How Much Money To Retire At 50: Complete Guide & Key Details

So, you're dreaming of ditching the alarm clock and swapping TPS reports for tropical tans? Retiring at 50! It sounds like a fantasy whispered on a Friday afternoon, doesn't it? But guess what? For some lucky ducks, it's totally achievable. It’s like finding a hidden stash of your favorite cookies – pure joy!

The big question, the one that keeps you up at night pondering sprinkle counts on your imaginary retirement cake, is: How much moolah do you actually need? It's not as simple as pulling a number out of a hat, but we're going to break it down like a delicious pie. Think of this as your secret recipe for early freedom!

The Magic Number: It's Not Just One Size Fits All!

Here’s the thrilling truth: there isn't a single magic number that applies to everyone. Your retirement party might be catered with caviar, or it might involve a super-fancy picnic. Your lifestyle is the dictator here, the ringleader of your retirement circus.

Consider your current spending habits. Are you a "buy-my-coffee-from-that-trendy-place-every-day" kind of person, or do you whip up your own latte magic at home? The more you spend now, the more you’ll likely want to spend then. It's like expecting a bigger birthday bash if you're used to elaborate celebrations!

Your Dream Retirement: What Does It Look Like?

Imagine your perfect day at 50. Are you building sandcastles on a beach in Fiji, or are you happily tending to your prize-winning petunias? Do you plan to travel the globe like a seasoned explorer, or are you content with cozy nights in with a good book and a roaring fireplace?

Be brutally honest with yourself! If your dream involves daily spa treatments and private jet rides, well, that’s going to require a slightly larger mountain of cash. But if a peaceful life with hobbies and occasional getaways is your jam, then your target number will be a bit more… approachable.

