How Often Can You Get Credit Limit Increases

Ever feel like your credit limit is playing hide-and-seek with your spending habits? You know, one minute you're feeling like a financial rockstar, ready to conquer that online shopping spree, and the next, BAM! Declas, declined, declined. It's the credit card equivalent of asking for a second helping of dessert and getting a stern look from the waiter. So, the burning question on many of our minds, especially after that spontaneous Amazon impulse buy (we’ve all been there!), is: How often can you actually get a credit limit increase?

Think of your credit limit like the gas tank in your car. Sometimes you cruise along, barely sipping from it, and other times, well, you’re flooring it, hoping you don’t run out of juice before you reach your destination (which, let’s be honest, is usually a brightly lit online store). And just like you wouldn't want to be stuck on the side of the highway with an empty tank, you don't want to be stuck in checkout purgatory with a maxed-out card.

The truth is, there's no magic number, no cosmic countdown clock that tells you when your credit card issuer will deem you worthy of more plastic power. It’s not like your birthday, where you get a year older and magically get a bigger slice of cake. Instead, it's more of a subtle dance, a constant evaluation by your card issuer, like a parent assessing if you've really cleaned your room or just shoved everything under the bed.

Some folks will tell you it's every six months, others say a year. And you know what? They might be right. For them. But for you, it could be different. It’s like asking your friend how often they get invited to exclusive parties – it totally depends on who you know and how well you play the game.

Let's break it down, shall we? Because understanding the "how" and "when" can feel as complicated as assembling IKEA furniture without the instructions, but way more rewarding.

The Usual Suspects: When Lenders Might Consider You

Most credit card companies aren't just handing out extra credit like free samples at Costco. They have their own set of rules, their own internal algorithms that are probably more complex than deciphering ancient hieroglyphics. But there are some general timeframes that tend to be the sweet spot.

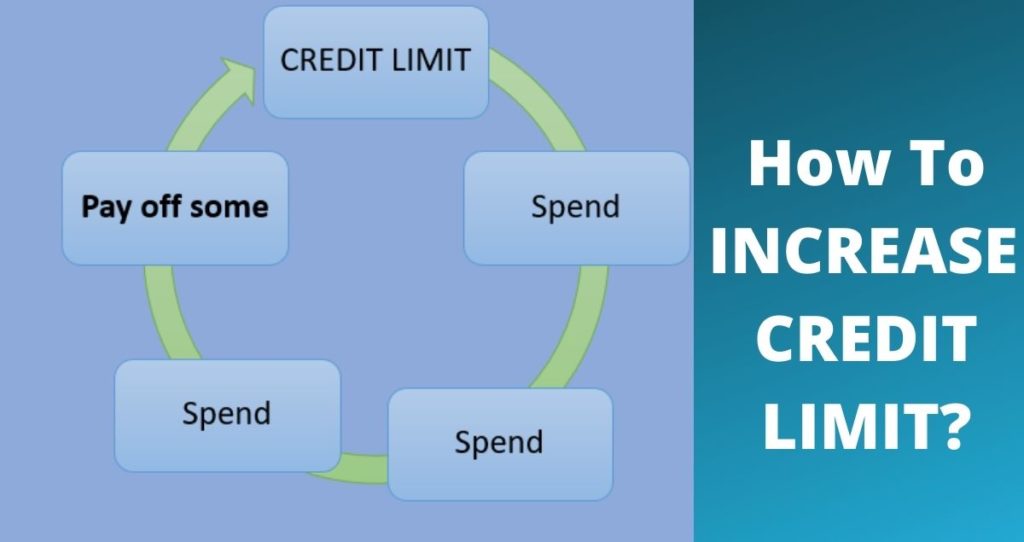

The "Six-Month Shuffle": This is a pretty common guideline you'll hear. After about six months of responsible card usage – meaning you're paying your bills on time, not maxing out your card every single month, and generally being a good credit citizen – many issuers will start looking at you with a bit more favor. Think of it as the probation period ending. You've shown you can handle the basic responsibilities, so maybe, just maybe, you're ready for more.

The "Yearly Upgrade": For some, especially if they're a bit more cautious with their spending or their credit history is a tad shorter, the six-month mark might be a bit ambitious. A full year of consistent, good behavior can also be a strong indicator. It's like getting a good report card for a whole school year – you've proven yourself over a longer stretch.

The "Automatic Overlords": Sometimes, the card issuers do it all by themselves. You wake up one morning, check your account, and poof! your credit limit has mysteriously (and wonderfully) increased. This is the best kind of surprise, like finding a twenty-dollar bill in an old jacket pocket. These automatic increases usually happen when you've been a stellar customer – consistently low utilization, perfect payment history, and maybe you've even been using the card for significant purchases. They’re basically saying, "You’re a rockstar! Here’s more firepower."

The "Aggressive Approach": And then there are those who like to be proactive. They know what they want and aren't afraid to ask for it. If you're feeling confident and have a solid credit track record, you can often request an increase yourself. More on that in a bit, but it's like going up to the barista and saying, "Can I get a venti latte instead of a grande?"

