Borrowers Choosing An Adjustable Rate Mortgage Brainly

Alright, let's talk about mortgages. Specifically, the ones that make your head spin a little. We're diving into the wild world of Adjustable Rate Mortgages, or ARMs, for those in the know. And trust me, there's a whole lotta "knowing" happening when people decide to hop on this particular rollercoaster.

Now, before you picture me in a tiny suit climbing into a miniature car, let's clarify. We're not talking about actual borrowers on a giant scale. We're talking about the idea of borrowers, the concept of choosing an ARM. It's a bit of a thought experiment, a playful poke at a financial decision that can feel as exciting as it is terrifying.

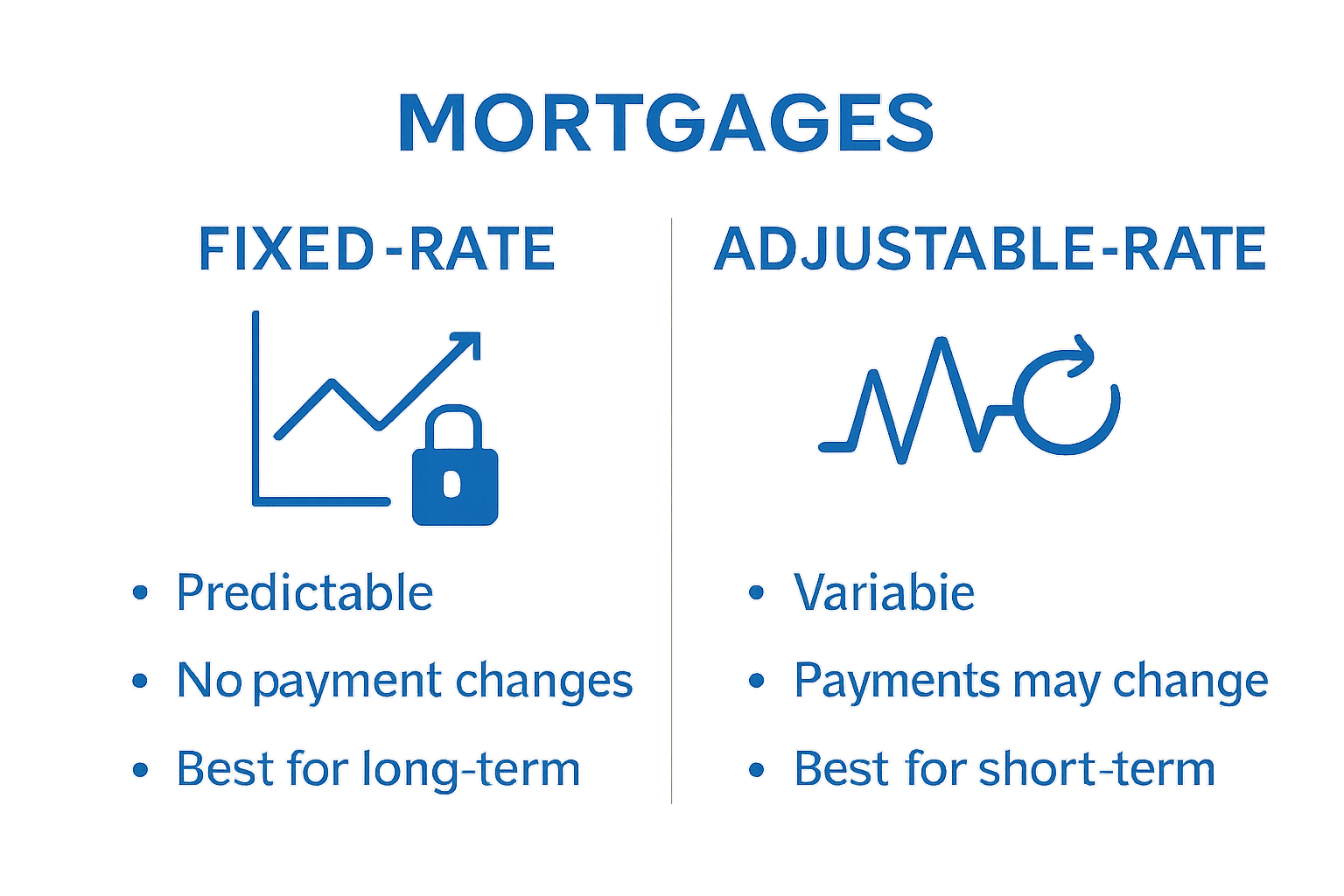

Imagine this: you're at the mortgage buffet. You've got your fixed-rate 'all-you-can-eat' option, nice and predictable. Then, there's the ARM. It's the 'mystery meat special' of home loans. Sometimes it's delicious, sometimes... well, let's just say your wallet might regret it.

Why would anyone choose the mystery meat? That's the million-dollar question, isn't it? Or, more accurately, the several-hundred-thousand-dollar question. It's a gamble, a calculated risk, or perhaps, a hopeful wish upon a falling interest rate star.

