus that pretty much run the show: Equifax, Experian, and TransUnion. They're like the ultimate scorekeepers of your financial life, collecting all sorts of information about how you handle money. This includes things like how often you pay bills on time, how much debt you have, and whether you've ever, you know, defaulted on that loan for a solid gold toilet.

When you apply for a loan, a credit card, or even sometimes an apartment, these companies are the ones that lenders go to for a peek at your creditworthiness. They compile all this data into your credit report. So, if someone is trying to open a new account in your name, they’re likely going to hit up one (or all!) of these bureaus to get the ball rolling. That’s why our mission is to get that fraud alert in front of all of them.

Why Bother With a Fraud Alert? The “Just In Case” Brigade

Okay, let’s be honest. Most of us aren't expecting to wake up tomorrow and find out our identity has been hijacked. But sadly, identity theft is a real thing. It's like that creepy clown who lives down the street – you might not see him every day, but he’s out there. A fraud alert is basically your personal bodyguard for your credit. It's a temporary measure, typically lasting for one year, that tells lenders to take extra steps before approving any new credit in your name.

What kind of "extra steps," you ask? Well, they’re supposed to verify your identity. This usually means they’ll try to contact you directly – by phone or mail – to confirm you’re the one actually signing up for that new, suspiciously large, diamond-encrusted unicorn saddle. If they can't reach you or verify your identity, they’re supposed to say, "Nope, not today, shady character!"

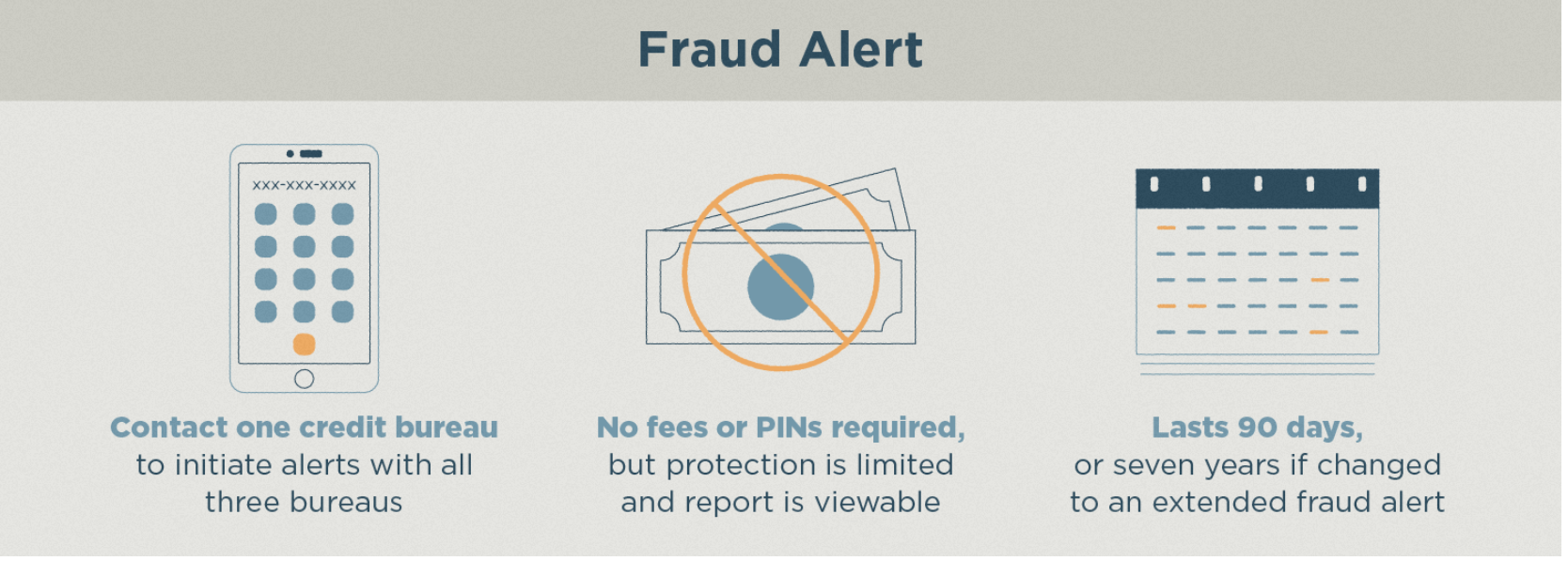

There are a couple of types of fraud alerts, and it's good to know the difference. We’ve got the initial fraud alert, which is what we're focusing on today. This one is for when you suspect you might be a victim of identity theft. Then there’s the extended fraud alert. This one is a bit more serious and lasts for seven years. You usually get this if you’ve actually been a victim of identity theft and can provide some sort of documentation, like a police report. For now, let's stick with the initial one – it's the easiest to get and a great starting point.

/images/2023/07/12/fraud-alert_02.png)

How to Actually Do It: The Step-by-Step, No-Sweat Guide

Alright, deep breaths! This is the fun part – the actual doing. And here’s the kicker: you only need to contact one of the three credit bureaus to initiate a fraud alert. Why just one? Because, by law, when you place a fraud alert with one of them, they are required to notify the other two. It's like the ultimate credit bureau gossip network, but for your own good!

