Credit Score Needed For Victoria Secret Credit Card

Okay, confession time. A few years back, I was obsessed. Like, truly, deeply, head-over-heels obsessed with Victoria's Secret. Their PINK section? A dangerous siren song for my wallet. I swear, every time I walked past one of their stores, a little glitter bomb went off in my brain, whispering sweet nothings about sparkly hoodies and super-soft leggings. And you know what fuels that kind of dedication? Rewards points, baby! So, naturally, I started eyeing up their credit card. I pictured myself swiping with an extra little flourish, earning enough angel wings (or whatever they called them back then) to practically fly to the moon on a cloud of discounted lingerie. But then came the nagging question, the one that haunts every aspiring cardholder: what kind of credit score do I actually need?

It’s like that moment when you’re about to ask someone out, and you’re mentally running through all the potential rejection scenarios. Except, in this case, the rejection comes from a plastic rectangle with your name on it. And let's be honest, nobody wants their dreams of affordable angel wings to be crushed by a strict credit bureau. So, I did some digging. A lot of digging. Because if I’m going to spend my hard-earned cash on lacy things, I want to be sure I'm getting the most bang for my buck, and that includes unlocking the sweet, sweet perks of a store credit card.

The Victoria's Secret credit card, you see, isn't just any old card. It's a gateway. A portal to exclusive sales, birthday treats, and, of course, those coveted rewards. Think of it as your backstage pass to the fashion show of your dreams, minus the actual runway and the awkward stage fright. But to get that pass, you need a certain... credibility. And that, my friends, is where the credit score comes in. It’s like the bouncer at the club of retail dreams. Too low, and you’re politely (or not so politely) shown the door.

So, What's the Magic Number for VS?

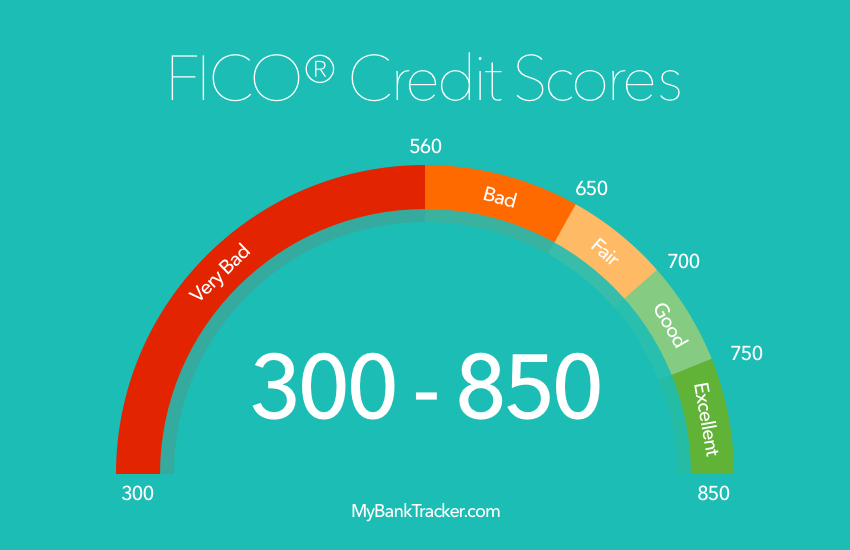

Alright, let's cut to the chase. What's the credit score "sweet spot" for snagging yourself a Victoria's Secret credit card? Drumroll, please... it's generally considered to be in the fair to good range.

Now, I know what you're thinking. "Fair? Good? What does that even mean?" It’s a bit like trying to guess the ideal temperature for a perfect cup of coffee – everyone has their preference! But in the world of credit scores, these terms have some pretty defined boundaries.

Generally speaking:

- Poor credit: Usually below 580. This is where things get a little tougher.

- Fair credit: Typically between 580 and 669. This is where the Victoria's Secret card starts to become a real possibility.

- Good credit: Usually from 670 to 739. With this range, you've got a pretty strong shot.

- Very good to excellent credit: 740 and above. You're practically golden.

So, if your score is hovering in that 580 to 739 zone, you're in a pretty good position to apply. Think of it as the "maybe" category that leans heavily towards a "yes." If you’re closer to the 670 mark and above, you're practically a shoo-in. It’s like having an inside track on those limited-edition holiday collections.

![HOW to do the Shopping Cart Trick Tutorial [2023] |Victoria's Secret](https://i.ytimg.com/vi/5EjkTLF5XvE/maxresdefault.jpg)

But Wait, There's More! (Isn't There Always?)

Here's the kicker, and it's a pretty important one. Victoria's Secret, like many retailers, partners with a larger credit issuer for their cards. Right now, that's Comenity Bank. And Comenity Bank has its own set of underwriting standards. This means that even if the general consensus is "fair to good," your application is still going to be evaluated on a bunch of factors.

Your credit score is a huge piece of the puzzle, no doubt. But it's not the only piece. They'll also look at:

- Your income: Can you actually afford to pay back what you spend? This is a big one. Lenders want to see that you have a stable income that can handle your existing debts and any new ones you might take on.

- Your debt-to-income ratio (DTI): This is basically a comparison of how much you owe versus how much you earn. A lower DTI generally looks better. Nobody wants to see you drowning in debt before you even get the card.