Think about the person who signs on the dotted line for an ARM. They're probably pretty optimistic. They're looking at those initial lower payments and thinking, "Yes! I can afford this beautiful house!" They envision themselves living the dream, perhaps with a little extra cash for fancy patio furniture or that really nice rug they've been eyeing.

And for a while, it's glorious. The payments are indeed lower. They're making their mortgage payments, feeling smug, and maybe even bragging to their friends about their "smart" financial move. "Oh, you're still paying that much? Mine went down!" they might chirp, blissfully unaware of the storm clouds gathering on the horizon.

The thing about ARMs is they have an initial period where the interest rate is fixed. This is the honeymoon phase. It's like that first date where everything is perfect, and you can't imagine anything going wrong. You're smitten, and the payments are easy to handle.

:max_bytes(150000):strip_icc()/what-is-an-adjustable-rate-mortgage-3305811_V2-d24ce035796b4b3ebb7cee3f65049a24.png)

But then, the music changes. The adjustable part kicks in. Suddenly, your payment can go up. And up. And up. It’s like your friendly barista suddenly decides to charge you extra for the foam, every single day.

This is where the "unpopular opinion" part comes in. While many financial gurus will tell you ARMs are a recipe for disaster for the average homeowner, I have a soft spot for the brave souls who choose them. There’s a certain daring spirit involved.

It’s like choosing to ride a roller coaster with a few unexpected drops. You know there's a thrill, and there's a chance you might scream your head off, but you do it anyway. Maybe you love the adrenaline rush of not knowing exactly what your payment will be next month.

Perhaps these borrowers are secretly financial wizards. Maybe they have a crystal ball that shows them interest rates will plummet. Or maybe, just maybe, they’re excellent at improvising. They’re the kind of people who can whip up a gourmet meal with whatever’s left in the fridge.

Let’s consider the scenario where interest rates do go down. In this case, the ARM borrower is practically doing a happy dance. Their payments decrease, and they feel like a genius. They've outsmarted the market, and their wallet is singing a joyous tune. This is the dream scenario, the lottery win of homeownership.

But what if interest rates climb like a mischievous cat scaling a bookshelf? Then, those initial savings can quickly evaporate. Suddenly, that "affordable" house feels a whole lot less so. This is where the popcorn comes out for the observers, the ones who chose the predictable fixed-rate path.

It's like watching a tightrope walker. You're on the edge of your seat, a mix of admiration and terror. You admire their courage, but you also can't help but wince a little when they wobble.

The borrowers who choose ARMs are, in my book, the true risk-takers. They’re not afraid of a little financial uncertainty. They're the pioneers, charting unknown waters while the rest of us are safely moored in the harbor of a fixed rate.

There's an undeniable charm to this audacity. It’s the same charm as someone who decides to wear mismatched socks to a formal event. It’s bold, it’s unexpected, and it certainly makes things interesting.

And let's be honest, who among us hasn't made a questionable financial decision at some point? We've all bought that impulse item we didn't need, or invested in a fad that quickly fizzled out. The ARM borrower is just doing it on a much grander scale.

They’re the ones who believe in the power of positive thinking, even when it comes to their monthly housing expenses. They’re the optimists who believe tomorrow will be better, and their mortgage payment will magically shrink.

So, next time you hear about someone choosing an Adjustable Rate Mortgage, don't just shake your head. Offer a little nod of respect. They're playing a different game, a game with higher stakes and potentially higher rewards. They’re the thrill-seekers of the housing market, and while I might stick to my boring old fixed rate, I can't help but admire their spunk.

It’s a decision that requires a certain level of financial gymnastics. You need to be able to leap from low payments to potentially higher ones without breaking a sweat. It’s a skill that not everyone possesses, but those who do are certainly… interesting.

Perhaps they're just really good at budgeting and can absorb those potential increases. Or maybe they have a secret side hustle that provides a buffer for any unexpected payment hikes. We can only speculate, and it’s more fun to imagine them as daring financial adventurers.

Ultimately, the choice of a mortgage is personal. But the ARM borrower? They’re the ones who make it a conversation. They’re the ones who keep the financial world a little more unpredictable, and dare I say, a little more entertaining. They are the brave, the bold, and sometimes, the ones who might be silently sweating when interest rates start to climb.

And in a world that often feels a bit too predictable, there's something to be said for that. So, here's to the ARM borrowers. May your interest rates be ever in your favor, or at least, may you be excellent at improvising when they're not.

"It's not about if the interest rate will change, but when and by how much."

That’s the silent mantra of the ARM borrower. They’re not ignorant; they’re just willing to dance with the unknown. They’re the ones who believe they can navigate the financial currents better than the average sailor. And who are we to argue with that kind of confidence?

It’s a decision that makes you lean in and pay attention. You want to know how it turns out. Will they soar, or will they stumble? The suspense is almost as good as a cliffhanger novel.

So, let’s raise a glass (of something affordable, of course) to the borrowers who choose the Adjustable Rate Mortgage. They’re the spice in the otherwise bland stew of home financing. They’re the ones who remind us that sometimes, a little bit of risk can lead to a whole lot of story.