What's the Secret Sauce? Factors Lenders Actually Care About

So, beyond just the passage of time, what are these credit card overlords really looking for when they decide to sprinkle a little more credit dust on your account? It's not just about being a good customer; it's about being a profitable customer, and more importantly, a low-risk customer.

Payment History: Your Report Card for Life. This is the big one. If you've ever missed a payment, it’s like showing up to your credit review with a giant red "F" stamped on your forehead. Consistently paying your bills on time, every time, is the most crucial factor. It shows you're reliable, like that friend who always shows up early.

Credit Utilization: Don't Be a "Maxer-Outer." This is where people often trip up. Imagine your credit limit is a pie. Your credit utilization is how much of that pie you're eating. If you're eating 90% of the pie every month, the issuer starts to get nervous. They think you might be struggling. Ideally, you want to keep your utilization below 30%. Think of it as having a really big pie and only nibbling a small, polite slice. This is where those sneaky balance transfers can be a lifesaver, but that's a whole other article!

Length of Credit History: The "Seasoned" Consumer. Lenders like to see a history. A longer credit history, filled with good decisions, shows you have experience managing credit. It’s like a chef who’s been cooking for years versus someone who just learned to boil water. The seasoned chef is generally seen as more capable.

Number of Recent Inquiries: Don't Go on a Credit Application Spree. Applying for too many new credit cards in a short period can make lenders think you're desperate for cash or a flight risk. It's like showing up to a party with a dozen new friends everyone’s met before – it can raise some eyebrows. Stick to one or two applications a year, max, unless you have a very specific, well-thought-out plan.

Income and Employment Stability: Are You a Steady Eddy? While not always the primary driver for an increase on an existing card (they already know your income from when you applied), a stable income and employment situation certainly don't hurt. It’s like a stable job makes you a more reliable tenant, it makes you a more reliable borrower.

The "Ask Me Anything" Session: Requesting an Increase

Sometimes, waiting for that magical automatic increase feels like waiting for a bus that's always delayed. If you've been a good credit citizen and feel you qualify, why not just ask? It's like walking up to the ticket counter and saying, "Any chance of an upgrade?"

When to Ask:

- After a Significant Life Event: Did you get a raise? Land a better job? These are prime times to ask. It’s like saying, "Hey, I’m doing better, can I have more power?"

- After 6-12 Months of Good Behavior: As we discussed, this is the general sweet spot. You’ve proven yourself.

- When You've Been Using Your Card Consistently: If you’re regularly putting purchases on the card and paying them off, it shows you’re an active user.

How to Ask:

- The Phone Call: This is often the most direct route. Call the customer service number on the back of your card. Be polite, have your account information ready, and be ready to explain why you're asking (e.g., "I've been a loyal customer for X years, always pay on time, and I've recently had an increase in income. I'd like to request a credit limit increase.").

- Online Portal: Many card issuers have a section on their website or app where you can directly request an increase. This is usually quick and painless.

- The "Soft" vs. "Hard" Pull: When you request an increase, they might do a "soft pull" of your credit, which doesn't affect your score. Sometimes, especially if you're requesting a huge increase, they might do a "hard pull," which can slightly ding your score. They should tell you which one they're doing. If you're worried about your score, ask them first.

What to Expect:

They might approve you on the spot, give you a tentative approval pending review, or deny your request. If they deny it, don't get discouraged! Ask them why and what you can do to improve your chances for the future. It’s like a teacher giving you feedback so you can ace the next test.

Things That Can Put a Dampener on Your Credit Limit Dreams

Now, let's talk about the dream-crushers, the things that can make your credit card issuer say "nah" faster than you can say "buy now, pay later."

Late Payments: The Cardinal Sin. Seriously, this is the fastest way to kill your chances. It's like showing up to a job interview in pajamas – a definite no-go.

High Credit Utilization: Living on the Edge. As we mentioned, maxing out your cards consistently screams "risk." It's like driving a car with the gas light on perpetually – the issuer worries you'll break down.

Recent Credit Problems: Past Ghosts Haunting You. If you've had issues like defaults, bankruptcies, or a history of late payments in the past, it can take time to rebuild trust. The issuer needs to see a long, sustained period of good behavior.

Too Many New Accounts: The "Credit Hoarder." Applying for a bunch of cards at once can make you look like you're in financial distress.

Your Income Isn't Sufficient (for the increase requested): If you're asking for a massive jump in your limit but your income hasn't kept pace, they might decline. It's a basic math problem for them.

The "So, When?" Conclusion

So, to circle back to the original question: How often can you get a credit limit increase? The most honest answer is: It varies!

For many, a reasonable expectation is every six months to a year, provided you are using your credit responsibly. Some lucky ducks might get automatic increases more frequently if they’re exemplary cardholders. And if you’re proactive, you can often request one yourself after a solid period of good credit management.

The key takeaway isn't a specific number of months, but rather the consistent practice of good financial habits. Pay on time, keep your utilization low, and use your credit wisely. Think of it as tending to a garden. If you water it, give it sunshine, and pull out the weeds (late payments!), you’ll eventually get beautiful blooms (higher credit limits!).

And if you get denied? Don't sweat it! It's not a personal rejection. It's just a signal that you might need to work on a specific area. Then, you can try again down the line, armed with more knowledge and a cleaner credit report. Happy increasing!