So, choose your champion! You can pick Equifax, Experian, or TransUnion. Whichever one you feel most connected to (or just the one whose website loads fastest), that’s the one you’ll call or visit online.

Option 1: The Online Adventure (My Personal Favorite!)

Let's be real, who has time for endless hold music these days? Most of us prefer the digital route. And thankfully, all three credit bureaus have made it pretty straightforward to place a fraud alert online. Here’s the general gist:

- Head to their websites:

- Look for the "Fraud Alert" or "Identity Theft Protection" section. This might be under a "Security," "Help," or "Personal Services" tab. It’s usually pretty easy to spot once you’re on the right page.

- Follow the prompts to submit your request. You’ll likely need to provide some basic personal information to verify your identity. This might include your name, address, date of birth, and Social Security number. Don’t worry, this is standard procedure for security purposes.

- Confirm your request. They'll probably send you an email or a confirmation number. Keep this handy! It's your proof that you’ve taken this important step.

It’s usually a pretty quick and painless process. Think of it like ordering your favorite takeout online – click, click, done! And remember, once you do it with one, the others will get the memo. It's like sending a group text, but way more important.

Option 2: The Phone Call Crusade (For the Traditionalists)

If you’re more of a "talk to a human" kind of person, or if you're having trouble with the online forms (hey, technology isn't always our friend!), you can always give them a ring. Here are the general numbers, but it’s always a good idea to double-check their websites for the most current contact information:

- Equifax: 1-800-525-6285

- Experian: 1-888-397-3742

- TransUnion: 1-800-680-7289

When you call, you'll likely speak with an automated system first, but you should be able to navigate to the fraud alert department. Be prepared to provide the same personal information you would online. The representative will guide you through the process. It might take a little longer than the online method, but you'll get that personal touch.

Option 3: The Mail-In Mission (For the Patient Philosophers)

This is the slowest method, and honestly, not recommended unless you really prefer snail mail or have specific circumstances. But for completeness, here’s how it generally works:

- You’ll need to download a fraud alert request form from the credit bureau’s website.

- Fill it out completely with all your personal details.

- Mail it to the address provided on the form.

Again, this can take a while for them to process, and in the meantime, your information is still out there. So, if you’re going to mail it, be extra vigilant until you get confirmation that the alert is in place.

What Happens Next? Your New Credit Reality

Okay, you’ve done it! You’ve placed your fraud alert. High five! So, what does this actually mean for your day-to-day life? Here’s the lowdown:

- You'll likely receive a confirmation letter or email from the credit bureau(s) stating that your fraud alert has been placed. Hold onto this like it's a winning lottery ticket!

- When you apply for new credit, lenders will be required to verify your identity. This might involve a phone call or an email from them. Don't be surprised if this happens – it's exactly what you wanted!

- You're entitled to a free credit report from each of the three bureaus if you've been notified of a suspected identity theft incident. Even without that notification, you can still get free credit reports annually from each bureau at www.annualcreditreport.com. This is your chance to give your reports a good old once-over and make sure everything looks legit.

It's important to remember that a fraud alert is not a credit freeze. A credit freeze is a more restrictive measure that completely blocks access to your credit report, making it impossible for anyone (including you, sometimes!) to open new accounts. A fraud alert simply adds a layer of verification. You can still get credit with a fraud alert in place, it just takes a bit longer.

Bonus Tip: The Free Credit Report Rodeo!

Seriously, go get your free credit reports! It’s the best way to be in the know about what’s happening with your financial self. You can get one free credit report every 12 months from each of the three bureaus by visiting www.annualcreditreport.com. This is the official, government-mandated way to get your reports, so no funny business.

Once you have them, don't just glance at them and toss them aside. Pour yourself a cup of your favorite beverage, put on some chill music, and actually read them. Look for any accounts you don't recognize, any addresses that aren't yours, or any inquiries you didn't authorize. If you spot anything fishy, that’s your cue to take further action, which might involve filing a dispute with the credit bureau directly.

/images/2023/07/12/fraud-alert_15.png)

Don't Forget About Other Important Stuff!

While we're on the topic of protection, here are a few more things to keep in mind:

- Review your bank and credit card statements regularly. This is your first line of defense! If you see something off, report it immediately to the financial institution.

- Be cautious about sharing personal information. Don't give out your Social Security number, bank account details, or other sensitive information unless you are absolutely sure you know who you're dealing with and why they need it.

- Shred sensitive documents before tossing them in the trash. Think old bills, pre-approved credit offers, and anything with your name and address on it.

- Use strong, unique passwords for your online accounts and enable two-factor authentication whenever possible.

Think of all these steps as building a fortress around your financial well-being. The more layers of protection you have, the harder it is for any unwanted guests to get in.

You've Got This!

Phew! We made it. See? Placing a fraud alert is totally doable. It’s a smart, proactive step that gives you a bit of peace of mind in a world that can sometimes feel a little uncertain. You’ve taken control, you've armed yourself with information, and you’re looking out for yourself. That's pretty darn impressive, if you ask me!

Remember, you're not alone in this. Millions of people take steps to protect their identity every year. By understanding how these systems work and taking simple actions like placing a fraud alert and regularly checking your credit reports, you’re becoming a financial superhero. So, go forth, be vigilant, and know that you've got the power to keep your financial future bright and secure. Give yourself a pat on the back – you’ve earned it!