How Much Should You Have In Savings? Updated Costs & Ranges

Let's talk about something a little less thrilling than a surprise pizza party, but way more important for your peace of mind: savings! Think of it as your financial superpower, your "just in case" fund that lets you tackle life's curveballs with a confident smile. While it might not be the first thing that pops into your head when you're dreaming of your next vacation, having a solid savings cushion is incredibly popular for a reason. It’s the quiet hero of financial well-being, enabling you to sleep soundly knowing you’re prepared for the unexpected. We're diving into how much you should have in savings, with a fresh look at today's costs and ranges. So, grab a comfy seat, maybe with that pizza you’ve been craving, and let's break it down!

Why Save? Your Financial Safety Net

The purpose of saving is pretty straightforward: to create a buffer between you and financial emergencies. Life is unpredictable. Your car might decide it's had enough and stage a protest on the highway, or you might face an unexpected medical bill. Without savings, these events can quickly spiral into a debt nightmare. But with a healthy savings account, you can handle them without derailing your long-term financial goals. The benefits are huge!

- Peace of Mind: This is arguably the biggest win. Knowing you have funds set aside dramatically reduces stress and anxiety about the unknown.

- Freedom and Flexibility: Savings give you choices. You can leave a job you dislike without immediately panicking, or take advantage of a great investment opportunity.

- Achieving Goals: From a down payment on a house to a dream vacation, savings are the engine that drives your aspirations forward.

- Avoiding Debt: Instead of reaching for high-interest credit cards when an emergency strikes, you can tap into your savings, saving yourself a ton of money on interest payments.

How Much is Enough? The Updated Ranges

So, the million-dollar question: how much should you actually have in savings? The old adage often points to a 3-6 month emergency fund. This is a fantastic starting point, and for many, it remains a solid target. However, the exact amount can fluctuate based on your personal circumstances, your lifestyle, and, of course, the current cost of living. Let’s break down what that range looks like today:

The 3-6 Month Emergency Fund: This is your foundational savings goal. It's designed to cover your essential living expenses if you were to lose your income unexpectedly. To calculate this, you need to look at your non-negotiable monthly expenses. Think rent or mortgage payments, utilities, groceries, transportation, insurance premiums, and minimum debt payments. For instance, if your essential monthly expenses total $3,000, then 3 months would be $9,000 and 6 months would be $18,000. It might sound like a lot, but remember, this is a goal, and you can build it up over time!

