Can I Get A Mortgage At 50? What To Know

Thinking about buying a home at 50? Fantastic! It’s a milestone that many people reach, and guess what? It’s absolutely possible to snag a mortgage at this age. In fact, it’s becoming increasingly common, and for good reason. Many folks are finding themselves in a great financial position in their 50s – perhaps careers are peaking, kids are grown, and the desire for a stable, personal haven is stronger than ever. This isn't the stuffy, complicated process you might imagine; it's more about understanding your financial picture and knowing what lenders are looking for. Let’s dive into what makes getting a mortgage at 50 not just doable, but potentially a really smart move!

Why 50 is a Great Time to Consider a Mortgage

So, why is this topic so popular and, dare we say, fun? Because it shatters a lot of outdated myths! For generations, there was this unspoken idea that mortgages were strictly for the young and the ambitious. But times have changed. Lenders are much more focused on your current financial health than your birth certificate. For many people in their 50s, this can be a sweet spot. You've likely built up a solid credit history, possibly paid off other significant debts, and might have a substantial down payment saved up. This translates into a stronger application and potentially better terms. Think of it as leveraging all those years of hard work and smart financial decisions.

The benefits of getting a mortgage at 50 are manifold. Firstly, homeownership itself provides incredible stability and a sense of belonging. Imagine finally having that dream home, decorated exactly to your taste, without worrying about landlord restrictions. It's an investment in your future comfort and security. Secondly, it can be a strategic financial move. Real estate has historically been a reliable asset class for long-term growth. Owning a home can contribute to your net worth and provide equity that can be used for future needs, like retirement planning or even helping out family. Plus, imagine the satisfaction of having your mortgage potentially paid off by the time you reach traditional retirement age, meaning lower living expenses during those golden years. It’s about taking control of your housing costs and building lasting wealth.

What Lenders Look For (And How You Shine!)

When you apply for a mortgage, lenders are essentially assessing your ability to repay the loan. At 50, you have a lot of strengths to highlight. The primary factors they’ll scrutinize are:

- Income Stability: Lenders want to see a consistent and reliable income stream. At 50, you likely have a well-established career and a strong employment history. This is a huge plus! If you're self-employed, ensure your financial records are impeccable and showcase a steady income over several years.

- Credit Score: Your credit score is like your financial report card. Years of responsible borrowing and repayment at this age often mean you have an excellent credit score, which is music to a lender's ears. A higher score typically translates to lower interest rates.

- Debt-to-Income Ratio (DTI): This is the percentage of your gross monthly income that goes towards paying your monthly debt payments. Many people in their 50s have fewer outstanding debts (e.g., student loans paid off, car loans finished) which can lead to a favorable DTI.

- Down Payment: The more you can put down, the less you need to borrow, which reduces the lender's risk and often gets you better loan terms. Many individuals in their 50s have significant savings or equity from selling a previous home, allowing for a substantial down payment.

- Assets and Savings: Lenders like to see that you have liquid assets (savings, investments) beyond your down payment. This shows you have a financial cushion for unexpected expenses and can continue to manage your mortgage payments even if your income fluctuates.

Navigating the Mortgage Process at 50

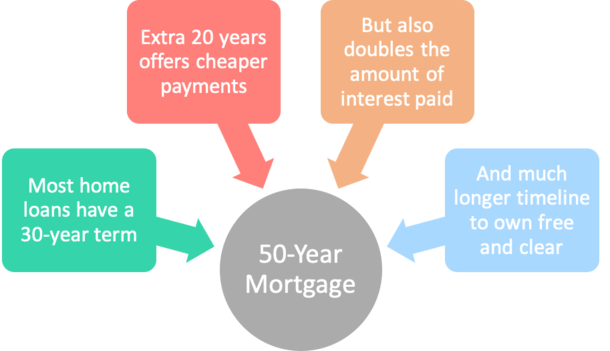

The process itself isn't dramatically different from what someone younger might experience, but there are a few nuances to consider. The main difference might be the term of the mortgage. While younger buyers might opt for a 30-year mortgage, at 50, you might consider a shorter term, like a 15-year or 20-year mortgage. This means higher monthly payments but significantly less interest paid over the life of the loan and potentially being mortgage-free well before traditional retirement. This is where the "fun" comes in – you're making a strategic decision that aligns with your life stage and future goals.

Be prepared for increased scrutiny regarding your retirement plans. Lenders might ask about your projected income in retirement and ensure you have sufficient funds to cover your living expenses after the mortgage is paid off. This isn't to deter you, but to ensure the loan is sustainable for your entire life. Having clear documentation of your retirement savings, pensions, and investment strategies can be very helpful here.

Consider your health and life expectancy. While lenders can't discriminate based on age, they do consider the length of time they'll be receiving payments. Lenders will look at your overall financial health and stability. If you have existing health conditions that might impact your ability to work or earn income in the future, it’s wise to have a robust financial plan in place.

Explore different mortgage types. Beyond traditional fixed-rate mortgages, there are options like adjustable-rate mortgages (ARMs) that might have lower initial payments, but be sure to understand the risks of fluctuating interest rates. Speak with a mortgage broker or loan officer to discuss what best fits your financial situation and risk tolerance. They are there to guide you!

Tips for a Smoother Application

To make your mortgage application as smooth as possible, focus on these key areas:

- Gather all your financial documents: This includes pay stubs, tax returns (usually the last two years), bank statements, investment account statements, and any documentation for other income sources.

- Get pre-approved: This helps you understand how much you can borrow and shows sellers you're a serious buyer.

- Be upfront and honest: Disclose all your income and assets accurately.

- Consult with professionals: A good mortgage broker can be invaluable, helping you navigate the options and present your strongest case to lenders. A financial advisor can also help you assess how a mortgage fits into your overall retirement plan.

Getting a mortgage at 50 isn't just an option; it's a testament to your financial journey and a fantastic way to secure your future comfort and wealth. With careful planning and a clear understanding of what lenders require, your dream home is well within reach. So, embrace this exciting chapter – your golden years might just be the perfect time to invest in your own piece of paradise!