How To Calculate Monthly Payment For Credit Card

Hey there, fellow humans navigating the wonderful, sometimes bewildering, world of plastic money! Ever stare at your credit card statement and feel a tiny knot of… well, something… in your stomach? It’s that little voice that whispers, “How much am I actually paying for that fancy coffee or those comfy new shoes?”

Don’t worry, you’re not alone! Understanding your credit card payments might sound like advanced calculus, but it’s actually more like figuring out how much pizza you get when you split a large with your bestie. We’re here to break it down in a way that’s as easy-going as a Sunday morning, so you can feel empowered and not overwhelmed.

Why Should You Even Bother? Let’s Get Real.

Okay, let's be honest. Sometimes, it's tempting to just pay the minimum. It feels like magic, right? Like the debt just shrinks on its own. But here’s the thing: that minimum payment is like a tiny seed trying to grow a whole forest. It’s going to take a loooong time, and you’ll end up paying a lot more in the long run.

Think of it like this: You borrowed $100 to buy a really cool gadget. If you only pay $5 a month, that $100 will likely turn into $120 or more by the time you’re done, thanks to interest. That extra $20 is like paying for the gadget twice! We’re trying to avoid that, folks. We want to get the most bang for our buck, and that means understanding how those payments work.

It’s also about financial peace of mind. Knowing exactly where your money is going, and how much you’re really paying for things, is like having a clear path through a confusing maze. No more surprises, no more that sinking feeling when you realize you’ve been paying interest on that impulse purchase for years.

The Nitty-Gritty: Interest Rates and How They Work

So, what’s this “interest” thing that makes our debt grow? Think of it as a fee you pay for borrowing money. Credit card companies charge you for the privilege of using their money now, and they charge it based on your Annual Percentage Rate (APR).

Your APR is usually a percentage. Let’s say your APR is 18%. This doesn't mean you pay 18% of your balance every single month. Phew! It’s actually divided by 12 (for the 12 months in a year) to get your monthly interest rate. So, an 18% APR is roughly a 1.5% monthly interest rate (18% / 12 = 1.5%).

This monthly interest rate is what gets applied to your outstanding balance. If you owe $1,000 and your monthly interest rate is 1.5%, that’s $15 in interest for that month alone. Ouch! And if you only pay the minimum, that $15 often gets added back into your balance, and you start paying interest on the interest. It’s like a snowball rolling downhill, getting bigger and bigger.

How to Calculate Your Monthly Payment (The Simplified Version)

Now, let’s get to the good stuff: calculating your payment. The truth is, credit card companies have fancy formulas. But we can get a pretty good idea by understanding the core components. Here’s the simplified breakdown:

Your Monthly Payment ≈ (Principal + Interest)

Where:

:max_bytes(150000):strip_icc()/CalculateCardPayments4-a6570a7d2e36410b9980f4833a4f8f6e.jpg)

- Principal is the amount of money you actually owe for purchases, minus any payments you’ve made.

- Interest is what you owe for borrowing the money.

Let’s take an example. Imagine you have a balance of $500 on your credit card. Your APR is 18%, which means your monthly interest rate is 1.5% (0.015 as a decimal). You decide you want to pay more than the minimum. Let’s say you aim to pay $50 this month.

Here’s how it might break down:

- Calculate the interest for the month: $500 (balance) * 0.015 (monthly interest rate) = $7.50. So, $7.50 of your $50 payment goes towards interest.

- Calculate the principal payment: $50 (your total payment) - $7.50 (interest) = $42.50. This is the amount that actually reduces your debt!

See? A good chunk of your payment goes to interest if you only pay the bare minimum. By paying $50, you’re reducing your principal by $42.50. That’s like giving your debt a good haircut!

The Minimum Payment Trap: A Cautionary Tale

Let’s stick with that $500 balance and 18% APR. If the credit card company’s minimum payment is, say, 2% of your balance or $25, whichever is greater. In this case, 2% of $500 is $10. So your minimum payment would be $25.

If you pay just the $25:

- Interest: $500 * 0.015 = $7.50

- Principal payment: $25 - $7.50 = $17.50

You’ve only reduced your debt by $17.50! And the next month, your balance will be $500 - $17.50 = $482.50, and you’ll start the cycle again. It’s like trying to bail out a sinking boat with a thimble. You’re technically doing something, but the progress is incredibly slow, and the boat (your debt) is still taking on water (interest).

