Do Medical Bills In Collections Affect Your Credit

Ah, medical bills. They’re like that surprise guest who shows up uninvited to your perfectly planned party, except instead of bringing a questionable casserole, they bring a hefty tab. And then, sometimes, those medical bills decide to go on an adventure. An adventure into the land of collections. It’s enough to make you want to bury your head in a pillow and pretend it’s not happening, right? We’ve all been there, staring at a bill that makes our eyes water more than the actual procedure itself. It’s like trying to decipher ancient hieroglyphs, but instead of learning about pharaohs, you’re learning about co-pays and deductibles that seem to have a mind of their own.

So, the big question on everyone’s mind, usually whispered in hushed tones over a strong cup of coffee (or something stronger), is: Do these medical bills, when they’re being chased down by collectors, actually mess with our precious credit scores? The short answer, my friends, is a resounding, eye-rolling, "yes, but let's break it down so it doesn't feel like a scene from a horror movie." Think of your credit score like your financial report card. You know, the one you used to dread getting from your parents after a particularly challenging semester? Well, this is the adult version, and medical bills in collections are like that one C-minus that keeps glaring at you from the top of the page, even though you aced all your other subjects.

Let's paint a picture, shall we? You've had a minor emergency, nothing too dramatic, maybe you tripped over your own enthusiasm while trying to catch a falling remote control. You go to the doctor, get patched up, and are sent home with a smile and a prescription. Easy peasy. Then, weeks later, a bill arrives. And another. And then, a letter that’s slightly more official-looking than your usual junk mail arrives. This, my friends, is the gentle nudge (or perhaps a not-so-gentle shove) that your bill has been handed off to a collection agency. It’s like when your favorite toy goes missing, and then you find out your little cousin "borrowed" it and hasn't put it back yet. Except this "borrowing" has financial implications that can linger longer than a bad case of the flu.

The Nitty-Gritty: How It Works

When you owe money for medical services, and you haven't paid it, the healthcare provider will often try to collect it themselves. They'll send you reminders, perhaps even call you. It's like your mom reminding you to clean your room – sometimes effective, sometimes met with a dramatic sigh. If those efforts don't yield results, they might sell the debt to a third-party collection agency. This agency then becomes the new "owner" of your debt, and their job is to get you to pay. They're like those persistent telemarketers who somehow always call when you're about to eat dinner, except they're calling about something you actually owe.

And here's where the credit score dragon awakens. Once a medical debt is sent to collections, it can absolutely appear on your credit report. This is the part that makes people want to retreat under their duvet. Imagine your credit report as a social media profile for your financial life. It lists all your financial interactions: loans, credit cards, and yes, even those overdue medical bills that have been forwarded to a debt detective. If a collection account shows up, it's like a friend posting an embarrassing photo of you without your consent. It’s out there, for all the world (or at least, the lenders) to see.

The Impact on Your Credit Score

So, how does this unwelcome guest affect your credit score? Think of your credit score as a delicate ecosystem. A healthy score is like a thriving rainforest, full of life and opportunities. A damaged score is more like a desert, barren and a bit depressing. When a medical bill goes to collections, it's a significant negative mark. It signals to lenders that you've had trouble managing your financial obligations. It's not like forgetting to water your houseplants; it's more like forgetting to pay your rent for a few months. It's a bigger deal.

The presence of a collection account on your credit report can drag your credit score down. How much it drops depends on several factors, including your existing credit history. If you have a generally strong credit profile, one collection might have a less severe impact than if your credit is already a bit shaky. It’s like adding an extra sprinkle of salt to an already seasoned dish. If the dish is perfect, the salt is noticeable. If it’s a bit bland, maybe it helps, but in this case, it's usually not for the better.

This lowered score can make it harder to get approved for things like a new credit card, a car loan, or even a mortgage. Lenders see that collection account and might think, "Hmm, this person isn't the most reliable with their payments." It’s like trying to get a second date after you accidentally wore socks with sandals to the first one – the impression isn't great.

The Good News (Yes, There’s Good News!)