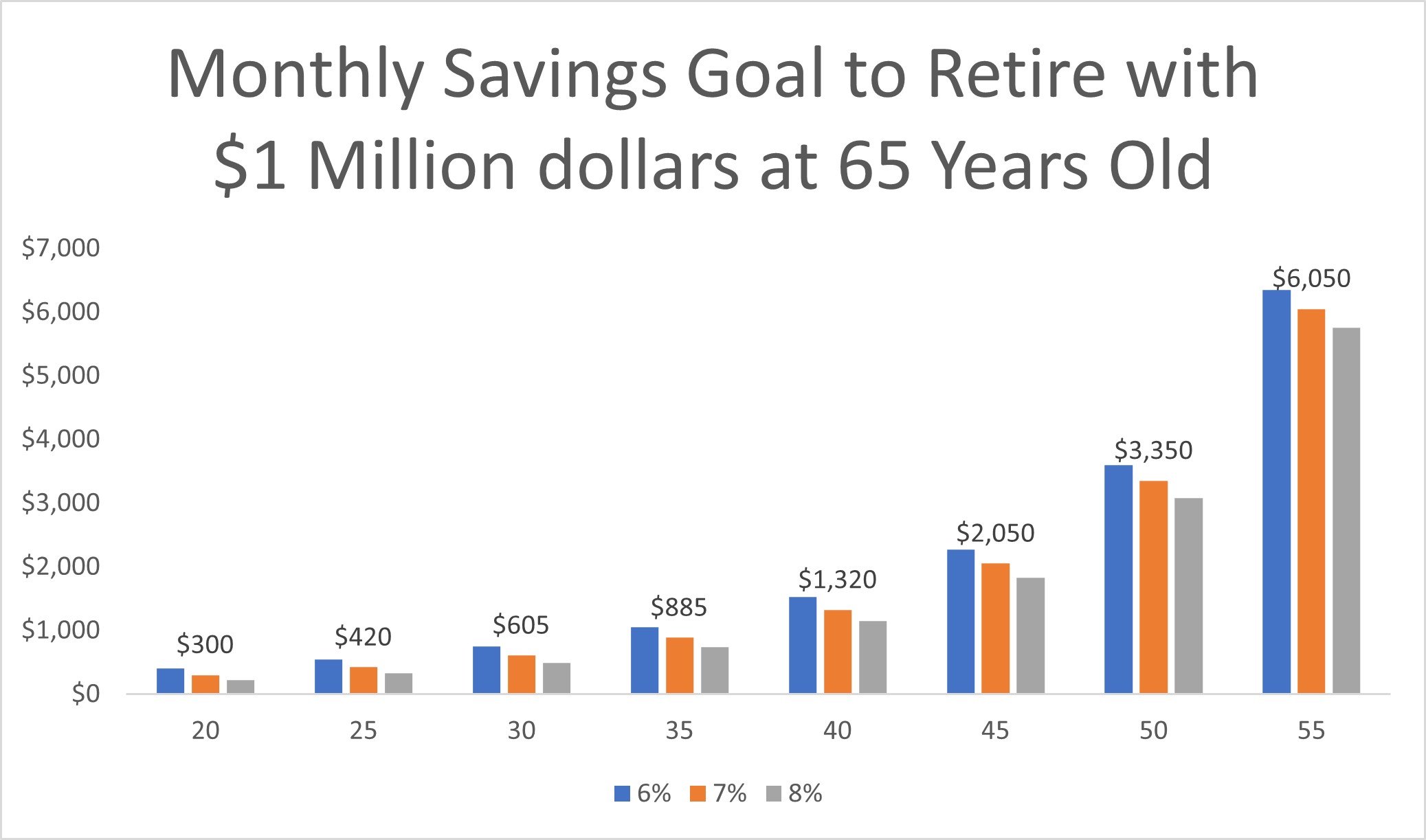

The 4% Rule: Your Friendly Retirement Compass

Okay, let's talk about a super-helpful concept called the 4% Rule. This is your golden ticket to understanding how much you can safely withdraw from your nest egg each year without running out of money. It's like having a magic money tree that replenishes itself!

Basically, the idea is that you can withdraw about 4% of your total retirement savings in your first year of retirement. Then, in subsequent years, you adjust that amount for inflation. So, if you have $1 million saved, you could theoretically withdraw $40,000 in your first year. Pretty neat, right?

Calculating Your Magic Number: Let's Do Some (Fun!) Math

So, to retire at 50 using the 4% rule, we need to work backward. First, estimate your annual expenses in retirement. Let's say you figure out you'll need $50,000 per year to live your fabulous early retirement life. This includes everything from your mortgage (or lack thereof!) to your epic travel fund.

Now, for the super-duper simple math: you take your desired annual income and multiply it by 25. That's because 100% divided by 4% is 25. So, for our $50,000 example, you’d need $50,000 x 25 = $1,250,000. Ta-da! That's your estimated nest egg goal. It sounds like a lot, but remember, it’s for a lifetime of freedom!

Where Does the Money Come From? Your Retirement Treasure Chests!

Now for the exciting part: how do you actually get all that shiny cash? It’s a multi-pronged attack, a financial superhero team-up! You've likely been building these treasure chests without even realizing it.

Your trusty 401(k) and IRA accounts are probably your biggest allies. These tax-advantaged accounts are like super-powered piggy banks. The government gives you breaks for saving in them, which is like getting bonus sprinkles on your ice cream!

Other Avenues to Early Riches

Don't forget about your investment accounts outside of retirement plans. If you've been wisely investing in stocks or bonds, that's another significant chunk of your potential retirement fund. Think of it as finding a secret compartment in your treasure chest!

And what about your house? If you own your home, you might consider downsizing, selling, or even doing a reverse mortgage later on. Your home equity can be a substantial resource. It’s like having a golden goose waiting in the wings!

The Not-So-Fun But Super-Important Details

Okay, deep breaths. We need to talk about a couple of things that aren't as glamorous as yachts and private islands, but are absolutely crucial for retiring at 50.

Healthcare is a biggie. Before Medicare kicks in at 65, you'll need to have a solid plan for health insurance. This can be a significant expense, so factor it into your calculations. It’s like the broccoli on your retirement plate – maybe not your favorite, but good for you!

Taxes: The Uninvited Guest

And then there are taxes. Oh, taxes. While your retirement accounts offer tax advantages during your working years and in retirement, you'll still have tax obligations. Understanding how withdrawals from different accounts are taxed is key. It's like realizing the party might end, but the memories (and the tax bill!) linger.

Consider consulting a financial advisor. They’re like your personal retirement sherpas, guiding you through the tricky terrain. They can help you create a personalized plan that accounts for your unique situation, your dreams, and yes, even your love for artisanal cheese.

The Power of Early Saving: Your Secret Weapon

The earlier you start saving, the more the magic of compound interest works its wonders. It’s like planting a tiny seed that grows into a giant money tree over time. Even small, consistent contributions can make a colossal difference when you're aiming for an early retirement.

Think about it: the money you save in your 20s and 30s has way more time to grow and earn returns than money saved in your 40s. So, if you're on this journey, celebrate every dollar you sock away. It's a victory dance in slow motion!

Making it Happen: A Playbook for the Aspiring 50-Something Retiree

Retiring at 50 isn't a pipe dream for a select few; it's a well-planned adventure for those who are strategic and disciplined. It requires a clear vision of your retirement lifestyle, a realistic understanding of your expenses, and a commitment to saving and investing diligently.

Start by crunching your numbers. Get a handle on your current spending and project your future needs. Then, aggressively ramp up your savings. Cut unnecessary expenses, negotiate a better salary, and make every dollar work harder for you. This is your time to be a financial ninja!

Embrace the Journey!

The path to retiring at 50 might have its challenges, but the reward – a life of freedom, flexibility, and fun – is absolutely worth it. It’s about designing a life you truly love, on your own terms. So, dust off that dream board, start saving with gusto, and get ready to say goodbye to the daily grind at an age most people are still climbing the corporate ladder!

Remember, this is your life, your retirement, and your adventure. With a solid plan and a sprinkle of determination, retiring at 50 can be your reality. Now go forth and conquer your financial future, you magnificent early retiree-in-the-making!