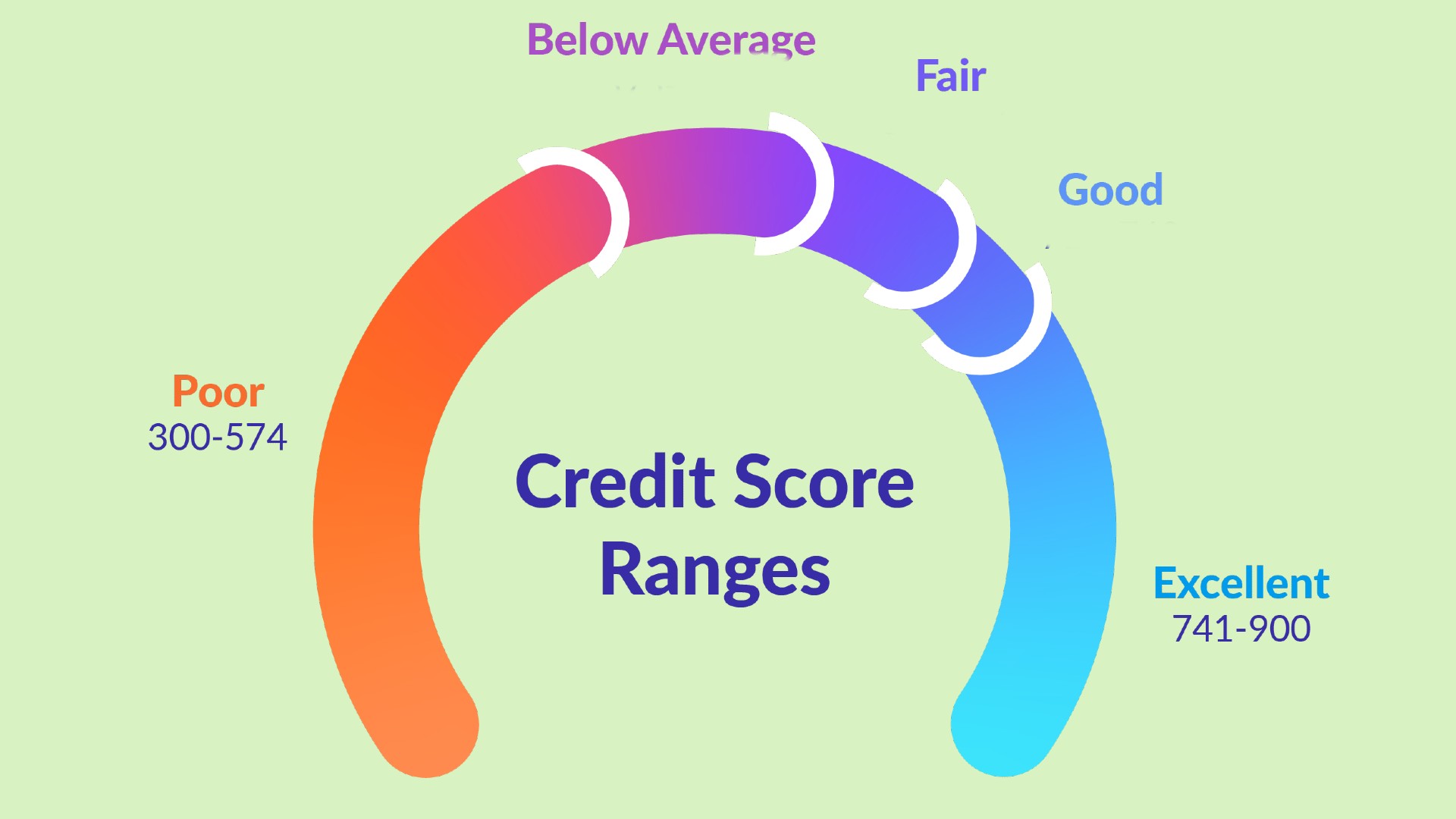

How To Check Why Your Credit Score Went Down

So, you peeked. You bravely navigated the labyrinthine digital pathways to find out your credit score, and… oops. It’s not quite the dazzling number you were hoping for. Maybe it’s dipped a little, like a shy turtle retracting its head. Don’t panic! Think of this not as a personal failing, but as a fun little mystery to unravel. After all, understanding your credit score is like learning the secret handshake to a club that can get you awesome stuff like new apartments, cool cars, and even that dream vacation. And who doesn’t love a good secret?

Let’s be honest, the world of credit scores can sound a bit intimidating. Like trying to assemble IKEA furniture without the instructions. But trust me, it’s way less frustrating (and you won’t end up with a wobbly bookshelf). This is your chance to become a credit score detective, armed with curiosity and a can-do attitude!

The Great Credit Score Mystery: Where Did It Go?