- Your credit history: Have you been responsible with credit in the past? Late payments, defaults, bankruptcies – these will definitely weigh against you. Conversely, a long history of on-time payments is a big plus.

- How many credit accounts you have open: Sometimes, having too much credit can be a red flag. It can suggest you're overextended.

- How many recent credit inquiries you have: Applying for a bunch of credit cards in a short period can temporarily ding your score. So, don't go on a credit-applying spree right before you decide you need that VS card.

So, while that 580-669 range is a good benchmark, having a bit more breathing room above that, especially if your other financial ducks are in a row, will definitely increase your chances. Think of it as having your credit score as the main star, but your income and payment history are the very important supporting actors.

I remember a friend of mine, bless her heart, her credit score was right on the cusp. She had a decent income, but a few late payments from a really rough patch a few years prior. She applied, and… denied. Ouch. It wasn't that her score was terrible, but those other factors just tipped the scales. It was a tough lesson, but a good reminder that it's a holistic picture.

What If My Score Isn't Quite There Yet?

Don't despair, my fellow fashion enthusiasts! If your credit score is currently chilling in the "fair" to "poor" category, it doesn't mean your dreams of VS rewards are dead in the water. It just means you need to do a little bit of pre-gaming before you hit that "apply" button.

Step 1: Check Your Credit Report (It's Free!)

First things first, you need to know where you stand. You're entitled to a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once a year. Websites like AnnualCreditReport.com are your official go-to for this. Don't just guess your score; know your score. You might even find errors on your report that are dragging your score down, which you can then dispute. Imagine finding out you have an incorrect late payment that's costing you points – talk about a plot twist!

Step 2: Focus on Building Your Score

This is the marathon, not the sprint. But the rewards are totally worth it. Here's what to prioritize:

- Pay bills on time, every time: This is hands-down the most crucial factor. Payment history accounts for a massive chunk of your credit score. Set up automatic payments, use calendar reminders, do whatever it takes. Even one late payment can have a significant impact.

- Keep credit utilization low: This is the amount of credit you're using compared to your total available credit. Ideally, you want to keep this below 30%, and even better, below 10%. If you have a card with a $1,000 limit, try not to carry a balance higher than $300. This shows lenders you're not relying heavily on credit.

- Avoid opening too many new accounts at once: As mentioned earlier, each application can result in a "hard inquiry," which can temporarily lower your score. Be strategic.

- Don't close old accounts (if they're in good standing): The length of your credit history matters. An older account with a good payment record can actually help your score.

Step 3: Consider a Secured Credit Card

If your score is really low or you have no credit history, a secured credit card is your best friend. You make a security deposit, which then becomes your credit limit. It's a fantastic way to build or rebuild credit responsibly. Use it for small purchases and pay it off diligently. It's like a training wheels program for credit cards.

Some retailers, including those who partner with Comenity, might even offer store cards with lower entry barriers for those with less-than-perfect credit. These are sometimes called "store-specific" cards or "private label" cards, and they can be a stepping stone to better credit products.

The Perks of Being an Angel (Cardholder)

Okay, so why all this fuss about a credit card? What are the actual benefits of getting the Victoria's Secret card? Well, if you're a regular shopper, the rewards can add up pretty nicely.

Typically, you'll earn points for every dollar you spend. These points can then be redeemed for discounts, gift cards, or exclusive offers. Think of it as getting paid to shop for your favorite bras and loungewear. Pretty sweet, right?

Beyond the points, there are often other perks:

- A welcome offer: Usually a discount on your first purchase or a statement credit when you open and use the card.

- Birthday surprises: A little treat from Victoria's Secret to celebrate your special day.

- Exclusive access to sales and promotions: Cardholders often get early access to big sales events, like Semi-Annual Sale, so you can snag the best deals before they're gone.

- Free shipping offers: Sometimes you'll get free shipping thresholds that are lower for cardholders.

It’s basically like being part of an exclusive club. And who doesn't like feeling a little exclusive, especially when it comes to shopping for comfy PJs?

When I finally got approved for my own store card (not VS, but a similar retailer!), I felt this ridiculous surge of accomplishment. It was just a credit card, I know, but it represented progress. It meant I was doing something right with my finances. And, of course, it meant discounted new sweaters. So, the motivation is two-fold: financial responsibility and retail therapy. A winning combination, if you ask me.

The Bottom Line: It's Achievable!

So, to recap: for the Victoria's Secret credit card, you're generally looking at needing a credit score in the fair to good range (approximately 580-739). However, remember that your score is just one part of the equation. Your income, credit history, and debt-to-income ratio also play significant roles.

If your score is a little lower than you'd like, don't get discouraged! Focus on building good credit habits: pay your bills on time, keep your credit utilization low, and be mindful of new applications. A secured credit card can be a great way to start rebuilding.

The Victoria's Secret credit card can be a rewarding way to save money on your favorite purchases if you're a frequent shopper. Just remember to use it responsibly, pay off your balance in full each month to avoid interest charges, and treat it as a tool to enhance your shopping experience, not as a way to spend beyond your means.

Now go forth, check your credit, and may your applications be ever in your favor. And if you get approved? Treat yourself to something fabulous. You've earned it!