How Long Does It Take To Reestablish Credit

Hey there, credit champions and aspiring credit wizards! Let’s talk about something that can feel a bit like a, well, a long and winding road: reestablishing your credit. We’ve all been there, right? Maybe a few too many impulse buys during the early 2000s (remember when buying things online was still a novelty?), a rocky patch in your career, or just life throwing a few curveballs. Whatever the reason, your credit score might be whispering rather than shouting its approval.

But here’s the good news: it’s absolutely possible to get that score back in fighting shape. Think of it less like a sprint and more like a leisurely hike with some stunning views along the way. Today, we’re diving into the nitty-gritty of how long it actually takes to reestablish credit, sprinkled with some practical tips, a dash of pop culture, and the kind of relaxed vibe you’d find sipping a latte at your favorite coffee shop.

The Great Credit Comeback: Setting Expectations

First things first, let’s ditch the idea of an overnight miracle. Rebuilding credit isn't like ordering a pizza that arrives in 30 minutes or less. It's more of a slow burn, a gradual process of proving to lenders that you’re a reliable borrower. And the timeline? It’s not a one-size-fits-all answer. It depends on a few key factors:

- The severity of past issues: Were we talking about a single late payment or a full-blown bankruptcy?

- Your current financial habits: Are you ready to be super responsible from here on out?

- The methods you use to rebuild: Some strategies can speed things up more than others.

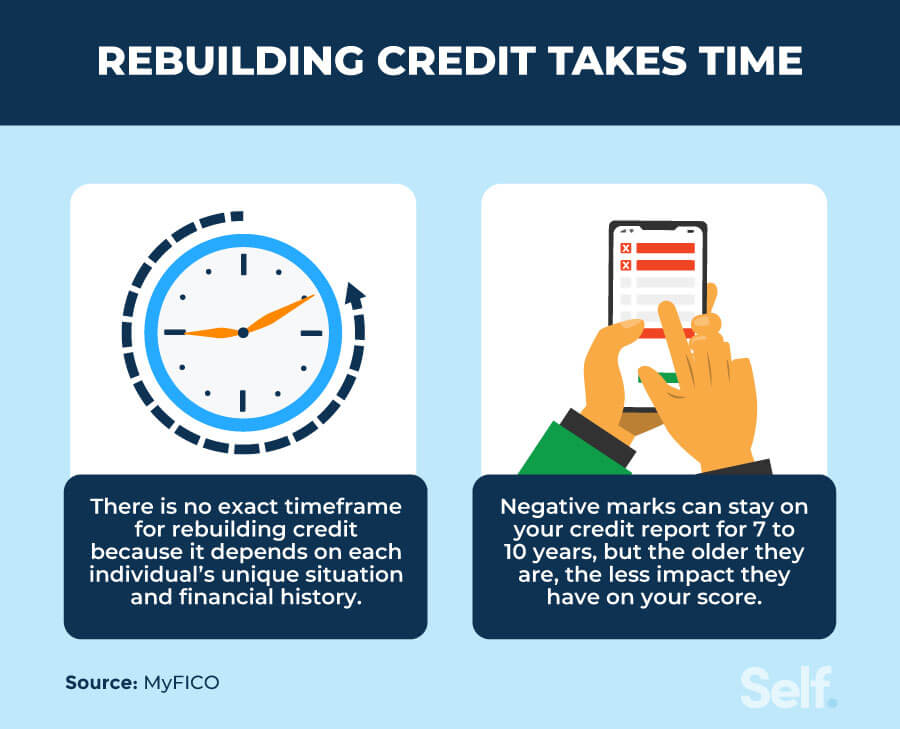

Generally speaking, you can start seeing noticeable improvements in your credit score within 6 to 12 months of implementing a solid rebuilding strategy. However, a truly robust and healthy credit score, the kind that gets you that dream apartment or a sweet interest rate on a car loan, often takes 1 to 3 years. And for more severe issues like bankruptcy, it can take longer, with the impact often lingering for up to 7 or 10 years, depending on the type of bankruptcy.