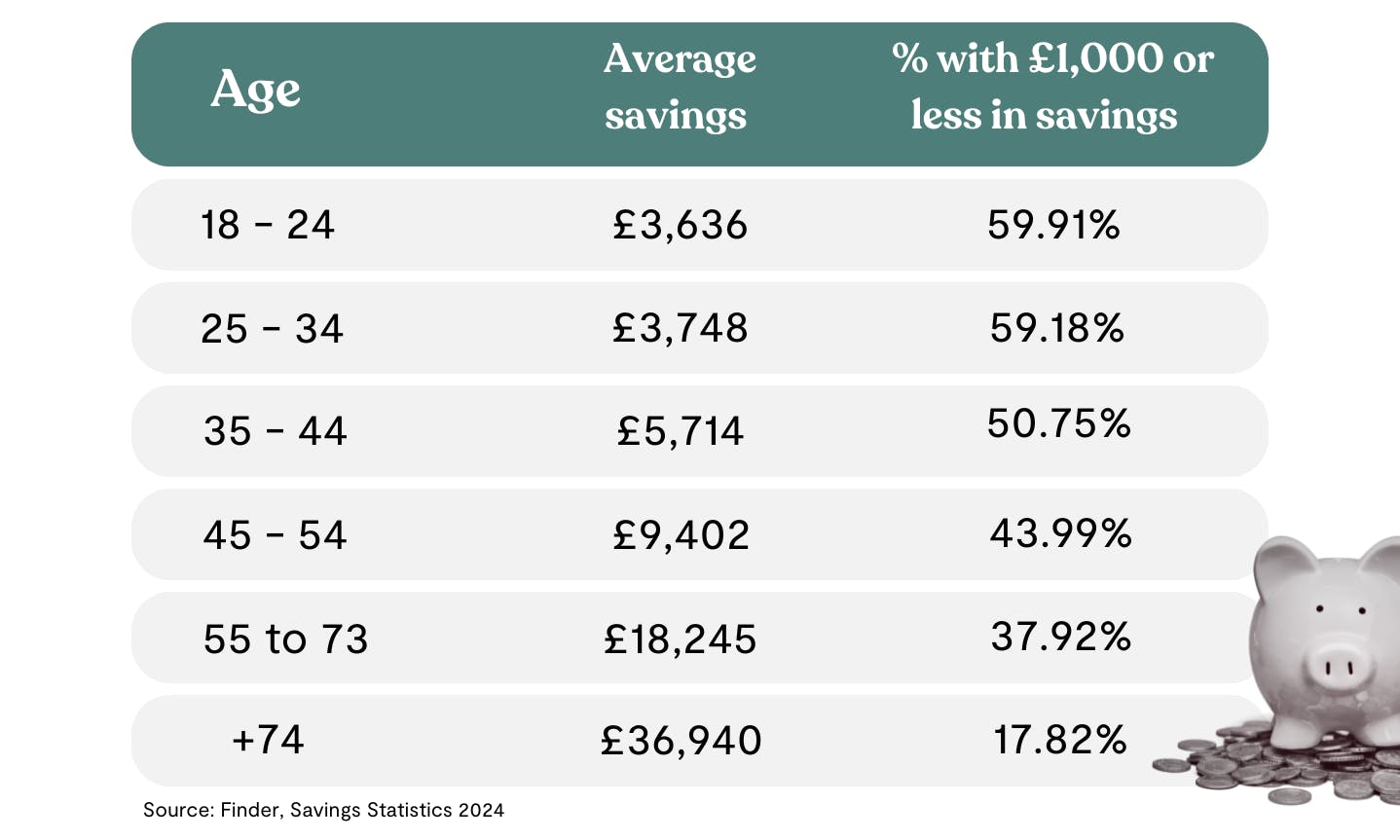

How Much You Should Have In Savings On Average By Age | Tembo blog

Factors Influencing Your Target:

- Job Security: If you work in a volatile industry or are self-employed with unpredictable income, aiming for the higher end of the 6-month range, or even a bit more, is wise. Conversely, if you have a very stable job with a company known for its security, you might feel more comfortable at the lower end.

- Dependents: Do you have children or other family members who rely on your income? Their needs will increase your essential monthly expenses and, therefore, your savings target.

- Health Considerations: If you or a family member has ongoing medical needs, a larger emergency fund can provide crucial peace of mind.

- High Deductible Insurance: If your health or auto insurance has a high deductible, you'll want to ensure your savings can cover that deductible in an emergency.

- Lifestyle: While we focus on essentials, some people prefer to have a bit more wiggle room for minor unexpected costs that aren't life-altering but can still be inconvenient.

Beyond the Emergency Fund: Other Savings Goals

:max_bytes(150000):strip_icc()/DW1-7adbbd3b079d483da37bebe1eaa9f15e.png)

While the emergency fund is paramount, it's not the only savings pot you should be thinking about. Consider these other popular and important savings goals:

- Short-Term Goals (1-3 Years): This could be for a down payment on a car, a vacation, or a new piece of furniture. The amount here is directly tied to the cost of the item or experience. If that dream vacation costs $5,000, that's your savings target for that goal.

- Medium-Term Goals (3-10 Years): This might include saving for a down payment on a house, funding further education, or starting a business. These require more significant planning and consistent saving.

- Long-Term Goals (10+ Years): The big one here is retirement. This is where long-term investing often comes into play, but the foundational principle of saving regularly is key. Your employer-sponsored retirement plan, like a 401(k) or 403(b), is a fantastic tool for this. Even small, consistent contributions can grow significantly over decades thanks to the magic of compounding.

The key takeaway is that "how much" is a personalized answer. Start by understanding your essential monthly expenses, and then build from there. Celebrate every milestone, no matter how small. Even saving an extra $50 a month is a step in the right direction. Your future self will thank you for it!