Making Your Payments Work FOR You

The key takeaway here is that paying more than the minimum is your superpower. It’s the secret sauce to escaping credit card debt faster and saving yourself a ton of money in the long run.

How much should you pay? There’s no single magic number. It depends on your budget and how quickly you want to be debt-free. But here are some fun strategies:

- The “Extra Few Bucks” Approach: Even adding an extra $10 or $20 to your minimum payment can make a surprising difference over time. It’s like adding an extra sprinkle of fairy dust to your debt reduction efforts.

- The “Round Up” Method: If your payment is, say, $72.50, round it up to $75 or even $80. It’s a small mental adjustment that leads to a bigger impact.

- The “Pay Off a Small Purchase” Goal: If you’ve made a few smaller purchases, try to pay them off completely within a month or two. It feels amazing to see those zero balances pop up!

Tools to the Rescue!

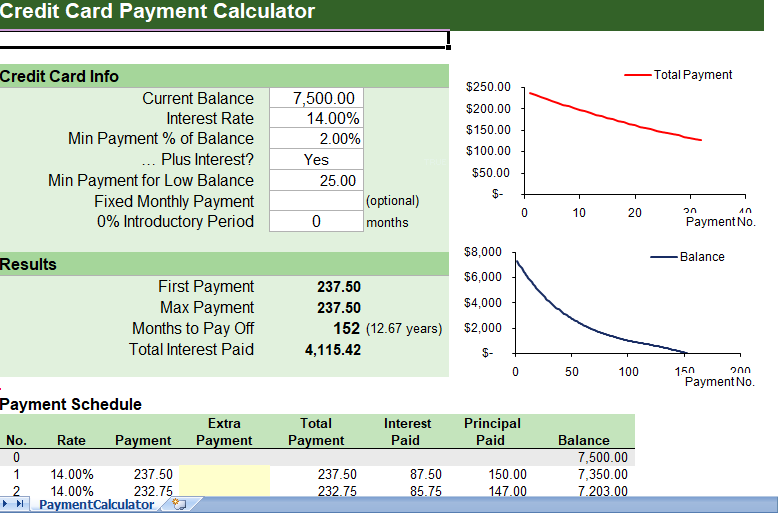

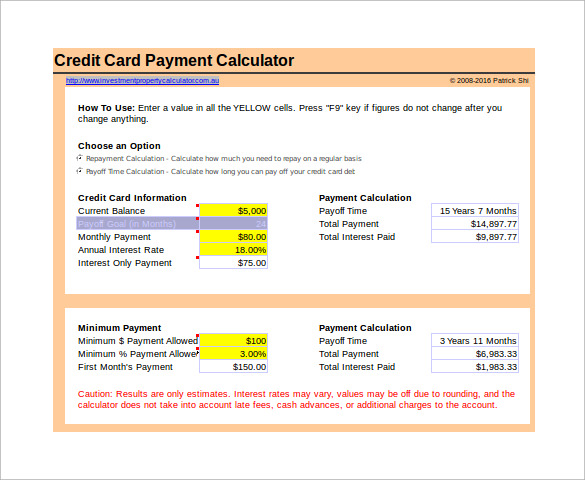

We’re not expected to be human calculators! Thankfully, there are lots of online tools and apps that can help you. Many credit card companies have payment calculators on their websites. You can also find free debt payoff calculators online. These tools can show you how long it will take to pay off your debt based on different payment amounts and interest rates.

Imagine inputting your balance and seeing a chart showing how quickly your debt disappears when you pay a bit more each month. It’s like watching a sad cloud turn into a bright, sunny sky! It can be incredibly motivating.

The Bottom Line: Be in Control!

Understanding your credit card payment isn’t about being a financial guru; it’s about being a smart consumer. It’s about knowing where your money is going and making it work for you, not against you.

So next time you look at that credit card statement, don’t let it intimidate you. Take a deep breath, remember the pizza-splitting analogy, and realize you have the power to control your financial destiny. By making informed payments, you’re not just paying off debt; you’re investing in your own future freedom and peace of mind. And that, my friends, is a beautiful thing.