Think of your credit score like a friendship. It takes time to build trust and a solid reputation. You can’t just skip a few months of calling your bestie and expect them to be instantly fine with you borrowing their favorite sweater again. It requires consistent effort and showing you’ve learned from past missteps.

The Building Blocks: What Really Matters

So, what exactly are the lenders looking at when they decide if you’re credit-worthy again? It boils down to a few core components of your credit report:

1. Payment History (The Big Kahuna): This is, by far, the most important factor, accounting for about 35% of your FICO score. Making payments on time, every time, is your golden ticket. Even a single late payment can ding your score, but consistent on-time payments will slowly but surely rebuild trust. It's like showing up for work every day, even when you’d rather be binge-watching that new Netflix series. Reliability is key!

2. Amounts Owed (Don’t Overextend): This looks at how much credit you’re using compared to your total available credit. Keeping your credit utilization ratio low – ideally below 30%, but even better below 10% – is super crucial. Maxing out your credit cards tells lenders you’re living on the edge. Imagine a superhero trying to save the day while juggling five flaming chainsaws. It’s a lot of pressure!

3. Length of Credit History (The Grandkids of Your Credit): The longer you’ve had credit accounts in good standing, the better. This shows lenders you have experience managing credit over time. So, that old store credit card you opened in college? Keep it open and in good standing if it has no annual fee, even if you rarely use it. It’s like your credit history’s wise old grandparent, adding a touch of experience.

4. Credit Mix (Variety is the Spice of Life): Having a mix of different types of credit – like credit cards, installment loans (think car loans or mortgages) – can be a good thing. It shows you can manage various forms of debt responsibly. But don’t go opening up a bunch of new accounts just to diversify; that can backfire. It’s about showing you can handle different flavors, not about stuffing your face with every dessert on the menu.

5. New Credit (Don’t Be Too Eager): Applying for too many credit accounts in a short period can make you look desperate and risky to lenders. Each hard inquiry (when you apply for credit) can slightly lower your score. Pace yourself! It’s like trying to get a date with everyone at a party simultaneously – it can come across a little… intense.

Your Rebuilding Toolkit: Strategies for Success

Alright, now for the fun part – the actual strategies you can use to get that credit score back on track. Think of these as your trusty sidekicks in the quest for financial freedom.

1. Secured Credit Cards: Your Credit-Building Stepping Stone

This is often the first port of call for those starting from scratch or rebuilding. How do they work? You put down a security deposit, which then becomes your credit limit. It’s essentially a debit card with a credit card wrapper. You use it, pay it off, and the issuer reports your activity to the credit bureaus. It’s like training wheels for your credit, allowing you to practice responsible spending without too much risk.

Pro-Tip: Look for secured cards that have no annual fee and report to all three major credit bureaus (Equifax, Experian, and TransUnion). Some cards even have a clear path to graduating to an unsecured card after a period of good behavior, which is super motivating!

2. Credit-Builder Loans: Practicing Financial Discipline

These are small loans designed specifically for building credit. You make regular payments, and the money you pay is often held in a savings account until the loan is repaid. Once paid off, you get the money back. It's a fantastic way to demonstrate your ability to make consistent payments. It's like a mini-financial boot camp, getting you in shape for bigger credit goals.

Fun Fact: Some credit unions offer these. They're often more community-focused and might be more willing to work with you.

3. Authorized User: Riding Coattails (Wisely!)

If you have a trusted friend or family member with excellent credit, they can add you as an authorized user on their credit card. Their positive payment history can then appear on your credit report, giving your score a potential boost. However, this is a two-way street. If they miss payments or run up high balances, it can hurt you too. So, choose wisely, and have a clear understanding with the cardholder.

Cultural Reference: Think of it like being part of a well-oiled machine. You’re benefiting from the smooth operation, but you also have to contribute to its success.