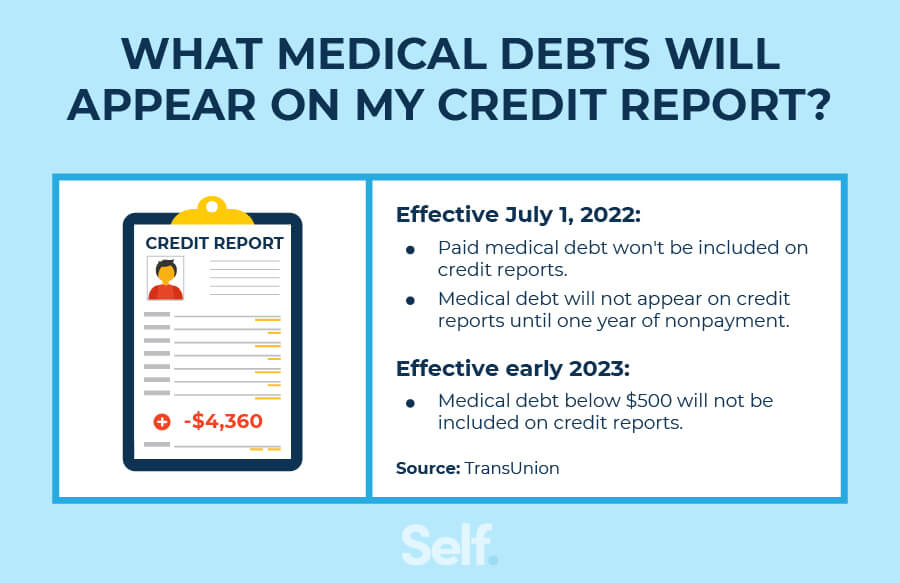

Now, before you start hyperventilating into a paper bag, let's talk about some silver linings. The world of medical debt and credit reporting is a bit of a unique beast, and there have been some important changes made to make things a little less terrifying. As of recent years, there are now stricter rules about when medical debt can appear on your credit report.

Here's the scoop: Medical collection debt typically won't appear on your credit report until it's at least a year old. This gives you a significant window of time to address the bill before it potentially impacts your credit. It’s like getting a warning before your internet goes out completely – you have time to fix the router. Plus, if you pay off a medical collection debt, it should be removed from your credit report. This is a big deal! Unlike some other types of debt, where the negative mark can linger for years even after it's paid, medical collections are often treated differently.

This removal after payment is a game-changer. It’s like finding out that embarrassing photo your friend posted has been deleted from the internet. Ah, sweet relief! It means that once you've settled the bill, you can often get back on track with your credit health relatively quickly, without that persistent shadow hanging over you.

What Can You Do? Tackling the Medical Bill Beast

So, what's the best strategy when faced with a medical bill that's headed for collection land? First off, don't ignore it. I know, I know, the urge to pretend it doesn't exist is strong. It's like when you see a spider in the bathroom – the instinct is to freeze and hope it goes away. But unfortunately, ignoring bills doesn't make them disappear. It usually just makes them angrier.

Communicate is key. If you receive a bill you can't afford, contact the healthcare provider's billing department immediately. Explain your situation. They might be willing to work out a payment plan with you. Many hospitals and clinics have financial assistance programs or can offer discounts if you're struggling. It’s like trying to negotiate with a stubborn toddler – sometimes a little back-and-forth can go a long way.

If the bill has already gone to collections, contact the collection agency directly. Don't be intimidated! You have rights. You can ask them for validation of the debt, which means they have to prove you actually owe it. You can also try to negotiate a settlement. Sometimes, they'll be willing to accept a lower amount than what you originally owed, especially if you can pay it off in one lump sum. It’s like finding a coupon for that item you really want – you save some money!

And remember, if you pay off the collection debt, make sure to get confirmation that it will be removed from your credit report. Get this in writing! It’s your little financial peace treaty. Once that collection account is gone, your credit score has a much better chance of bouncing back.

A Little Perspective

Life throws curveballs, and sometimes those curveballs come in the form of unexpected medical expenses. It’s a common human experience, and it’s easy to feel stressed and alone when dealing with debt. But remember, your credit report is just a snapshot of your financial life. A medical bill in collections can definitely impact it, but it's not the end of the world. With proactive communication, a willingness to negotiate, and an understanding of your rights, you can navigate these tricky situations and keep your financial future on the right track. Think of it as a temporary detour, not a permanent roadblock. You’ve got this!

So, the next time you get a bill that makes you sweat, take a deep breath. Remember that knowledge is power. And a little bit of calm negotiation can go a long way in keeping your credit score as healthy as your newfound well-being. It's all about managing the unexpected, one bill at a time, with a bit of strategy and maybe a good dose of humor.