Can I Borrow Against My 401k To Buy A House

So, you're dreaming of that little bungalow. Or maybe a chic city loft. Whatever your housing fantasy, it probably involves a ton of cash. And you're thinking, "Hey, what about my 401k?"

It's a question that pops into a lot of heads. Like, "Can I snag some of my retirement cash to snag my dream pad?" The answer is… kinda. It's not exactly a free-for-all, but it's definitely a thing some people explore.

The Great 401k House Hunt Caper

Picture this: You're scrolling Zillow. Unicorn listing pops up. Your heart does a little jig. But then, reality hits. Your down payment fund is looking a bit… sad. Enter the 401k. It's like a secret stash of cash, right? Well, a retirement stash. So, using it for a house feels a bit like raiding your future self's piggy bank.

But hey, we're talking about buying a house! That's a major life event. It's exciting! It's stressful! It's the kind of thing that makes you ponder all sorts of creative (and maybe slightly eyebrow-raising) financial maneuvers.

Let's Talk "Borrowing"

When you "borrow" from your 401k, you're not actually taking it out in the traditional sense. It's more like you're loaning it to yourself. Your retirement account becomes your personal ATM, but with a few very important caveats.

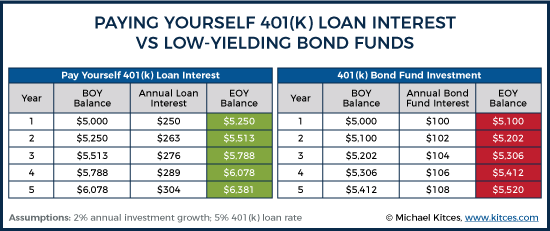

Think of it like this: You're your own bank. You owe yourself the money back. And there's interest involved. Yep, you pay yourself interest! How meta is that?

This is where things get interesting. It's a bit of a financial juggling act. You're taking money from your future security to fund your present comfort. It's a trade-off, a high-stakes negotiation with your future self.

The Nitty-Gritty (Don't Worry, We'll Keep it Fun!)

So, how does this borrowing magic actually work? Typically, you can borrow up to 50% of your vested balance, or $50,000, whichever is less. So, if you have a million bucks saved up (good for you!), you can't just take it all. There are limits, because, you know, retirement planning and all that.

And you have to pay it back. Usually within five years. Unless you're using it for a primary residence, then you might get a bit more breathing room. Like, years more breathing room. Imagine paying yourself back over 15 or even 25 years! It's like a super-long-term loan from… yourself.

The interest rate? It's generally set by your plan, often tied to the prime rate. It's usually not a terrible rate, which is one of the attractive parts. You're not giving a huge chunk to an external lender.

Why is This Even a Thing?

Well, for starters, a house is a big purchase. A down payment can be a massive hurdle. Sometimes, it feels like the only way to get your foot in the door.

And let's be honest, the idea of accessing your own money without the typical hoops and hurdles of a bank loan is pretty appealing. It feels… direct. Like you're cutting out the middleman.

Plus, it’s a fun topic to chat about! It taps into that "what if" side of our brains. What if I could just… tap into that nest egg? It’s a little bit forbidden, a little bit exciting.

The Quirky Side of 401k Loans

Did you know that some people treat their 401k loan payments like a fun savings challenge? They're literally paying themselves back. Imagine that! You're basically building wealth twice – once in your retirement account, and then again as you repay the loan to yourself.

It’s like a financial ouroboros. The snake eating its own tail, but in a good, money-growing way. You're both the borrower and the lender. It's a solo financial adventure!

And think about it: no credit check! For people who might have a tricky credit score, this can be a lifesaver. It’s your money, after all. You don't need permission from a credit bureau to borrow from yourself.

The "What If" Scenarios Are Endless

What if you get a big bonus and decide to pay off a chunk of your loan early? You just saved yourself a bunch of interest payments. High five, future you!

What if you change jobs? Ah, now things get a little dicey. Typically, if you leave your employer, you have to pay back the loan much sooner. Like, 60 days sooner. That’s a big deal. It’s like a financial surprise party you didn’t ask for.

This is where the fun can quickly turn into a bit of a panic. Suddenly, you need a pile of cash now. And if you can't pay it back, guess what? It becomes a withdrawal. And withdrawals before retirement age often come with a 10% penalty. Ouch.

So, Should You Do It?

That’s the million-dollar question, isn't it? Borrowing from your 401k for a house is like having a superhero power, but one with a secret weakness. It can help you achieve a major goal, but it comes with risks.

.png)

You’re essentially taking money that’s meant to grow for decades and using it now. That means you’re missing out on potential investment gains. That’s the biggest downside. Imagine your money compounding over years! You’re pausing that magic.

Plus, if you lose your job and can’t repay the loan, you could face taxes and penalties. That’s a pretty hefty consequence for a quick financial fix.

It's All About the Balance

Ultimately, borrowing from your 401k for a house is a deeply personal decision. It’s about weighing the immediate gratification of homeownership against the long-term security of your retirement.

It’s not a decision to take lightly. Talk to a financial advisor. Understand the rules of your specific 401k plan. And most importantly, have a solid plan for repaying the loan. Because while it's fun to think about, messing with your retirement fund is a serious business.

But hey, at least we can have a laugh and a curious chat about it, right? The world of personal finance is full of these quirky, thought-provoking scenarios. And this one, about borrowing from your future self to buy a piece of the present? It’s definitely a conversation starter.