4. Pay Down Debt Aggressively: Less is More

If you have existing debt, especially on credit cards, making a concerted effort to pay it down is crucial. Lowering your credit utilization ratio (remember that 30% rule?) is a powerful way to improve your score. Focus on paying down the cards with the highest interest rates first (the "avalanche" method) or the smallest balances first for quick wins (the "snowball" method). Whatever works for your brain and your motivation!

Entertainment Nod: It’s like decluttering your digital life. Getting rid of those old digital files (debts) makes your whole system run smoother and faster!

5. Monitor Your Credit Report: Be Your Own Detective

You're entitled to a free credit report from each of the three major bureaus annually at AnnualCreditReport.com. Stalking your own credit report might sound a little creepy, but it’s essential! Check for errors, inaccuracies, or fraudulent activity. If you spot something amiss, dispute it immediately. You’re the guardian of your financial identity!

Culture Clash: In the age of instant information, it's easy to forget the importance of diligence. But when it comes to your credit, a little old-school detective work goes a long way.

6. Be Patient and Consistent: The Long Game Wins

This is perhaps the most important piece of advice. Rebuilding credit takes time and consistent effort. There will be days when it feels like you’re not making progress, but stick with it. Small, consistent positive actions will compound over time. Think of it as tending to a garden. You water it, weed it, and give it sunlight, and eventually, it blossoms.

The Timeline Revisited: When Can You Expect the Magic?

Let’s put some (flexible) dates on this. If you’re starting with a severely damaged credit history or rebuilding from scratch:

- Months 1-6: You’ll likely see some initial movement. This is when you establish new, positive habits with secured cards or credit-builder loans. Your score might tick up a few points as you demonstrate reliability. It’s like the first few green shoots in your garden.

- Months 6-12: Expect more significant progress. As your history of on-time payments grows and your utilization remains low, your score should climb more noticeably. You might start getting pre-approved offers (but be cautious about applying for too many!). This is when your garden starts to look lush.

- 1-3 Years: This is where you'll likely achieve a good, solid credit score. You’ll have a substantial positive payment history, a healthy credit mix, and responsible utilization. Lenders will see you as a low-risk borrower. Your garden is now in full bloom, and you’re enjoying the fruits (and flowers) of your labor.

Outstanding Info About How To Restore Credit - Pricelunch34

Outstanding Info About How To Restore Credit - Pricelunch34 - 7-10 Years: The more severe negative marks, like bankruptcies, will eventually fall off your credit report. While their impact lessens over time, they might still be visible for a while. Think of these as stubborn weeds that eventually wither away.

Remember, these are general timelines. Your journey is unique!

A Little Bit of Whimsy: Credit Quirks and Fun Facts

Did you know that the FICO score, the most widely used credit scoring model, was created by Fair Isaac Corporation? It’s been around since 1989! And that credit reports don’t actually contain your credit score itself, but the information that credit scoring companies use to calculate your score? It’s like getting a report card on your financial behavior.

Also, the concept of credit itself is ancient. Early forms of credit existed in ancient Mesopotamia and Rome. So, while our credit cards might be sleek and modern, the idea of borrowing and repaying is as old as civilization itself!

The Daily Grind: Connecting Credit to Your Life

So, why does all of this matter in the grand scheme of your day-to-day life? Well, your credit score is like the quiet engine under the hood of your financial life. It affects whether you can get that apartment you’ve been eyeing, the interest rate on your car loan (think of all the road trips you can have with lower payments!), and even the cost of your insurance premiums.

Think about it: a better credit score means more disposable income, less stress about financial emergencies, and the freedom to pursue those big life goals. It’s not just about numbers on a report; it’s about unlocking opportunities and living with a little more ease.

Rebuilding credit is a marathon, not a sprint. It requires patience, discipline, and a willingness to learn. But with the right strategies and a consistent approach, you can absolutely transform your financial future. So, take a deep breath, grab your favorite comfy socks, and start building that credit powerhouse. You’ve got this!