American Express Charge Card Vs Credit Card

Hey there, folks! Ever found yourself staring at two shiny plastic rectangles in your wallet, both with that familiar Amex logo, but one whispering "charge card" and the other shouting "credit card"? It's like trying to choose between a trusty old dog and a sleek new sports car – both get you where you need to go, but in very different ways. Let's break down this whole American Express charge card vs. credit card thing, without needing a business degree to understand it.

Think of it this way: your charge card is like a friendly reminder. You know that awesome new gadget you bought online? Or that spontaneous weekend getaway with your pals? With a charge card, you're generally expected to pay the full amount by the due date, every single month. No carrying a balance, no accruing interest. It's like saying, "Yep, I bought it, and I'll settle up completely soon!"

Now, your credit card? That's more like a helpful buddy who says, "Don't have all the cash right now? No sweat! You can pay me back over time." This is where that magic word, interest, comes into play. If you don't pay your credit card balance in full by the due date, you'll start racking up interest charges. It's like a little fee for borrowing their money longer.

Let's paint a picture. Imagine you're at your favorite local coffee shop, the one that makes those ridiculously delicious croissants. You decide to treat yourself and your coworker to a couple of fancy coffees and pastries. If you whip out your Amex charge card, you're essentially saying, "I'm buying this now, and I'll clear this whole tab when the bill comes." It's straightforward, no funny business.

Now, picture a bigger splurge. Maybe you're finally redoing that kitchen, or perhaps you snagged an amazing deal on a new living room sofa. These are purchases that might stretch your immediate budget. This is where your Amex credit card shines. You can make that big purchase, enjoy your beautiful new kitchen or comfy couch, and pay it off in manageable chunks over several months. You'll pay a bit of interest, but it allows you to get that big thing now without draining your savings account.

So, why should you even care about this distinction?

Well, it all comes down to your spending habits and your financial goals. It’s not about one being inherently "better" than the other; it’s about finding the right tool for the right job, just like you wouldn’t use a hammer to screw in a lightbulb (unless you’re going for a very avant-garde approach, of course).

Let's talk about the charge card lifestyle. Think of it as a discipline builder. If you're someone who likes to keep things neat and tidy, and you generally have the cash flow to cover your expenses each month, a charge card can be fantastic. It helps you avoid the sneaky trap of credit card debt. It’s like having a built-in mechanism to prevent you from overspending, because you know that full payment is coming down the pike.

I remember a friend, Sarah, who was always a bit worried about getting into debt. She got an Amex Green Card (a classic charge card) when she first started her career. She loved that it forced her to be mindful of every swipe. She said it felt like a personal finance bootcamp, but a rather pleasant one, full of travel rewards and good service!

On the other hand, if you're saving up for something big, or you like the flexibility to spread out payments for larger purchases, a credit card might be your jam. It's the "buy now, pay later" option, but with a structured repayment plan. It can be a lifesaver for unexpected emergencies too. That leaky roof? The sudden car repair? A credit card can bridge the gap while you figure things out.

Consider Mark, another friend. He was renovating his house and needed to buy all new appliances. He used his Amex Platinum Card (which can function as a credit card with a Pay Over Time feature) for the bulk of the purchases. This allowed him to spread the cost over a few months, keeping his savings intact for other renovation expenses, while still earning those sweet travel points he loves for his family vacations.

The Perks and Pitfalls (in simple terms!)

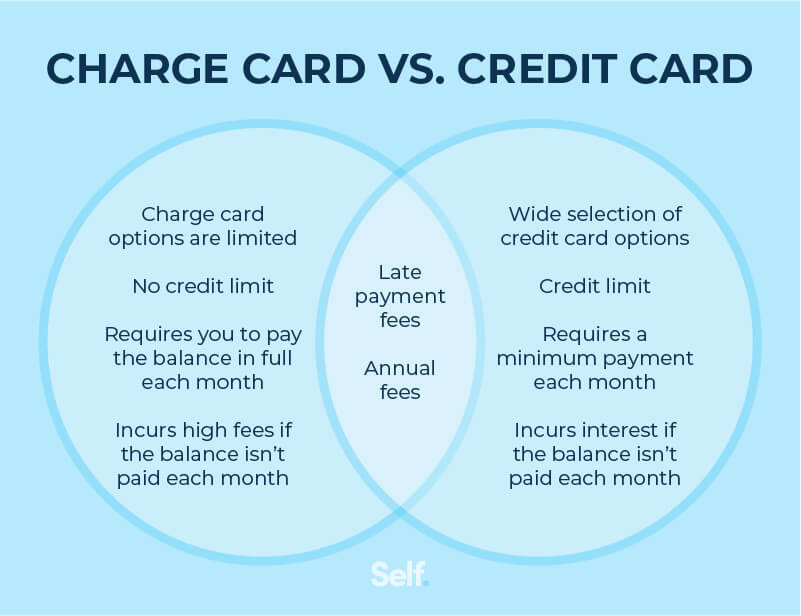

Charge Cards often come with:

- No preset spending limit: This is a big one! While not unlimited, it means your spending power can adjust based on your history and financial behavior. It's more about responsible spending than hitting a hard cap.

- Focus on full payment: This encourages good financial habits and helps you avoid interest.

- Potentially premium rewards: Many Amex charge cards are known for their generous rewards programs, especially for travel and dining.

The flip side? You must pay it off in full. If you miss a payment, there can be hefty late fees. And if you consistently can't pay, well, that's not great for your credit score, even with a charge card.

Credit Cards often come with:

- A preset spending limit: You know your maximum borrowing amount.

- Ability to carry a balance: This is the key feature for spreading payments.

- Interest charges if you don't pay in full: This is the cost of borrowing.

- Rewards and benefits: Just like charge cards, credit cards offer a world of points, cashback, and perks.

The danger here is the temptation to spend more than you can afford and get stuck in a cycle of debt, with interest eating away at your money. It's like a leaky faucet – a small drip might seem insignificant, but over time, it can waste a lot of water (or money!).

Finding Your Perfect Amex Match

So, how do you decide? Ask yourself these simple questions:

- Am I disciplined with my spending? Do I usually have enough cash to cover my monthly expenses without breaking a sweat? If yes, a charge card could be your best friend.

- Do I prefer to pay things off quickly, or do I sometimes need flexibility? If you like the idea of paying in full and avoiding interest, go charge. If you like the option to spread out payments for bigger items, a credit card with a "Pay Over Time" feature might be better.

- What are my biggest financial goals right now? Are you trying to aggressively save and avoid debt? Or are you planning a big purchase and need to manage cash flow?

American Express offers a fantastic range of both charge and credit cards, each with its own unique set of perks and benefits. Whether you're a frequent flyer looking for airline miles, a foodie chasing restaurant rewards, or someone who simply wants a reliable way to manage your daily spending, there's likely an Amex card out there for you.

The key takeaway is that understanding the difference between a charge card and a credit card empowers you to make smarter financial decisions. It's not about a fancy logo; it's about choosing the right tool to help you achieve your financial dreams, whether that's a dream vacation or a perfectly renovated kitchen, all while keeping your wallet happy!