Alright, Detective! Your first mission, should you choose to accept it (and you totally should!), is to figure out why your score decided to take a little siesta. The good news? It’s usually not some shadowy figure working against you. More often than not, it’s a few simple things you might have overlooked. Think of it as your financial report card, and it’s just giving you a friendly nudge.

So, where do you even begin? The most important step is to get your hands on your credit report. This is the detailed record of your credit activity. It’s like the whole backstory for your credit score. You can get free copies of your credit report from each of the three major credit bureaus – Equifax, Experian, and TransUnion – once a year. Yep, totally free! Just head over to AnnualCreditReport.com. It’s a government-mandated site, so you know it’s legit and not trying to sell you a magic elixir.

Once you have your report, grab a comfy chair and a beverage of your choice. This isn’t a race! You’re looking for specific sections that might be whispering clues about your score’s descent.

The Usual Suspects: What to Look For

Let’s talk about the common culprits. These are the guys who most frequently cause a credit score to do a little jig downwards.

Payment History: The King of Credit Scores. This is by far the most significant factor. If you’ve missed a payment, even by a day or two (though most lenders give you a grace period), it can ding your score. Did you forget to pay a credit card bill? Missed a loan payment? Your credit report will show this clearly. It’s like leaving a negative review on a restaurant; it stays with you for a while. But here’s the uplifting part: making consistent, on-time payments from now on is the most powerful way to rebuild your score.

Credit Utilization Ratio: The Art of Not Maxing Out. Imagine your credit cards are like pizza slices. You have a certain amount of pizza available. Your credit utilization ratio is how much of that pizza you're actually eating. If you’re constantly finishing almost all of your pizza (maxing out your cards), it can signal to lenders that you might be a bit too reliant on credit. The golden rule here is to try and keep your utilization ratio below 30% for each card, and overall. So, if you have a $10,000 credit limit, try to keep your balances below $3,000. It’s a little bit of financial finesse!

Length of Credit History: The Wisdom of the Ages (of Credit). Lenders like to see that you've managed credit responsibly over a long period. The longer you've had credit accounts open and in good standing, the better. So, that old, rarely used credit card your grandma gave you? Don’t close it just yet! If it doesn’t have an annual fee and is in good shape, keeping it open can actually help your credit history length. It’s like letting your vintage wine age gracefully.

Credit Mix: Variety is the Spice of Financial Life. Having a mix of different types of credit – like credit cards, installment loans (like a car loan or mortgage) – can be a good thing. It shows you can handle different kinds of debt responsibly. But don’t go out and open a bunch of new loans just for the sake of it! This factor is less impactful than payment history or utilization, so it’s not worth stressing over.

New Credit Applications: Don’t Go On a Shopping Spree for Credit. Every time you apply for new credit, a “hard inquiry” is placed on your credit report. Too many hard inquiries in a short period can make you look like you’re desperately seeking credit, which can make lenders nervous. Think of it like showing up to too many job interviews at once; it can look a little desperate. Spreading out your credit applications is key. A few here and there? Totally fine. A dozen in a month? Maybe take a breath.

Making it Fun: Your Credit Score Adventure!

Okay, so finding out your score might have been a slight buzzkill. But let’s reframe this! This is your personal finance adventure! Instead of seeing it as a problem, see it as an opportunity to gain a superpower: financial literacy. And let’s be honest, being financially savvy is incredibly empowering. It means more control, more choices, and less stress.

Think of each step you take to understand and improve your credit score as leveling up in a game. You’re collecting knowledge and building skills. You can even make it a game with friends or family! Who can find the most surprising thing on their credit report? Who can come up with the most creative way to stay under their credit utilization limit?

Imagine this: you’re at a party, and someone mentions how hard it is to get a good interest rate on a loan. You, with your newfound credit detective skills, can casually chime in with some awesome advice. You become the go-to financial guru among your pals! How cool is that?

Learning about your credit score isn’t about restriction; it’s about unlocking possibilities. It’s about being able to confidently pursue your dreams, whether that’s buying a home, starting a business, or simply having the peace of mind that comes with financial stability.

Your Uplifting Takeaway: You’ve Got This!

So, your credit score took a little tumble? No biggie! The fact that you’re even looking into it means you’re already ahead of the game. You’re proactive, curious, and ready to learn. That’s the spirit of someone who can achieve anything!

Remember, your credit score is not a fixed destiny. It’s a reflection of your financial habits, and habits can be changed. It’s a journey, and every step you take towards understanding and improving it is a victory. You’re building a stronger financial future, one informed decision at a time.

So, dive into those credit reports! Become a credit score ninja! You’ll be surprised at how much you can learn, and even more surprised at how much fun you can have taking control of your financial well-being. This is just the beginning of your empowering financial adventure. Go forth and conquer your credit! You’ve totally got this!